Understanding the NCCI Mod Worksheet: A Guide for Staffing Companies (2026)

If you own or manage a staffing agency, your NCCI mod worksheet may be the single most important document affecting how much you pay for workers’ compensation insurance. Most staffing owners receive this worksheet and set it aside — but that’s a costly mistake.

This guide breaks down every section of the NCCI experience modification worksheet in plain language, explains why staffing companies face unique challenges with their mod, and gives you concrete steps to lower it.

Whether you’re seeing your mod for the first time or trying to understand why your premium jumped at renewal, this post covers what you need to know for 2026.

What Is the NCCI Mod Worksheet?

The NCCI Experience Modification Worksheet is a document produced by the National Council on Compensation Insurance (NCCI) that calculates your Experience Modification Factor — also called your “mod,” “e-mod,” or “EMR.”

Your mod is a multiplier applied directly to your base workers’ compensation premium. A mod of 1.00 means you’re paying the average rate for your industry. A mod below 1.00 means you’re paying less because you have fewer claims than peers. A mod above 1.00 means you’re paying a surcharge because your claims history is worse than average.

Quick Example

If your base workers’ comp premium is $80,000 and your mod is 1.20, you pay $96,000 — an extra $16,000 per year simply because of your claims history.

NCCI calculates mods for 38+ states. If you operate in a state that uses its own rating bureau (like California, which uses the WCIRB), the process is similar but the bureau differs.

You will typically receive your updated mod worksheet approximately three months before your workers’ compensation policy renews.

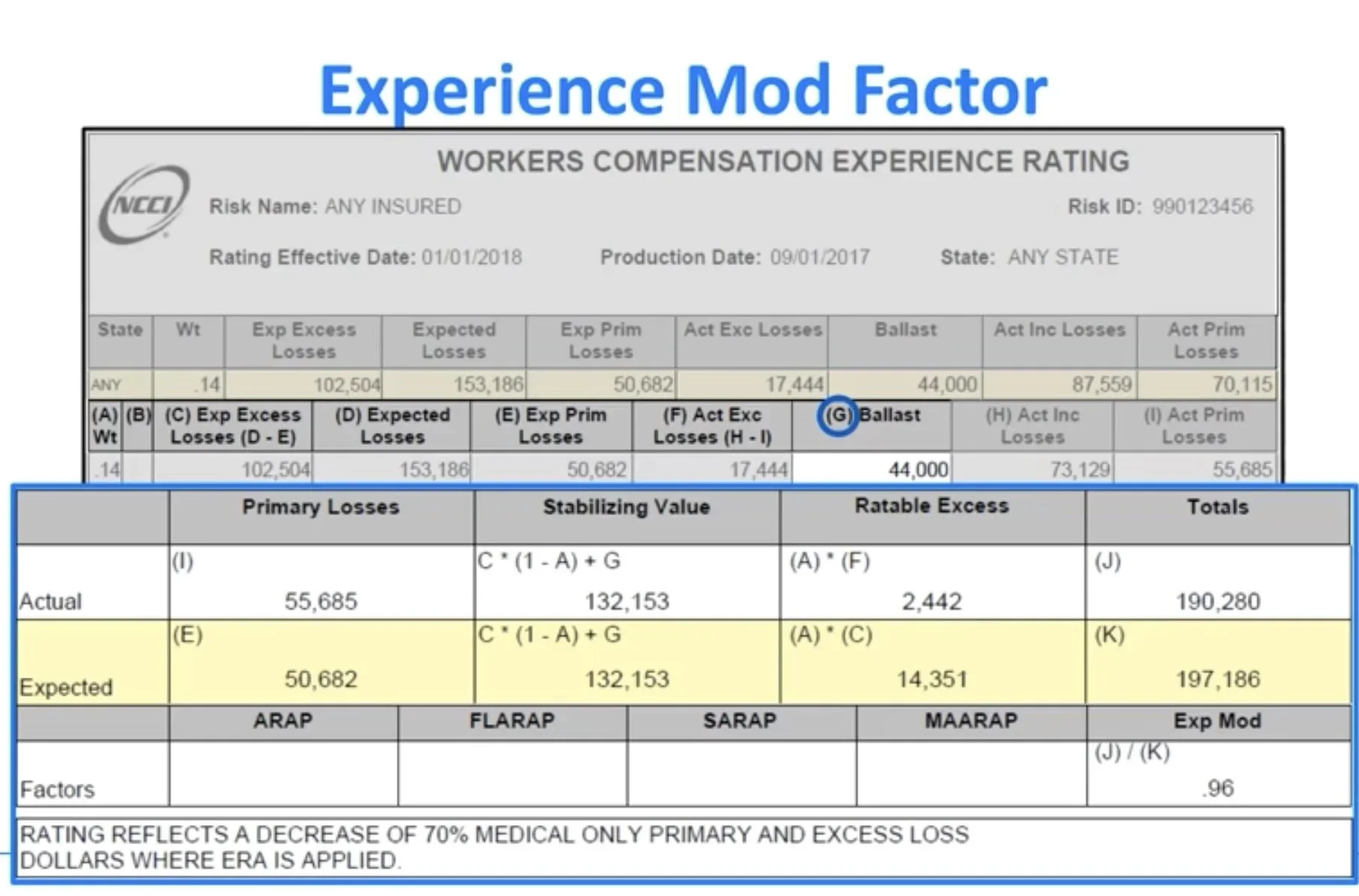

How to Read Your NCCI Mod Worksheet: Section by Section

The worksheet may look dense at first, but it follows a consistent structure. Here’s what each part means:

1. Header Information

The top of the worksheet shows your company name, address, NCCI risk ID number, policy number, and whether your business is rated as a single state or multi-state (interstate) risk. Double-check that your legal entity name and risk ID are correct — errors here can cause the wrong mod to be applied to your policy.

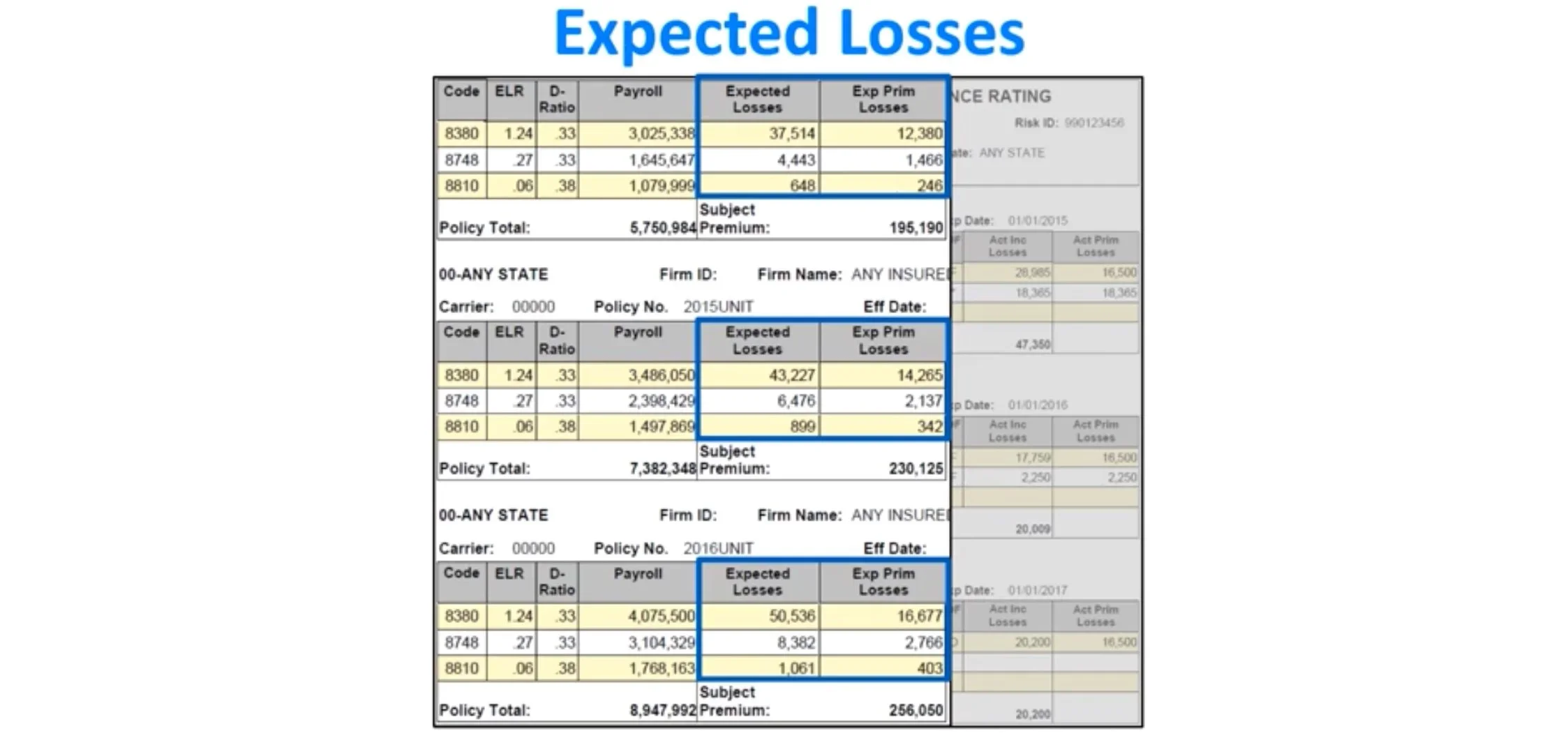

2. Policy Periods (Three Years of History)

The worksheet pulls in three years of payroll and loss data, but excludes the most recent policy year since audited data may not yet be filed. The oldest period appears at the top and the most recent at the bottom. Each year includes your payroll broken down by classification code.

For staffing companies, you’ll often see multiple classification codes — for example, clerical (8810), light industrial (varies by state), IT staffing (8742), and so on. Each carries a different Expected Loss Rate.

3. Classification Codes and Payroll

Each row represents a workers’ comp class code tied to the type of work your placed employees perform. The payroll listed is your audited payroll for that year and code. Verify these numbers against your own payroll records — overstated payroll in a high-risk class code inflates your expected losses and can distort your mod.

4. Expected Loss Rate (ELR)

The Expected Loss Rate tells you how many dollars of losses NCCI expects for every $100 of payroll in a given class code. These rates are set actuarially by state and updated periodically. If NCCI expects $2.50 per $100 of payroll in your most common class code and you have $5 million in payroll, your expected losses for that class and year are $125,000.

5. D-Ratio (Discount Ratio)

The D-ratio is used to split your expected losses into primary (more predictable, frequency-driven) and excess (severity-driven) components. NCCI places greater weight on primary losses when calculating your mod because frequent small claims are more indicative of your safety culture than one large unpredictable event.

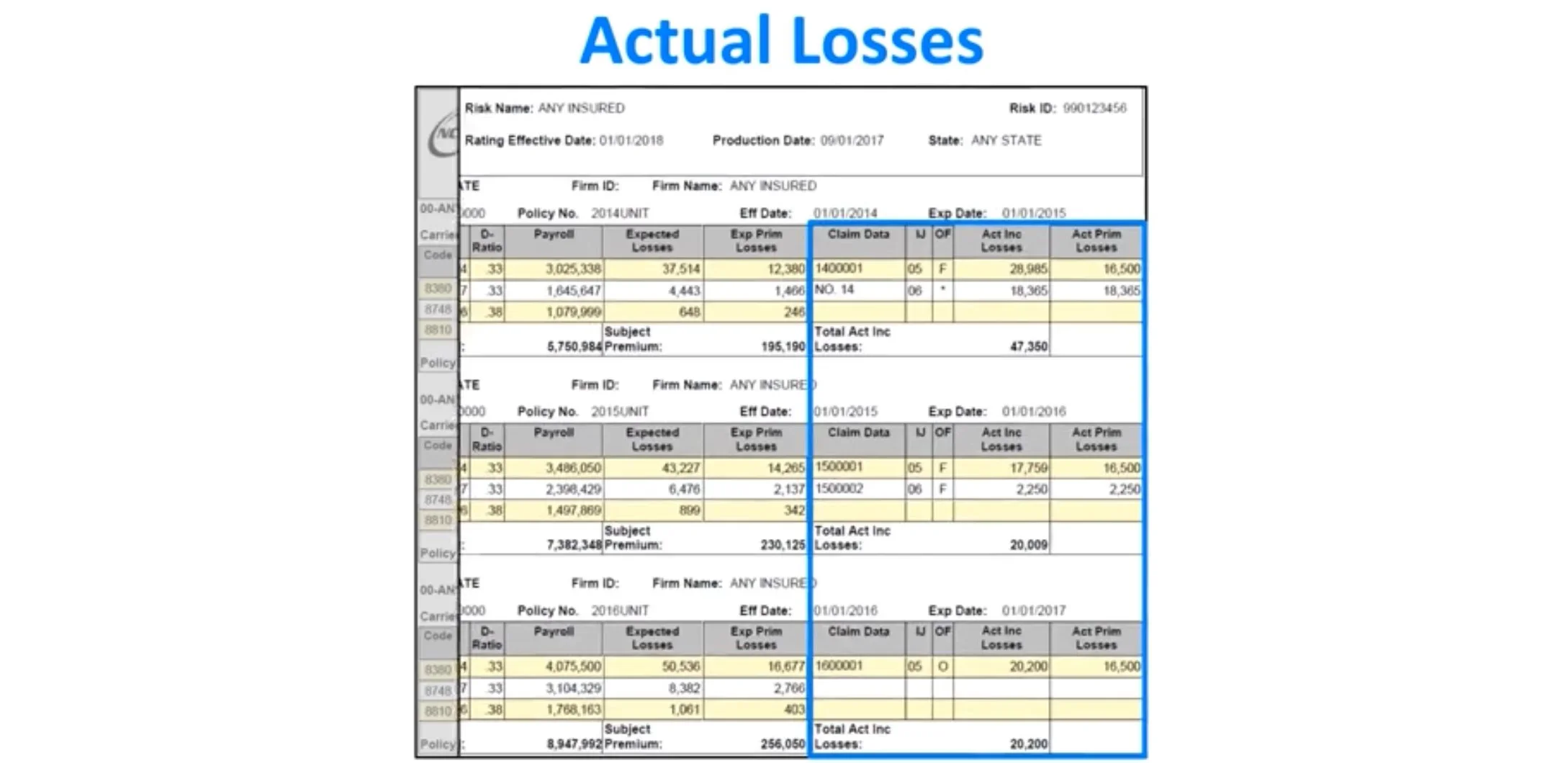

6. Actual Losses: Primary vs. Excess

Each claim in the three-year period is split into a primary and excess component. The split point (called the “split point” or primary threshold) is currently $18,500. That means for any claim, the first $18,500 counts as primary loss. Anything above $18,500 is excess.

This is one of the most important concepts for staffing owners: a single catastrophic claim matters less than multiple smaller, frequent claims. Frequency hurts you more than severity in the mod formula.

7. The Mod Calculation

Once actual losses are compared to expected losses, NCCI applies a credibility weighting based on your company’s size (called the ballast and weighting values). Larger companies are held more accountable to their own history; smaller companies are blended more with industry average. The final output is your mod number.

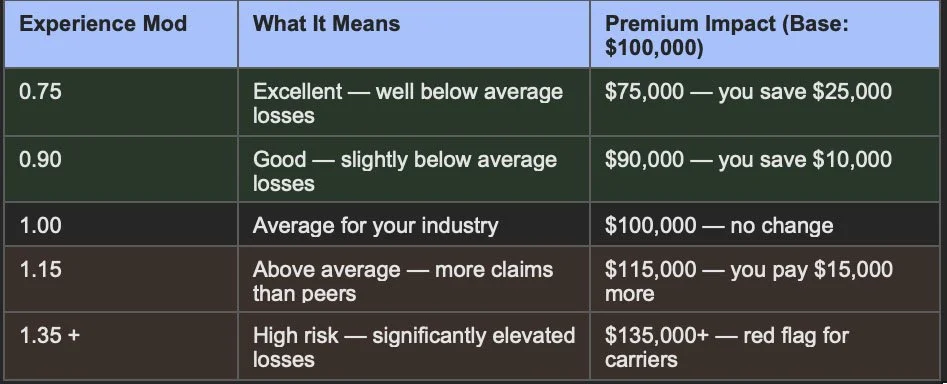

What Does Your Mod Number Actually Cost You?

Here’s how different mod values translate to real dollars on a $100,000 base workers’ comp premium:

For staffing agencies, which often carry large workers’ comp premiums due to high headcount and labor-intensive placements, even a 0.10 improvement in your mod can save thousands of dollars per year.

Why Staffing Companies Face Unique Mod Challenges

Managing an experience mod is harder for staffing companies than for most other businesses. Here’s why:

• Turnover: High employee turnover means more individuals are exposed to workplace injuries across more worksites.

• Multiple class codes: Multiple class codes with different ELRs make mod management more complex than single-trade businesses.

• Limited worksite control: You don’t always control the job sites where your workers are placed, which limits your ability to prevent injuries.

• Open claim reserves: Open claims with high reserves can inflate your mod even before they are fully resolved.

• Classification errors: Misclassification of workers into higher-risk class codes is a common and correctable problem.

None of these challenges are insurmountable, but they do mean that staffing company owners need to be more proactive about reviewing their mod worksheet than most other business owners.

How to Lower Your Experience Mod as a Staffing Company

A high mod isn’t permanent. Because the worksheet uses a rolling three-year window, improvements you make today will be reflected in your mod within one to two renewal cycles.

1. Close open claims: Audit your open claims and push for timely closure. Open reserves inflate your mod. Work with your carrier’s claims team to close stale claims and challenge inflated reserves.

2. Return-to-work programs: Implement a return-to-work program. Getting injured workers back to modified duty — even light office tasks — reduces the total claim cost and your future mod.

3. Check class code accuracy: Verify your classification codes. If workers are coded into a higher-risk class when their actual duties are lower risk, you’re both overpaying in premium and distorting your mod. Request a classification audit.

4. Dispute worksheet errors: Dispute errors on the worksheet. NCCI accepts correction requests from your broker or carrier. Incorrect payroll, mismatched loss data, or wrong policy periods can all be corrected.

5. Pre-placement screening: Invest in pre-placement screening. Verifying candidate work history and conducting safety orientations before placements reduces the frequency of claims — which is what the mod formula cares about most.

6. Work with a specialist: Work with a broker who understands your worksheet. Many staffing owners work with generalist brokers who don’t review the mod until renewal. A specialist will review your worksheet proactively each year.

Akker Tip

At Akker, we review our staffing clients’ NCCI mod worksheets proactively, not just at renewal. We’ve helped clients identify classification errors and open claim issues that, once corrected, reduced their mod by 0.10 to 0.20 — translating to thousands of dollars in annual premium savings.

NCCI Mod Worksheet FAQ

These are the questions staffing company owners ask us most often.

How often does my mod change?

Your mod is updated once per year, typically 3 months before your workers’ comp policy renews. It reflects the most recent three complete policy years of data.

Can I dispute my experience mod?

Yes. If you believe your payroll or loss data is incorrect, your broker or insurance carrier can file a correction request with NCCI. Act quickly — corrections are easier to make before the mod is finalized and applied to your renewal.

What is a “contingent mod”?

A contingent mod is issued when NCCI has not yet received audited payroll or loss data from your carrier. Once that data is received, your mod is revised. A contingent mod is not final — never assume it reflects your true history.

Does one large claim ruin my mod?

Not as much as people think. Because of the primary/excess split at $18,500, the excess portion of a large claim is weighted less heavily. Frequent smaller claims actually hurt your mod more than a single catastrophic event.

My mod is above 1.00 — will carriers decline to insure me?

A mod above 1.00 won’t automatically disqualify you, but mods above 1.20–1.25 can start limiting your market options and triggering higher rates. Some admitted carriers have maximum mod eligibility requirements. The higher your mod, the more important it is to work with a broker who has access to specialty staffing markets.

What states don’t use NCCI?

California (WCIRB), North Dakota, Ohio, Washington, and Wyoming have state-operated workers’ comp funds or their own rating bureaus. New York, Massachusetts, and several others use their own independent bureaus. If you place workers across multiple states, your mod calculation may involve multiple bureaus.

Not Sure What Your Mod Means for Your Business?

We review NCCI mod worksheets for staffing companies every day. If you’d like a second set of eyes on yours — or want to know if your current coverage is the right fit — reach out to Akker for a free review.

→ Get a Free Mod Worksheet Review — akkerins.com/staffinginsurance

#staffinginsurance #nccimod #staffingnccimod