How to Lower Your Workers' Comp Insurance Cost: The Complete Guide for Any Business

Workers' compensation insurance is one of the largest controllable line items on a business's P&L — and one of the most misunderstood. Most owners treat it like a tax: an unavoidable cost that goes up every year. The truth is the opposite. Workers' comp premium is one of the few insurance lines you can actively engineer downward through risk management, claims discipline, NCCI experience modification (mod) review, premium audit prep, smarter program structures, and the right carrier relationship.

This guide is industry-agnostic. Whether you run a manufacturing plant, a staffing firm, a construction company, a restaurant group, a clinic, a logistics operation, an office-only professional services firm, or a 12-person startup, the levers are the same. We walk through every one of them — what to do, in what order, and what kind of premium impact to expect — so you can reduce your workers comp premium, lower your experience mod, and stop overpaying on audit.

The 7 Biggest Workers' Comp Cost Levers

1) Lower your NCCI experience modification factor. 2) Audit your class codes. 3) Prepare aggressively for premium audits. 4) Report and manage claims fast (the first 24 hours decide the cost). 5) Run a real return-to-work (RTW) program. 6) Choose the right premium structure (guaranteed cost, dividend, deductible, retro, group, captive, or PEO). 7) Document everything — safety, training, incidents, mod worksheets, and audit workpapers.

Table of Contents

1. How Workers' Comp Premium Is Calculated (the formula every owner should know)

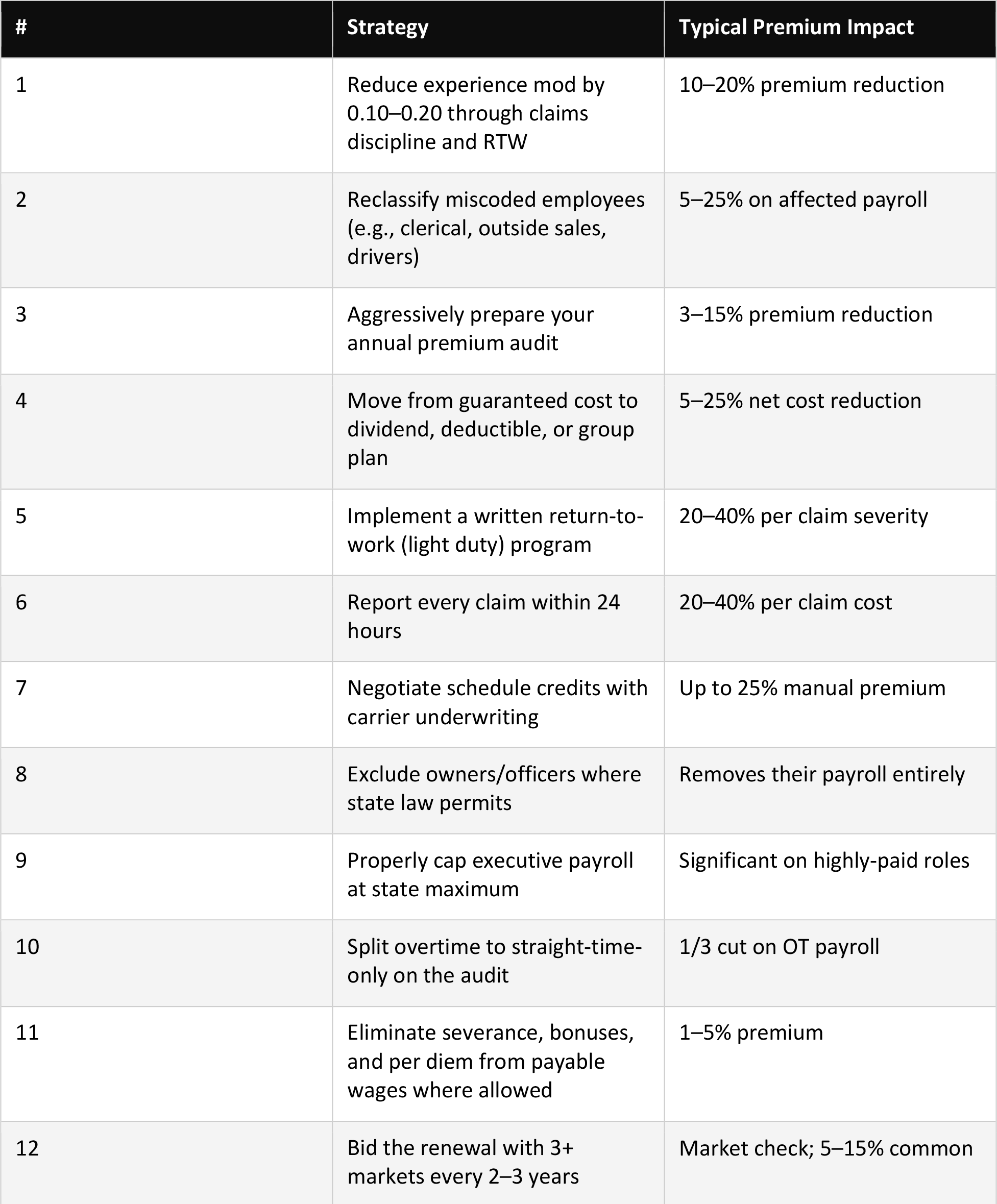

2. 12 Concrete Ways Any Business Can Save on Workers' Comp

3. Risk Management Procedures That Actually Move the Premium Needle

4. Claims Handling: How to Close Claims Faster and Cheaper

5. The NCCI Experience Modification (Mod) Deep Dive — Audit, Lower, Dispute

6. Premium Audit Preparation — Stop Overpaying at Year-End

7. Class Code Review and Reclassification Opportunities

8. Choosing the Right Carrier, Agent, and Program Structure

9. Deductible and Retention Strategies

10. Loss-Sensitive Plans: Retro, Large Deductible, Captive, Self-Insurance

11. Wellness Programs and Their Real Premium Impact

12. Documentation and Record-Keeping Best Practices

13. FAQ — Workers' Comp Insurance for Businesses

1. How Workers' Comp Premium Is Calculated

Before you can lower the cost, you need to understand the math. In most NCCI states (and most independent state bureaus follow the same skeleton), the simplified formula is:

The Workers' Comp Premium Formula

Manual Premium = (Payroll ÷ 100) × Class Code Rate Modified Premium = Manual Premium × Experience Mod (EMR) Final Premium ≈ Modified Premium × Schedule Credits/Debits × Premium Discount × Expense Constant ± Surcharges/Assessments

Three of those four inputs are directly within your control:

• Payroll (the exposure base) — audited annually; classification accuracy and overtime/bonus/severance treatment can swing it 10–30%.

• Class code rate — set by the rating bureau, but the class code itself can often be challenged or split.

• Experience modification (EMR/mod) — calculated from your last 3 prior policy years (excluding the most recent); driven by claim frequency and severity vs. expected losses for your class.

• Schedule credits/debits — carrier discretion — typically ±25% — based on safety program quality, management experience, premises, equipment, classification, and medical facilities.

If your business writes $1,000,000 in modified premium and you can shave 0.10 off your mod, you save roughly $100,000 — without changing carriers, without cutting coverage. That's why the rest of this guide spends so much time on the mod.

3. Risk Management Procedures That Actually Move the Premium Needle

Carriers don't reward intentions; they reward written, dated, signed, and audited safety procedures. A risk management program that exists only as a binder on a shelf earns zero schedule credit. A real one earns credit, lowers frequency, lowers severity, and — most importantly — lowers your mod three years from now.

3.1 Written Safety Program

A real written safety program contains these components, all dated and acknowledged by employees:

• Hazard assessment (workplace, by location, by job title)

• Job hazard analysis (JHA) for every position with physical exposure

• Personal protective equipment (PPE) policy with signed receipts

• Lockout/tagout (LOTO) for any equipment with stored energy

• Bloodborne pathogen plan (medical, dental, salon, gym, custodial)

• Hazard communication / SDS (chemicals, cleaners, paints, solvents)

• Heat illness prevention (any outdoor work or hot indoor environments)

• Respiratory protection program (dust, fumes, infectious disease)

• Fall protection (any work above 4 ft general industry / 6 ft construction)

• Powered industrial truck (forklift) certification with retraining every 3 years

• Driver safety / motor vehicle records (MVR) policy

• Workplace violence and active shooter response

• Emergency action plan and fire prevention plan

• Disciplinary policy that ties back to safety violations

3.2 Safety Training

Training is the single most-audited element of a safety program. Carriers and OSHA both want to see who was trained, on what, when, by whom, in what language, and with proof of comprehension (a quiz or signed acknowledgment — not just a sign-in sheet).

• New hire orientation safety training — before any production work; minimum 30 minutes; covered topics aligned to JHA.

• Job-specific training — before independent operation of any equipment, vehicle, or chemical.

• Annual refresher training — for high-frequency loss areas: lifting/ergonomics, slips/trips/falls, vehicle safety, PPE.

• Toolbox talks — 5–10 minute weekly stand-ups documented with sign-in sheets — cheap, effective, audit-friendly.

• Bilingual delivery — if any portion of your workforce is more comfortable in another language. Untrained-because-it-was-in-English is an indefensible claim.

3.3 PPE Program

PPE is regulated under 29 CFR 1910.132. Your program must include a written hazard assessment certifying that PPE is required, employer-provided PPE (with limited exceptions), training on use and limitations, and documented inspection/replacement. The single most common deficiency: no signed certification of the hazard assessment.

3.4 Hazard Assessments and Inspections

Hazard assessments should be done at every location, every time the operation changes materially, and at least annually. Use a written form, take photos, and assign corrective actions with due dates and responsible owners. Track them to closure. The audit trail (assessment → finding → corrective action → verification) is what carriers love to see during a loss control visit.

3.5 OSHA Compliance

Whether you're federal-OSHA or state-plan (CA, MI, NC, WA, etc.), the foundations are the same:

• Maintain OSHA 300, 300A, and 301 logs accurately and post 300A from Feb 1 – Apr 30

• Submit electronic 300A data for establishments ≥250 employees, or ≥20 in high-hazard industries (Form 300/301 for ≥100)

• Report any work-related fatality within 8 hours; in-patient hospitalization, amputation, or loss of an eye within 24 hours

• Keep written required programs (LOTO, HazCom, BBP, RPP, fall protection, PIT, etc.) up to date

• Train and document; nothing exists if it isn't written

• Conduct a mock OSHA inspection annually — your safety committee or broker can lead it

3.6 Return-to-Work (RTW) Program

A written, transitional duty / light duty / modified duty program is the single highest-ROI risk management initiative most businesses can implement. The math is simple: the workers' comp formula in NCCI states penalizes frequency more harshly than severity(because of the split point — see Section 5). Every lost-time claim is exponentially more expensive on the mod than a medical-only claim. RTW converts lost-time claims into medical-only or shorter-duration indemnity claims.

A real RTW program has:

• A written policy distributed to every employee at hire

• A bank of pre-approved transitional duty job descriptions across the company (greeting, inventory counting, light filing, training videos, safety inspections, tool inventory, parts cleaning, customer service callbacks)

• Transitional duty offered in writing within 24–48 hours of release with restrictions

• Coordination with the treating physician — send the job description so they can release back to work

• Maximum transitional period (commonly 90 days) with weekly check-ins

• Documentation: doctor's note, job offer letter, employee acknowledgment, daily timecard, supervisor sign-off

3.7 Ergonomics

Musculoskeletal disorders (MSDs) and cumulative trauma injuries account for roughly one-third of serious work-related injuries in the U.S. (BLS). Ergonomic interventions — height-adjustable desks, lift assists, anti-fatigue mats, mechanical aids, two-person lift policies — pay back fast in reduced frequency.

3.8 Drug-Free Workplace Program

Several states (FL, GA, AL, MS, OH, SC, TN, VA, AR among others) offer a 5–7.5% premium credit for a certified drug-free workplace program. Requirements typically include: written policy, employee education, supervisor training, employee assistance program (EAP) referral, and pre-employment, reasonable suspicion, post-accident, and random testing. Even in non-credit states, a documented drug/alcohol policy supports intoxication defenses on claims.

3.9 Safety Committee

Several states (e.g., OR, WA, MT, MN, NV) require a safety committee at certain headcounts; many others offer premium credit for one. A real safety committee meets monthly, includes rank-and-file employees and management, reviews recent incidents and near-misses, conducts inspections, and drives corrective actions. Document every meeting with minutes, attendance, action items, and closure dates.

3.10 Hiring and Onboarding Discipline

The most effective claim-prevention program starts before someone is hired. Background checks, MVRs for any driving role, post-offer / pre-placement physicals (where ADA-compliant), reference checks, and structured 30/60/90 day check-ins all reduce frequency. Conditional offers contingent on physical exams must be administered uniformly to defend against ADA claims — work with employment counsel.

4. Claims Handling: How to Close Claims Faster and Cheaper

Workers' comp claims behave like wildfires — cheap to extinguish in the first hour, exponentially more expensive every day they're allowed to grow. The difference between a claim closed in 30 days and the same claim closed in 18 months is often 5–20× the cost. Here's the procedure that drives that down.

4.1 Immediate Incident Response (First 60 Minutes)

1. Stabilize and provide medical care. Use a designated occupational medical clinic that knows workers' comp.

2. Secure the scene. Take photos before anything is moved or cleaned up.

3. Identify witnesses and capture statements while memory is fresh.

4. Complete an internal incident report — use a single standard form.

5. Notify the supervisor, HR, and the safety lead.

4.2 Report the Claim Within 24 Hours

Stanford and NCCI studies repeatedly show that claims reported within 24 hours cost 20–40% less than those reported after a week. Late reporting is the #1 source of unnecessary claim cost. Build a one-page workflow that any supervisor can execute, and audit it monthly.

4.3 Investigate Every Claim — Including Medical-Only

Every claim deserves a 4-corners investigation: who, what, when, where, why, witnesses, mechanism, prior conditions, recorded statement (where allowed), photos, and equipment inspection. Even medical-only claims occasionally develop into indemnity claims; an investigation done day 1 is worth 100× the same investigation done day 90.

4.4 Manage the Injured Worker Relationship

The single biggest predictor of claim cost — bigger than injury severity in many studies — is whether the injured worker feels cared for. Call them within 24 hours. Send a get-well card. Keep them on the schedule (transitional duty). Avoid the silence that drives them to a plaintiff's attorney. A claim with an attorney typically costs 2–4× a claim without one.

4.5 Work the Adjuster, Don't Wait for Them

Adjusters carry 100–200 open claims at a time. Yours is not their priority unless you make it one. Set the cadence:

• Acknowledge new claim contact within 48 hours of assignment

• 30-day claim review on every open indemnity claim

• Quarterly claims review meeting on every claim with reserves > $10,000

• Push for IME (independent medical exam) when treatment is plateauing

• Push for nurse case management on lost-time claims early — not at month 6

• Demand monthly reserve reviews — over-reserving inflates your mod

4.6 Reserve Management — The Hidden Mod Driver

Reserves on open claims count toward your experience mod at full value as of the unit statistical date (typically 18 months after policy inception). An over-reserved open claim hits your mod just as hard as paid losses. Get reserves to true exposure, push to close claims before the unit stat date, and dispute clearly excessive reserves with the carrier in writing.

4.7 Settlement Strategy

In most states you can settle workers' comp claims via Compromise & Release (full and final), Stipulation with Request for Award (continuing medical), or Section 32 (NY) / similar. Strategic considerations:

• Settle stale, low-activity claims aggressively — they sit on your mod indefinitely

• Use Medicare Set-Asides (MSAs) properly when CMS thresholds are met to avoid CMS recovery actions

• Time settlements before the unit stat date to keep them off the next mod calculation

• Coordinate with disability buyout, Social Security, and any LTD plans

• Don't over-pay just to close — but recognize a small premium beats years of reserve drag

4.8 Subrogation

If a third party caused the injury (defective equipment, negligent driver, contractor), the carrier has subrogation rights. Recoveries reduce your incurred losses and your mod. Flag every claim with potential subrogation in the first 30 days; carriers miss these constantly when not prompted.

5. The NCCI Experience Modification Deep Dive

Your experience modification factor (mod, EMR, e-mod, x-mod, X-Mod) is the multiplier applied to your manual premium based on your past claim performance. Mod 1.00 is average. 0.85 means you pay 15% less than average for your class. 1.20 means you pay 20% more. The mod is the single biggest controllable factor in your premium.

5.1 Who Calculates It

In NCCI states (most of the country), NCCI calculates and publishes the mod. Independent bureaus calculate in CA (WCIRB), DE, IN, MA, MI, MN, NJ, NY, NC, PA, TX, WI. The math is similar but the formulas vary slightly. Your mod is recalculated annually and applies to the policy effective on or after the rating effective date.

5.2 The Three-Year Rating Period

The mod uses three policy years of data, excluding the most recent completed year. So the mod effective in 2026 uses 2022, 2023, and 2024 claim data (not 2025). That lag is why every claim you have today affects your mod for 3+ years. It's also why aggressive claims management today shows up as mod savings two and three years out.

5.3 Eligibility

You're mod-eligible when your average annual manual premium during the rating period exceeds the state's threshold (commonly $5,000–$10,000 average over 3 years). Below that, you're at unity (1.00) by default.

5.4 The Formula in Plain English

NCCI Mod (simplified)

Mod = (Actual Primary Losses + (Actual Excess Losses × W) + Ballast + (Expected Excess Losses × (1 - W))) ÷ (Expected Primary Losses + (Expected Excess Losses × W) + Ballast + (Expected Excess Losses × (1 - W))) In practice: the mod compares your actual losses to the losses expected for a business your size in your class codes — with primary losses (frequency) weighted more heavily than excess losses (severity).

5.5 Primary vs. Excess Losses — Why Frequency Hurts More

Each individual claim is split into a primary portion (up to the split point) and an excess portion (above the split point). Primary losses count at full weight in the numerator. Excess losses are partially capped and weighted less. This is the single most important fact about the mod:

Frequency Hurts More Than Severity

10 claims of $5,000 each (all primary) damage your mod far more than 1 claim of $50,000 (mostly excess). That's why preventing small claims and managing transitional duty matters more than preventing the rare catastrophic claim — for mod purposes.

5.6 The Split Point

The NCCI split point is the dollar threshold dividing primary from excess losses on each claim. NCCI raised it dramatically over recent years (it sat at $5,000 for decades, then stair-stepped up to $19,500 by 2024 and continues to be inflation-adjusted). The current split point matters because raising the split point makes each claim hit the mod harder on the primary side. Confirm the current split point on your mod worksheet — it's printed at the top.

5.7 Audit Your Mod Worksheet (Step-by-Step)

Roughly 1 in 4 mod worksheets contains an error worth disputing. Get your worksheet directly from NCCI (or your state bureau) every year — don't rely on the carrier copy. Then check:

1. Class codes match your operations and your policy declarations page.

2. Payroll figures agree with your final audited payroll for each year (not estimated).

3. Expected loss rates (ELRs) and D-ratios are the bureau-published figures for the year.

4. Every claim listed actually belongs to you (no other employer's claims, no duplicates).

5. Claim amounts equal current incurred (paid + reserves) on the unit stat date, not stale figures.

6. Closed claims with $0 payments are reported as zero, not at original reserve.

7. Subrogation recoveries have reduced incurred losses.

8. Medical-only claims are reduced to 30% (the ERA — see below).

9. The split point applied is the current bureau split point.

10. The G value, B value (ballast), and W weighting factor align with bureau tables.

5.8 ERA — Experience Rating Adjustment (the Medical-Only Discount)

In NCCI states (and most independent states), the Experience Rating Adjustment reduces the mod-impact of a claim that is medical-only (no lost time / indemnity). Specifically, the loss amount used in the mod calculation is reduced to 30% of the actual amount. This is the math that makes your RTW program so powerful — convert an indemnity claim into a medical-only claim and you cut its mod impact by 70% instantly.

5.9 How to Lower Your Mod (Action List)

• Convert lost-time claims to medical-only via aggressive return-to-work — biggest single lever

• Close every dispute-able claim before its unit statistical date (18 months post-inception)

• Drive reserves on open claims down to true exposure — push for monthly reviews

• Pursue subrogation aggressively on any third-party-caused injury

• Eliminate frequency: focus on slips/trips/falls, lifting, and motor-vehicle which drive small claims

• Audit and dispute the worksheet annually — recover overcharges

• Reclassify miscoded employees (a clerical claim under a $35 rate beats one under a $9 rate)

• Settle stale, idle indemnity files via C&R before the next reporting cycle

• Coordinate with the carrier loss-control rep for documented schedule credits

• Track frequency and severity by location/supervisor — culture moves the mod

5.10 Disputing Your Mod

If your audit finds material errors, file a dispute with the rating bureau. Common dispute types: payroll corrections after final audit, claim reclassification (medical-only vs. indemnity), subrogation recovery not posted, claim assigned to wrong employer, ownership change not properly handled, claim amounts not updated to current incurred. Bureaus will revise the mod retroactively, and your carrier will issue premium refunds — often five and six figures.

6. Premium Audit Preparation — Stop Overpaying at Year-End

Workers' comp policies are based on estimated annual payroll. After the policy expires, the carrier conducts a premium audit to true-up. This is the moment most businesses lose 5–15% of premium they shouldn't have paid — because their books aren't organized to support deductions and exclusions the policy actually allows.

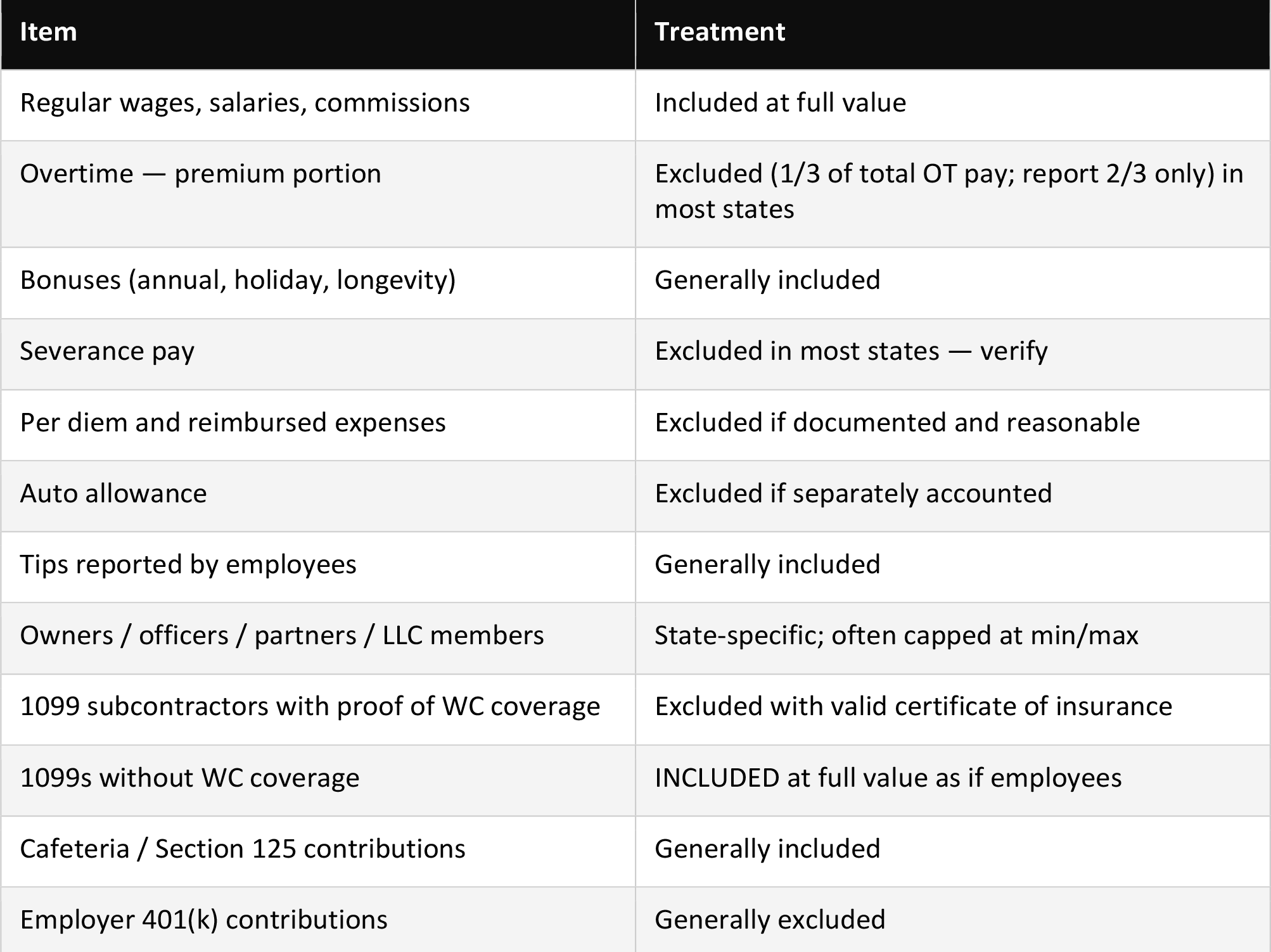

6.1 What's Included in 'Payroll' (and What Isn't)

Payroll includes most employee compensation, but the rules are nuanced and you can lose serious money if you don't claim what you're entitled to. Common rules (state variations apply — confirm in your manual):

6.2 Audit Prep Checklist (Run This 60 Days Before Renewal)

1. Pull payroll detail by class code and by employee for the policy period.

2. Reconcile to your 941s, state UI returns, and W-3 totals.

3. Separate and total overtime premium portion (1/3 of total OT) by class.

4. Identify and exclude excludable items (severance, per diem, 401(k) match, etc.).

5. Apply officer/owner caps for your state — don't let auditors use full payroll.

6. Collect certificates of insurance (COIs) for every 1099 contractor showing valid WC coverage during the audit period.

7. Document who performs which functions — to defend lower-rate class codes for clerical, outside sales, drivers.

8. Prepare a clean audit packet rather than dumping raw QuickBooks reports on the auditor.

6.3 During the Audit

• Always assign one designated person — never let the auditor wander your records

• Provide only what's requested, organized to your narrative

• Walk the auditor through your class code splits before they assume worst-case

• Keep the visit short — long visits find more issues

• Request a draft audit before final issuance — you have a right to dispute

• Reconcile the auditor's numbers to your prepared figures line-by-line

6.4 After the Audit — Dispute Aggressively

Most states require a dispute (formal premium audit appeal) within 90 days. Common winning disputes: misapplied class codes, included excludable items, uncredited COIs for subs, owner/officer caps not applied, double-counting of bonus accruals, OT premium portion not separated. Even if you go from a 5% additional bill to a 5% return premium, that's 10 points back.

7. Class Code Review and Reclassification Opportunities

There are roughly 700 NCCI class codes, each with its own rate. Two employees doing the same job in different class codes can produce wildly different premiums. Class code mistakes are the second-most-common premium overcharge after audit errors.

7.1 The Governing Classification Rule

In most states, a single business is assigned one governing class code representing its primary operations, plus standard exception codes (Clerical 8810, Outside Salespersons 8742, and Drivers 7380 in NCCI; numbers vary by state). You generally cannot split the governing operation across codes — an attempt to put production workers under a clerical code is improper and will be caught on audit.

7.2 Standard Exceptions Worth Capturing

• Clerical Office (8810): purely clerical employees in physically separated office space — among the lowest rates in the manual

• Outside Salespersons (8742): salespeople who work principally away from the employer's premises

• Drivers (7380): employees primarily engaged in operating motor vehicles for the employer

• Telecommuters (8871 in some states): a relatively new and lower-rated code for full-time remote workers

7.3 When to Request Reclassification

• Your operation has materially changed (new product lines, automated processes, new locations)

• You acquired a business and its codes were merged in without analysis

• Your industry's class has been split or revised by NCCI (e.g., warehousing splits in recent years)

• Your test audit reveals employees miscoded under your highest-rate class

• A competitor in similar operations is on a different (lower) code

7.4 How to Get a Code Reviewed

Request an inspection from your carrier, file a Test Audit request with the bureau, or, in some states, file an Application for Reclassification directly. Carriers can also request a Special Inspection from the bureau on your behalf. Document operations with photos, job descriptions, equipment lists, and percentage of time on each task.

8. Choosing the Right Carrier, Agent, and Program Structure

8.1 The Right Agent / Broker

Most businesses pay too much for workers' comp because their broker is a generalist. Workers' comp is its own discipline — full-time specialists deliver materially better outcomes. Look for:

• A broker with at least 25% of book in workers' comp specifically

• Direct relationships with multiple comp markets (10+ carriers)

• In-house claims advocacy and loss control resources, not just a sales rep

• Demonstrated mod-management track record with case studies

• Willingness to put fee compensation in writing (commission disclosure)

• Renewal bid process documented in writing — minimum 3 markets every renewal cycle

8.2 Choosing a Carrier

Underwriting appetite varies wildly by industry, state, and account size. The right carrier for a 5-person professional firm is rarely the right carrier for a 500-person manufacturer. Compare on:

• AM Best rating (A- minimum for most accounts)

• Industry / class code appetite alignment

• Claims handling reputation in your state — talk to other policyholders

• Loss control services (engineers, training, ergonomic assessments — included or extra)

• Premium audit accuracy and dispute handling

• Available program structures (dividend, deductible, retro, group, captive)

• Schedule credit/debit philosophy with this carrier's underwriters

• Use of preferred provider networks for medical and pharmacy

8.3 Dividend Plans

Dividend plans (sometimes called participating plans) return a portion of premium when loss experience is favorable. Common in mutual carriers and association programs. Typical dividend: 5–25% of premium, paid 12–18 months after policy expiration. Not guaranteed — declared at carrier discretion based on group or account performance. Best for stable, low-loss accounts that don't need cash flow now.

8.4 Group / Association Programs

Group programs aggregate similar businesses (often through a trade association) into a single rated unit. Benefits: shared loss control, group dividend, group purchasing power, better access to specialty carriers. Risks: your premium is partly hostage to other members' losses, exit can be expensive. Worth exploring if a strong association exists in your industry.

8.5 PEOs (Professional Employer Organizations)

A PEO co-employs your workforce and provides workers' comp under their master policy. Pros: access to coverage when you can't get a standalone policy, immediate compliance, potentially lower mod by joining a larger pool. Cons: opaque cost structure (admin fees blended in), loss of direct mod management, exit complications, regulatory variation by state. Best for: small businesses with high mods, hard-to-place industries, or businesses without HR/risk infrastructure. Read the agreement carefully — many PEO clients overpay vs. a standalone policy with proper management.

8.6 Captives

A captive is an insurance company that you (and possibly other members) own. You fund the predictable loss layer; reinsurance covers catastrophic losses; underwriting profits and investment income flow back to you instead of the carrier. Three flavors:

• Single-parent captive — you own it; large premium accounts ($1M+) only.

• Group captive — you own a share alongside other carefully selected members; common at $200K–$1M+ premium.

• Cell captive (Series LLC / segregated cell) — rented cell within a larger captive structure; lower entry threshold.

Captives reward best-in-class risks. If you're a low-mod, well-managed account, you're subsidizing your carrier's losses on worse risks under a guaranteed-cost program — captives recapture that subsidy. They demand sophisticated risk management and patience for the cash to recycle.

8.7 Self-Insurance

Qualified self-insurance is allowed in most states for businesses meeting net worth, liquidity, and bonding requirements (typically $5M+ net worth, plus a surety bond or letter of credit). You pay claims directly through a third-party administrator (TPA) and buy excess insurance for catastrophic claims. Benefits: maximum control, no carrier profit margin, full investment income on reserves. Costs: high administrative complexity, regulatory filings, security deposits, and direct exposure to bad years. Generally not appropriate below $1M annual claim spend.

9. Deductible and Retention Strategies

Most workers' comp policies are written guaranteed-cost (no deductible). Deductible plans transfer some of the working layer of losses back to the insured in exchange for a lower premium. Common structures:

• Small / medical-only deductible — $500–$2,500 per claim, often medical-only; modest premium credit (3–7%); easy to administer; reduces frequency of small claims clogging the system.

• Per-claim deductible — $5,000–$25,000 per claim; you pay the first dollars and the carrier pays above; meaningful premium credit (10–20%); requires cash flow to fund losses.

• Aggregate deductible — you pay all losses up to an annual aggregate stop-loss; carrier pays everything above; substantial credit but real downside.

• Large deductible — $100,000+ per claim; designed for accounts with $1M+ premium; substantial credit; usually paired with collateral requirements (LOC, surety).

Run the math: for a deductible plan to make sense, the present value of expected retained losses + administrative cost + collateral cost must be less than the premium credit. With a low-mod, low-frequency account, the math is highly favorable.

10. Loss-Sensitive Plans: Retro, Large Deductible, Captive

Loss-sensitive plans price your premium based on actual losses (after the fact) rather than estimated losses (in advance). The two most common:

10.1 Retrospective Rating (Retro) Plans

Premium is adjusted up or down after the policy expires based on actual losses, subject to a minimum premium and a maximum premium. Typically computed at 6, 18, and 30 months post-expiration, then closed out (or held open until losses fully develop). Common variations:

• Incurred-loss retro: based on incurred (paid + reserves) losses

• Paid-loss retro: based only on paid losses — better cash flow on long-tail claims

• 1-year, 2-year, 3-year retros: longer maximum periods give a smoother result

• Insured-paid loss retro vs. carrier-paid retro: who fronts the dollars matters for cash flow

10.2 Large Deductible Plans

Often more cash-flow friendly than retros for accounts with $500K+ premium. The carrier pays claims and bills you back the deductible portion. Collateral (LOC or surety) usually required. The carrier still gets credit for paying the claim through the network and managing the file.

10.3 When Loss-Sensitive Plans Make Sense

• Premium ≥ $250K (some markets) or $500K+ (most retros)

• Strong, documented safety culture and low mod (≤ 0.90)

• Low frequency, predictable losses

• Cash flow available to fund retained losses

• Risk management and claims oversight resources

• Multi-year commitment to the program — early exits can be punitive

11. Wellness Programs and Their Real Premium Impact

Wellness is overhyped on direct WC premium credit (only a handful of carriers offer formal credits) and underhyped on indirect impact. Healthier employees recover faster from injuries, take less time off, are less likely to develop comorbid conditions during a claim, and have lower frequency of soft-tissue claims. The best-leverage wellness components for workers' comp are:

• Pre-shift stretching and flexibility programs (cuts soft-tissue frequency)

• Tobacco cessation (smokers heal slower; cessation cuts comorbidity costs)

• Diabetes management and obesity intervention (large comorbidity multiplier on claim cost)

• Mental health / EAP access (depression and anxiety are top claim-extension drivers)

• Sleep hygiene and fatigue management (especially for shift workers and drivers)

• Physical therapy access — make first-touch PT available without an MD referral

Document everything. Even when there's no formal premium credit, schedule credit at underwriting renewal often comes with proof of a serious wellness program.

12. Documentation and Record-Keeping Best Practices

Insurance is a documentation business. The reason two identical-looking businesses get wildly different premiums is that one of them can prove its safety culture and the other can't. Build a single risk management binder (digital — not paper) that includes:

12.1 Policy and Premium File

• All policy declarations, endorsements, and applications (5+ years)

• Annual mod worksheets from the rating bureau (10+ years)

• Premium audit workpapers and final audits (5+ years; longer if disputed)

• Carrier loss runs (5+ years; pull a fresh one annually)

• Schedule credit / debit documentation

• Renewal proposals and competing quotes

12.2 Safety File

• Written safety programs with revision history

• Training records by employee (topic, date, instructor, language, comprehension proof)

• Hazard assessments and inspection reports with closure documentation

• Safety committee minutes and attendance

• Toolbox talk records

• Equipment inspection logs

• PPE issuance records and signed receipts

• OSHA logs (300, 300A, 301) — 5 year retention

12.3 Claims File (per claim)

• Internal incident report

• Witness statements

• Photographs of scene, equipment, PPE

• First report of injury (DWC-1, Form 101, etc.)

• Medical authorization and provider records

• RTW offer, doctor's release, transitional duty timecards

• Subrogation investigation

• Adjuster correspondence and reserve change history

• Settlement documents

• Closure confirmation

12.4 HR / Payroll File

• Job descriptions reflecting actual physical requirements

• Time and payroll records by class code

• 1099 contractor agreements and certificates of insurance

• Owner/officer election forms (inclusion or exclusion)

• Multistate payroll reports

Putting It All Together

Workers' compensation is not a fixed expense — it's a managed expense. The businesses that pay the least don't get lucky. They run the playbook in this guide every quarter: they know their mod, they audit their worksheet, they prepare for premium audit, they investigate every claim within 24 hours, they offer transitional duty in writing, they document everything, and they treat their carrier and broker as partners (or replace them).

Pick three items from this guide and execute them in the next 90 days. Then pick three more. Most businesses save 10–25% in 12 months and 25–40% over 36 months. The best-managed accounts run mods at 0.55–0.75 — and pay literally half what their unprepared competitors pay for the same coverage.

Need help auditing your mod or restructuring your program?

Akker, LLC specializes in workers' compensation insurance for businesses that want to actually lower the cost — not just renew it. We audit mod worksheets, restructure programs, run claims advocacy, and bid renewals across 10+ carriers. Reach out at info@akkerins.com or visit akkerins.com to start a no-cost mod and program review.

13. FAQ — Workers' Comp Insurance for Businesses

What is a good workers' comp experience modification rate?

A mod below 1.00 is better than the industry average for your class. Best-in-class accounts run 0.60–0.85. Anything above 1.10 means your business is paying more than your peers and is a strong signal you have a controllable cost problem.

How is workers' comp premium calculated?

Manual premium = (payroll ÷ 100) × class code rate. Modified premium = manual × experience mod. Final premium = modified × schedule credits/debits × premium discount × expense constant ± surcharges. Three of those four inputs are within your control.

How can I lower my workers' comp insurance cost?

The fastest levers are: report claims within 24 hours, run a written return-to-work program, audit your NCCI mod worksheet annually, prepare aggressively for premium audit, and review your class codes. Combined, these typically move premium 10–30% within 24 months.

What is the NCCI experience modification rate (EMR)?

It's a multiplier (around 1.00) applied to your manual premium that reflects your past three years of claim experience versus the average for your class codes. Below 1.00 means you pay less than average; above 1.00 means you pay more.

What is the difference between primary and excess losses on the mod?

Each claim is split at the bureau split point. The portion below the split point is 'primary' and counts at full weight in the mod formula. The portion above is 'excess' and is partially capped and weighted less. That's why frequency hurts the mod more than severity.

What is a return-to-work program and why does it matter?

It's a written program that brings injured employees back in transitional duty roles before full release. It converts indemnity (lost-time) claims into medical-only claims, which the NCCI Experience Rating Adjustment reduces to 30% of value in the mod calculation — typically a 70% mod-impact reduction per converted claim.

How do I prepare for a workers' comp premium audit?

Reconcile payroll by class code to your 941s and W-3s, separate the overtime premium portion (1/3) from straight time, exclude allowable items (severance, per diem, 401(k) match), apply officer/owner caps, gather certificates of insurance for every 1099, and provide an organized audit packet to the auditor.

Should I use a PEO for workers' comp?

PEOs are useful for hard-to-place businesses, very small employers without HR infrastructure, or businesses with unmanageable mods. Larger or well-managed accounts often pay more inside a PEO than they would standalone with disciplined mod management. Always run the math both ways.

What is a workers' comp captive?

A captive is an insurance company that you (and sometimes other businesses) own. You fund the working layer of losses; reinsurance handles catastrophes; underwriting profit and investment income flow back to you. Best-fit at $250K+ premium with strong safety performance.

Can I dispute my experience mod if it has errors?

Yes. File a dispute with NCCI or your state bureau. Common winning disputes: payroll corrections after final audit, claim reclassifications, subrogation recoveries not posted, claims assigned to the wrong employer, and ownership change errors. Bureaus revise the mod retroactively and the carrier issues premium refunds.