Your Client Just Sent a Contract Requiring a Waiver of Subrogation and an Alternate Employer Endorsement. Now What?

Two endorsements. Two contract requirements you are seeing more of than ever. Here is exactly what they do, why clients are demanding them, and what happens to your staffing agency if your workers' comp policy does not have them.

It lands in your inbox on a Tuesday morning. A new client contract. You scroll to the insurance requirements page and see two lines that you may not have dealt with before — or maybe you have, and you are not entirely sure your current policy actually covers them:

"The staffing vendor shall provide a Waiver of Subrogation in favor of [Client Company] on its Workers' Compensation policy."

"The staffing vendor shall provide an Alternate Employer Endorsement naming [Client Company] as an Alternate Employer on its Workers' Compensation policy."

These two requirements are appearing in staffing contracts at a rate I have not seen in my 15 years of working exclusively with staffing agencies. Enterprise clients, national logistics companies, hospital systems, manufacturing operations, and even mid-size businesses have started inserting both requirements as standard boilerplate — the same way they started requiring additional insured status on general liability policies ten years ago.

If you do not have them, you do not get the contract. It is that simple. And if your policy has not been reviewed recently, there is a real chance you are signing contracts you cannot actually fulfill from an insurance standpoint.

This blog breaks both endorsements down clearly — what they do, why your clients are demanding them more than ever, what the hidden risk is if you do not have them, and exactly what to check on your current workers' comp policy today.

Why These Two Requirements Are Everywhere Right Now

Before I explain what each endorsement does, it is worth understanding why the market shifted. Because five years ago, I could go weeks without a client mentioning either of these. Now I see them in contracts almost daily.

Three things drove this change:

1. The Litigation Environment Tightened

Workplace injury litigation costs have climbed consistently since 2022. Employers hosting temporary workers from staffing agencies started getting pulled into lawsuits they thought were not their problem — injured temp workers suing the host company directly because workers' comp exclusivity protections did not clearly apply to them at the host site. Legal teams at enterprise companies noticed and updated their vendor contract templates.

2. OSHA's Joint Employer Guidance Expanded

OSHA has consistently reinforced that when a staffing agency places workers at a client site, both the staffing agency and the host employer share responsibility for workplace safety. That shared safety responsibility translates directly into shared liability exposure — and enterprise clients responded by requiring the insurance documentation to match the legal reality.

3. Risk Management Departments Got Smarter

Corporate risk managers and procurement teams at larger companies have become significantly more sophisticated about supply chain insurance requirements since 2020. What used to be reviewed by a single procurement officer is now being run through centralized risk management checklists. Those checklists include both endorsements. If your COI does not show them, your agency gets kicked off the approved vendor list.

📋 Stan's direct observation:

In 2026, I would estimate that 60-70% of new staffing contracts I review from enterprise and mid-market clients include at least one of these two requirements — and approximately 40% require both. Three years ago those numbers were closer to 20% and 10%. This is not a trend. It is the new standard.

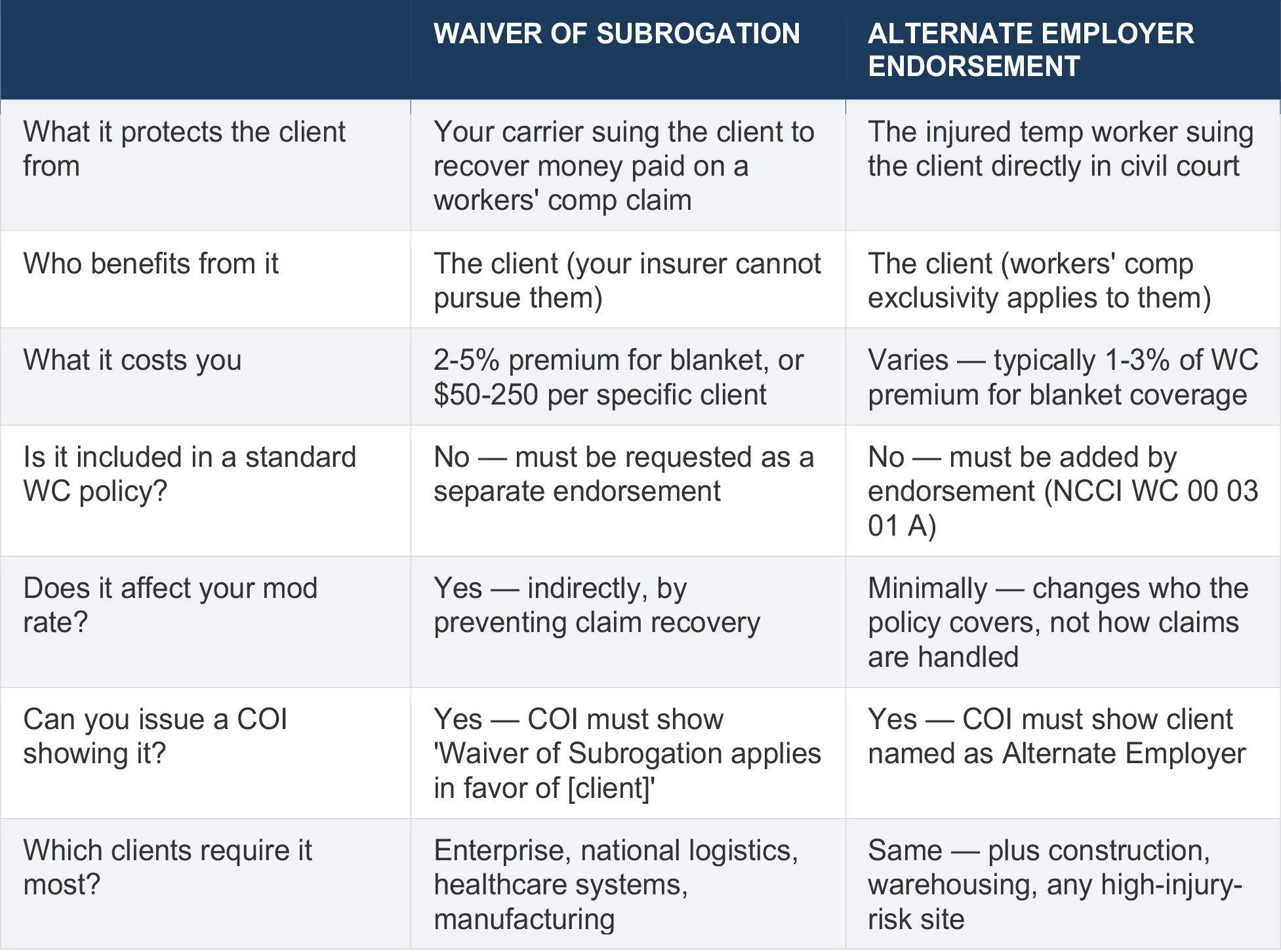

The Waiver of Subrogation — What It Actually Does

Start With Subrogation Itself

To understand the waiver, you first need to understand what subrogation is. Subrogation is the legal right your workers' compensation insurance carrier has to recover money it paid on a claim from the party that actually caused the injury.

Here is the scenario in a staffing context: Your temp worker — let's call him Marcus — is placed at a client's warehouse. While working there, Marcus is injured when a forklift operated by one of the client's own employees strikes him. Your workers' comp carrier pays Marcus's medical bills and lost wages. Now your carrier's legal team looks at the situation and determines that the client's forklift operator caused the injury through negligence. Under standard subrogation rights, your carrier can now sue the client company to recover what it paid Marcus.

That lawsuit does not help Marcus, who already received his benefits. It is purely a financial recovery mechanism for your insurer. But it can absolutely destroy your business relationship with that client.

The Waiver of Subrogation Removes That Right

Definition: A Waiver of Subrogation endorsement on your workers' compensation policy is a contractual agreement in which your insurance carrier gives up its right to sue a third party — in this case, your staffing client — to recover money it paid on a workers' comp claim, even if that third party's negligence caused the injury.

When you add this endorsement and your client is named in it, your carrier is agreeing upfront that it will pay the claim and will not pursue the client for reimbursement — regardless of what happened. The client is protected from your carrier's subrogation action.

This is why your clients want it. Their risk managers do not want to be sued by your insurance company for an injury that occurred on their site — even if their own employee contributed to the accident. The waiver closes that door before it ever opens.

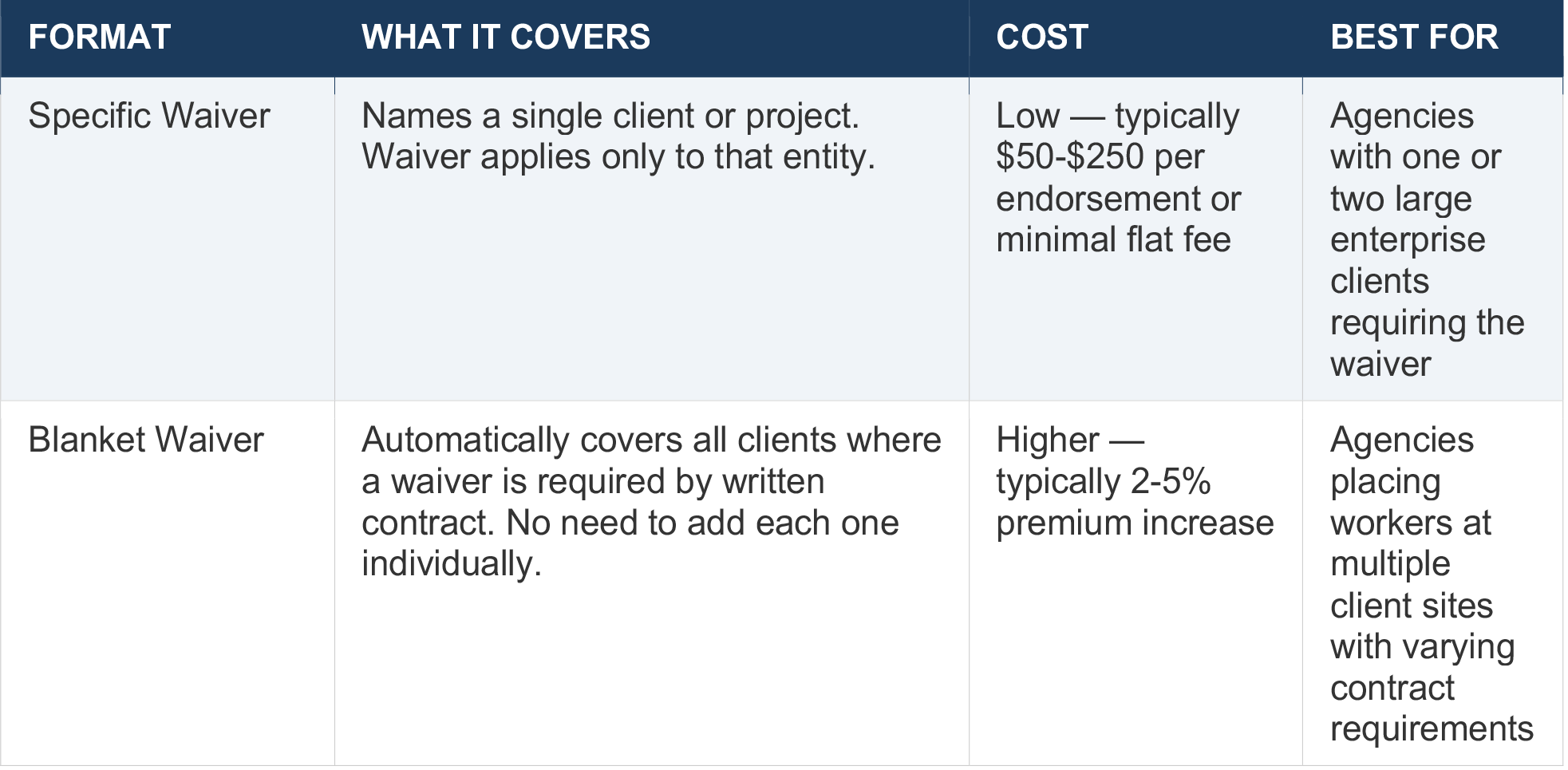

The Two Formats — Specific vs. Blanket

The Hidden Cost That Most Agencies Miss

Here is what your carrier will not volunteer at renewal: when a waiver of subrogation is in place and your carrier pays a claim it cannot recover from the responsible party, that full claim amount stays on your loss history. No recovery means the claim costs live on your experience modification rate for the full three-year look-back period.

Real dollar impact: A $50,000 workers' comp claim with no waiver in place gives your carrier the option to recover those funds from the at-fault third party. Successful recovery can reduce or eliminate that claim's impact on your experience mod. The same $50,000 claim with a blanket waiver in place stays on your record in full — and at a mod multiplier of 1.20, that one claim is costing you an extra $10,000 per year in premium for three years. That is $30,000 in compounding premium impact from a single unrecovered claim.

This does not mean you should refuse to sign contracts requiring a waiver. Losing the contract costs more than the mod impact in most cases. But it does mean you should know the trade-off you are making, and you should be managing your loss prevention program aggressively at every client site where a waiver is in place.

The Alternate Employer Endorsement — What It Actually Does

The Coverage Gap It Closes

When your staffing agency places a temp worker at a client's facility, two employers are involved in that worker's daily job. Your agency employs the worker — you handle payroll, you carry the workers' comp policy. But the client company is directing the work — they control the site, set the schedule, and supervise the actual tasks being performed.

Here is where a dangerous gap opens: if that temp worker is injured on the client's site, workers' comp is supposed to be the exclusive remedy — meaning the injured worker receives benefits through the comp system and cannot separately sue the employer for additional damages. But the question is: does that exclusivity protection extend to the client company, or only to your staffing agency?

Without an Alternate Employer Endorsement, the answer is often no. The temp worker may be able to sue the client company directly in civil court — bypassing the workers' comp system entirely — because the client is not technically the employer of record. That lawsuit can result in damages far exceeding what workers' comp would have paid, with no insurance policy from the client's side required to respond.

What the Endorsement Does

Definition: The Alternate Employer Endorsement (NCCI Form WC 00 03 01 A) adds the client company to the staffing agency's workers' compensation policy as an alternate employer. It extends both Part One (workers' compensation benefits) and Part Two (employer's liability) of the staffing agency's policy to cover the client as if the client were the named insured under the policy.

The practical result: Workers' comp becomes the exclusive remedy for the injured temp worker against both the staffing agency AND the client. The worker gets their benefits through the comp system. The client cannot be separately sued for additional civil damages. One policy, one insurer, one outcome.

This is exactly what your client's risk manager is protecting against. They want the legal shield of workers' comp exclusivity to apply to their company the same way it applies to your staffing agency. The Alternate Employer Endorsement gives them that protection — and it can only come from you, the staffing agency that holds the workers' comp policy.

What It Does NOT Do — Critical Distinction

This is where I see the most confusion in client conversations. The Alternate Employer Endorsement does NOT:

• Replace the client's own workers' comp policy.The AEE does not satisfy the client's independent legal obligation to carry workers' comp for their own direct employees. They still need their own policy.

• Make the client liable for your staffing agency's premium.All premium for the AEE is owed by your agency as the named insured. The client pays nothing.

• Cover the client's own employees.The endorsement covers only the staffing agency's placed workers while working at the client's site. The client's direct hire employees are not affected.

• Override state law requirements.Some states have specific restrictions on how AEEs can be used. Multi-state placements need to be reviewed state by state.

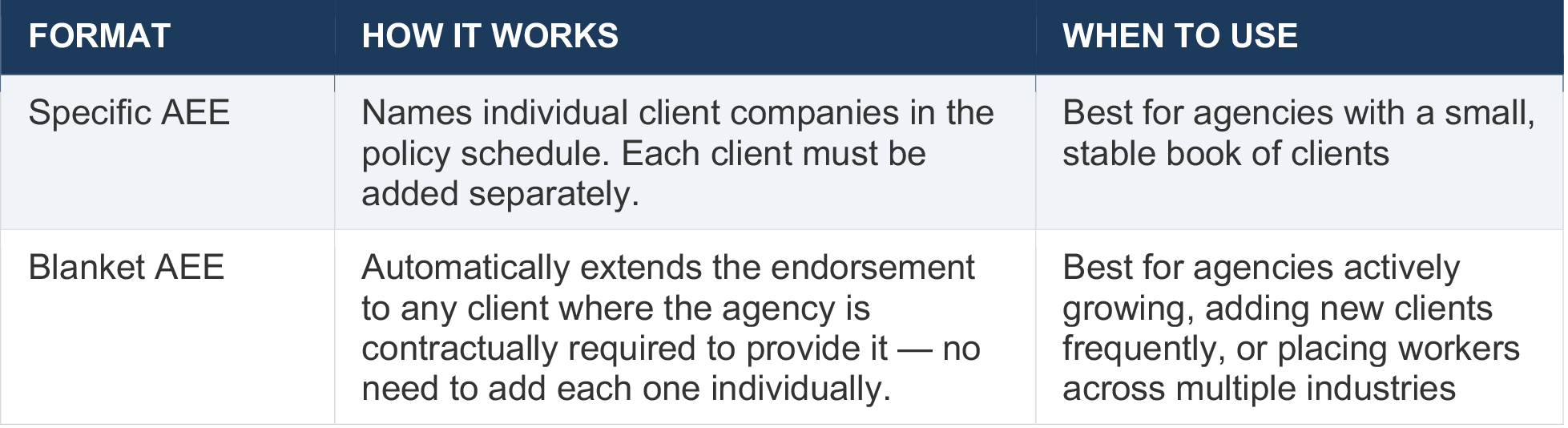

Specific vs. Blanket — and Why Blanket Is the Right Move for Growing Agencies

My strong recommendation for most staffing agencies: if you are growing and adding new clients regularly, negotiate a blanket AEE into your workers' comp policy at inception or renewal. The premium difference is modest. The operational headache of adding specific clients one at a time — especially when a contract has a 48-hour turnaround requirement — is significant. I have seen agencies lose contract opportunities because they could not get the AEE certificate issued fast enough.

Side-by-Side — What Each Endorsement Does for Your Client

What to Check on Your Current Workers' Comp Policy Right Now

Before you sign another client contract with either of these requirements, here is your five-point checklist. Pull out your current WC policy — or call your broker — and verify each of these:

1. Does your policy include a Waiver of Subrogation endorsement?Look for the endorsement on the policy's endorsement schedule — not the declarations page. Check whether it is a specific or blanket waiver. If it is specific, confirm the client requiring it is listed.

2. Does your policy include an Alternate Employer Endorsement?Look for NCCI Form WC 00 03 01 A in your policy documents. Same check — is it specific (listing named clients) or blanket? If specific, are all current client requirements covered?

3. Do your Certificates of Insurance reflect both endorsements correctly?A COI that does not specifically reference the Waiver of Subrogation and the Alternate Employer Endorsement — with the client named correctly — is not compliant with the contract requirement, even if the endorsements exist on the policy. Check your standard COI template.

4. Is your carrier willing to issue both?Not all workers' comp carriers will issue both endorsements — especially the AEE — for agencies in the assigned risk market or high-hazard classifications. If you are with an assigned risk carrier, you need to verify this specifically. Some states also restrict AEE issuance.

5. Is your policy in a state that allows waivers of subrogation on WC?Most states allow it, but requirements vary. A few states have restrictions on the form or scope of the waiver. If you are placing workers in multiple states, your broker needs to confirm compliance state by state.

⚠️ The most common mistake I see:

A staffing agency has a blanket waiver of subrogation on their general liability policy — and assumes it applies to their workers' compensation policy as well. It does not. These are separate policies with separate endorsements. A waiver on your GL does not create a waiver on your WC. You need both, separately, if your client's contract requires them on both lines.

Need to Verify Your Endorsements Before Signing Your Next Contract?

Akker LLC works exclusively with staffing agencies on workers' compensation and staffing liability insurance. If you have a contract in front of you requiring a Waiver of Subrogation or Alternate Employer Endorsement — or you want to verify your current policy has both in place — contact us today.