Why Your Film's Weapons Scene Could Void Your Entire Production Policy

What the Rust case taught insurance carriers — and what every indie producer needs to know before cameras roll in 2026.

On October 21, 2021, a live round fired from a prop gun on the set of the film Rust killed cinematographer Halyna Hutchins and wounded director Joel Souza. The armorer, Hannah Gutierrez-Reed, was convicted of involuntary manslaughter and sentenced to 18 months in prison. Rust Movie Productions was fined $136,793 — the maximum allowable under New Mexico law — for willful firearms safety failures.

The criminal cases are largely concluded. But for the film insurance industry, the Rust case is far from over. It permanently changed how carriers underwrite firearms on film sets — and for indie productions under $1 million, some carriers have simply stopped writing the coverage at all.

If your script has a scene with a real gun, here is what you need to know before you apply for production insurance in 2026.

The Line That Should Concern Every Producer

During the OSHA investigation into the Rust shooting, the state's bureau chief delivered a finding that deserves to be read by every film producer who has ever held a firearms safety policy in their hands:

"Rust Movie Productions identified a hazard. They adopted firearms safety policies, but they totally failed to enforce them, train their employees on them, practice them, reference them. Nothing. They adopted it, and it stopped at the word adoption."

— Lorenzo Montoya, New Mexico Occupational Health and Safety Bureau

That quote is not just a safety lesson. It is an insurance story.

When an incident occurs on set and a carrier investigates a claim, the first thing their legal team looks for is exactly what OSHA found on Rust: a gap between what the policy said the production would do and what the production actually did. That gap is called a material misrepresentation — and it can void your entire policy, not just the firearms portion.

You can have a $6 million production insurance policy, like Rust did, and still face a situation where your carrier declines to pay because your documented safety procedures were not followed in practice.

What Changed for Carriers After Rust

Before October 2021, most production insurance applications asked general questions about stunts, pyrotechnics, and unusual hazards. Firearms were often included in a catch-all category. After Rust, that changed materially.

Carriers across the entertainment insurance market began adding specific firearms underwriting questions to production applications. Some updated their policy exclusion language. Others changed their underwriting appetite entirely.

Here is what the market looks like for indie producers in 2026:

Sub-$1M Productions:

Multiple carriers have exited this segment for productions using real firearms with live rounds or blanks. If your budget is under $1 million and your script requires real guns, your broker pool is significantly smaller than it was four years ago.

$1M–$5M Productions:

Coverage is available but comes with heightened documentation requirements, higher deductibles for firearms-related claims, and specific armorer credential verification.

All Productions in California (As of January 1, 2025):

California SB 132 — the nation's first state-level film safety law, signed by Governor Newsom — now requires all productions using firearms or blanks to have a licensed armorer, property master, or assistant property master holding a current California DOJ entertainment firearms permit. Productions receiving California tax credits must also hire an independent safety advisor starting July 1, 2025.

The Underwriting Questions Carriers Are Now Asking

When you apply for film production insurance in 2026 and your production involves firearms, expect your broker to be asked — and to ask you — the following questions. These did not routinely appear on applications before Rust. They do now.

About Your Armorer

• Does the production have a dedicated, licensed armorer assigned exclusively to firearms duties?

• Is the armorer's only responsibility firearms, or are they also serving as a prop assistant or in another dual role?

• Has the armorer completed state-required training and do they hold a current California DOJ entertainment firearms permit (if filming in California)?

• Can you provide the armorer's credentials before the policy is bound?

About Your Weapons Protocol

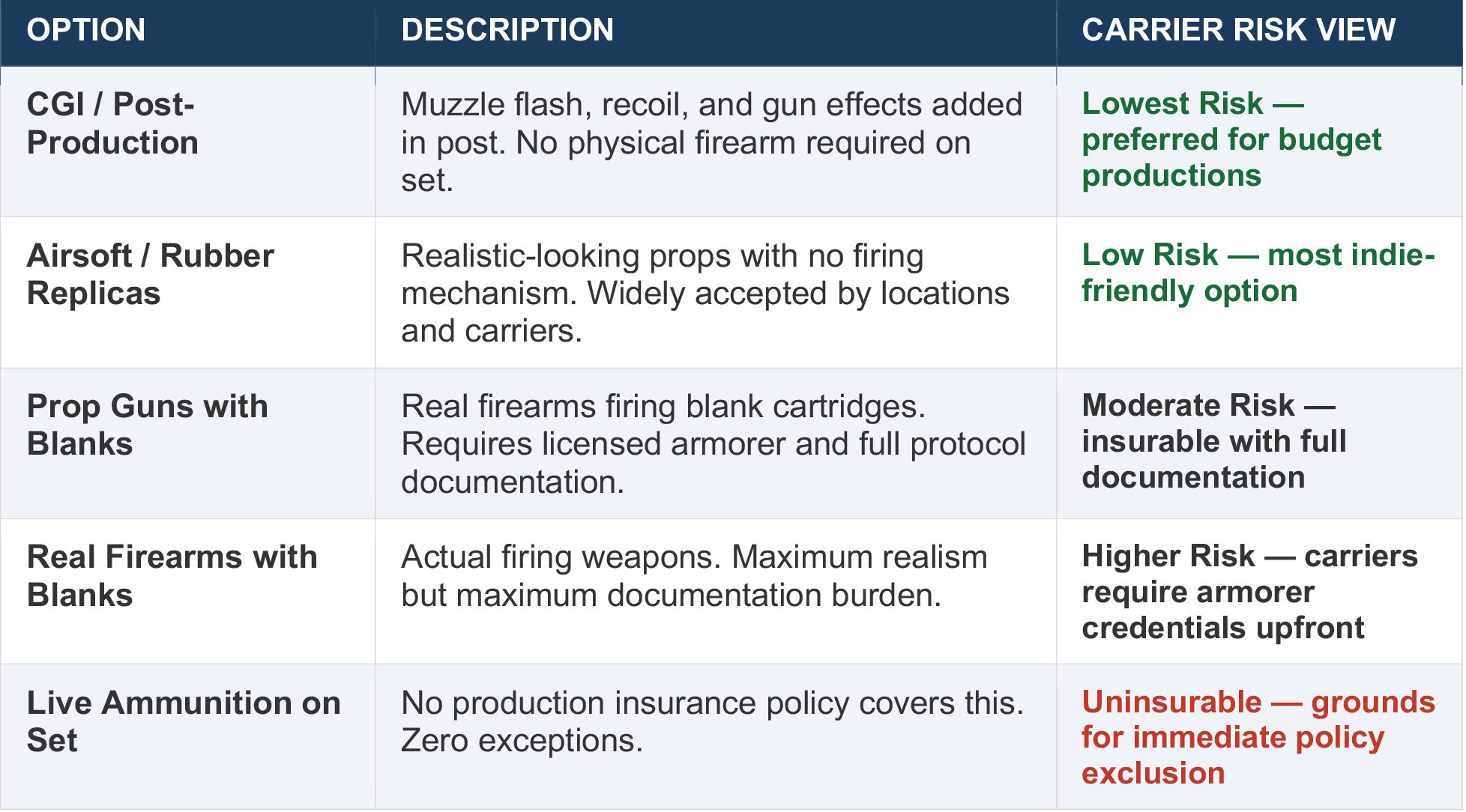

• Will the production use real firearms, replica/prop firearms, airsoft replicas, or CGI post-production effects?

• If real firearms are used, will live ammunition ever be present on set in any capacity?

• Does the production have a written firearms safety protocol? Is it signed by the armorer, property master, and the first AD?

• Are daily safety meetings held on any day when firearms are present on set?

• What is the chain of custody for firearms between scenes — who holds the weapon, how is it stored, and who verifies its status before any actor handles it?

About Your Documentation

• Is there a written risk assessment for every scene involving firearms, completed during pre-production?

• Are firearms handling incidents — including unintentional discharges — documented and reported immediately to the production's safety coordinator?

• Does the production maintain a logbook of every time a firearm is loaded, unloaded, transferred, or handled on set?

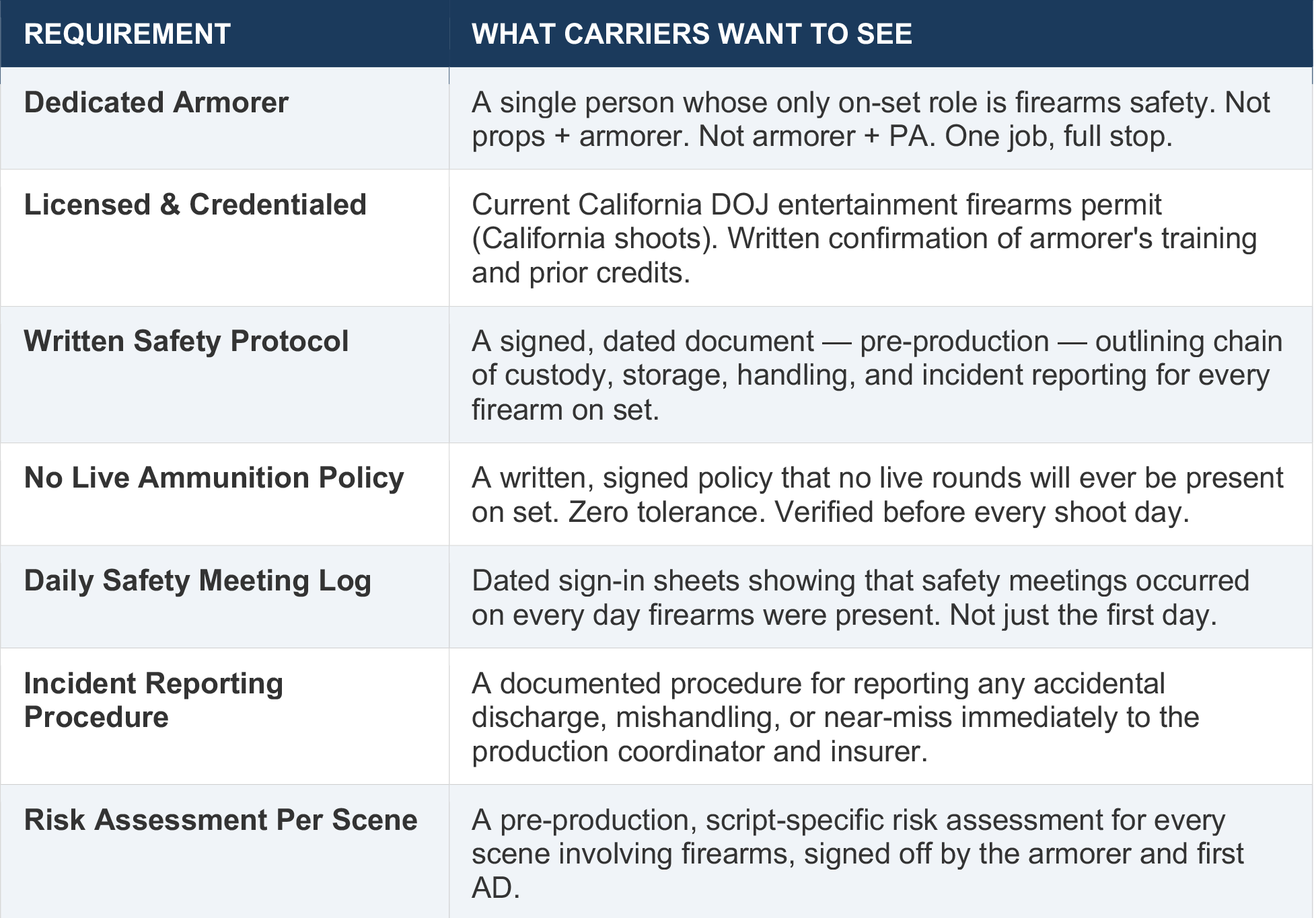

What the Right Answers Look Like

Getting coverage is not just about answering these questions — it is about being able to document your answers. Carriers are not looking for you to say the right things on an application. They are looking for proof that your production actually operates the way your application says it does.

Here is what a properly documented firearms protocol looks like for an indie production:

The Policy Voiding Scenario Every Producer Needs to Understand

Here is the scenario that keeps entertainment insurance brokers up at night:

A production applies for coverage, checks every box on the application, and receives a policy. The producer prints out a firearms safety document, hands it to the armorer, and considers the obligation fulfilled. The armorer — who is also doing double duty in the props department — does not run safety meetings consistently. There is no sign-in log. There is no chain of custody record. The firearms are stored in an unlocked case between scenes.

On day 11 of a 14-day shoot, there is an incident.

The carrier investigates. What they find is exactly what OSHA found on Rust: the production adopted a policy and it stopped at the word adoption. The application said one thing. The set operated differently. That gap — between the represented protocol and the actual protocol — is the grounds on which a carrier denies the claim and voids the policy for material misrepresentation.

This is not theoretical. Rust carried a $1 million general liability policy plus a $5 million commercial umbrella — $6 million in total coverage. Wikipedia notes that the carrier's obligation to pay was in question precisely because of how the investigation characterized the negligence. Documentation failures do not just reduce claims. They can eliminate coverage entirely.

Alternatives Carriers Now Actively Recommend

Because of the Rust aftermath, many carriers now include language in their production policies explicitly recommending or requiring alternatives to real firearms for budget productions. Here is what the market considers the risk hierarchy:

What Producers Need in Place Before Applying for Coverage

If your production includes any scene with a real firearm — or even a highly realistic prop — here is the documentation checklist your broker will need before submitting your application to underwriters:

1. A written firearms safety protocol — dated and signed by the armorer, property master, and first AD — before the application is submitted, not after.

2. Armorer credentials on file — name, current permit numbers (California DOJ entertainment firearms permit if shooting in CA), prior film credits, and confirmation of exclusive role on the production.

3. A no-live-ammunition policy — signed by the armorer, the producer, and the first AD, explicitly stating that no live rounds of any caliber will be permitted on set at any time.

4. A scene-by-scene firearms risk assessment — completed during pre-production based on the script, identifying every scene, the type of firearm, the number of crew members present, and the safety protocols for that specific scene.

5. A chain of custody procedure — specifying where firearms are stored (locked, separately from any ammunition), who has access, and the check-in/check-out process before and after each scene.

6. A daily safety meeting procedure — with sign-in documentation confirming that a safety briefing covering firearms occurred on every production day when weapons were present on set.

Does Your Production Have a Firearms Coverage Gap?

Akker LLC works exclusively with film and production companies. We know which carriers still write firearms coverage for indie productions, what documentation they require, and how to build a submission that gets your policy bound — not declined.

Productions over $1M: Use our film quote app at akkerins.com/film-quote-app

Short-term productions under $1M: akkerins.com/short-term-film-insurance