Film Production Insurance: The Complete 2026 Guide to Coverage, Costs, Risk Management & Claims

Quick Answer

Film production insurance is a bundled program — a Producer's Package (cast, equipment, props/sets/wardrobe, media, location damage, extra expense, civil authority) plus general liability and specialty coverages — required before any production can rent gear, sign locations, or get greenlit. In 2026, an indie short runs $1,200–$2,500; a mid-budget feature runs $15,000–$45,000; annual DICE policies start around $5,000; episodic shops pay $55,000–$200,000+.

Key Takeaways

• The Producer's Package bundles seven first-party coverages; add general liability and you have the spine of every U.S. production insurance program.

• 2026 cost ranges: $1,200–$2,500 (indie short), $15K–$45K (indie feature $1M–$3M), $60K–$150K+ ($5M–$10M feature), DICE from $5K/yr, annual scripted from $4,500/yr.

• Three structures exist — annual, DICE, and short-term project — and choosing wrong costs money on every production for the life of the company.

• The first sixty minutes after an incident determine whether a claim resolves cleanly or becomes a six-figure dispute.

Post-Rust firearms rules, 2025 wildfire repricing, completion-bond restructuring, and AI clauses in E&O have materially changed underwriting in 2026.

What Is Film Production Insurance?

Film production insurance is the bundled coverage program that protects a film, television, or commercial production against the financial losses of equipment damage, cast unavailability, location damage, shutdowns, injuries, and lawsuits.

Film and television production is one of the most insurance-dependent industries on earth. A single scripted streaming episode moves more equipment, people, vehicles, locations, and contractual obligations in eight weeks than most small businesses handle in a decade. Insurance is not a back-office line item — it is the structural element that lets the production exist. If the coverage is wrong, the studio will not greenlight, the network will not deliver-clear, the bank will not lend, the bond company will not bond, and the distributor will not pay.

This guide is built for the people who actually carry the risk: independent producers, line producers, UPMs, production accountants, production counsel, and in-house risk managers. It is the conversation we have at Akker before a shoot starts, condensed into a document you can hand a director, a 1st AD, or a financier.

What's Inside the Producer's Package?

The Producer's Package is the core bundled production policy — seven first-party coverages written as a single account on an inland-marine form, so coverage follows your gear and operations from location to location.

1. Cast Insurance (Essential Element Coverage)

Cast Insurance protects the production when a declared cast member or director cannot commence, continue, or complete work because of death, injury, sickness, or kidnapping. It reimburses the extra expense of the absence: idle crew costs, equipment rental during shutdown, location holds, replacement-actor fees, and reshoots.

The Cast Medical Examination is the underwriting backbone — every declared person needs one through a carrier-approved physician 2–4 weeks before principal photography, and undisclosed pre-existing conditions are universally excluded. Other standard exclusions: hazardous activities not approved in writing, substance use, and pandemic/communicable disease (still broadly excluded in 2026).

2. Negative Film & Faulty Stock

Negative Film & Faulty Stock coverage pays for the loss, damage, or destruction of original captured media — camera negative, RAW files, ProRes masters, sound files — and the cost of reshooting or recreating lost material. It is the line that responds when a hard drive falls off a truck, a Codex magazine corrupts, an LTO restore fails, or a SAN array gets hit by ransomware. The Faulty Stock subcomponent responds when defective stock, faulty processing, or a faulty camera produces unusable footage.

3. Props, Sets & Wardrobe

This line covers direct physical loss — fire, theft, vandalism, transit — to props, set construction, set dressing, wardrobe, and similar items the production owns, rents, or controls, including in transit between stages and locations. Keep a current inventory with replacement values: without documentation, you are paid actual cash value at the carrier's discretion, not what you spent.

4. Miscellaneous Equipment (Owned & Rented Gear)

Miscellaneous Equipment insures cameras, lenses, lighting, grip, sound, dollies, jibs, and cranes — usually the largest dollar-value line on the policy. Three sublimits matter: the per-item limit (must absorb your highest-value single piece — a $200K camera body needs a per-item limit that covers it), the per-occurrence limit (the worst-case truck loss), and the territory limit (US/Canada vs worldwide).

The COI Trap That Kills Indies

Every rental house demands a Certificate of Insurance before releasing gear. The COI must show an equipment limit at or above replacement value, name the rental house as Loss Payee, and add them as Additional Insured for liability. Get the COI 48–72 hours before pickup. Without it, the rental agreement's loss & damage clause governs — and you pay the rental house's published replacement cost, not your policy's valuation.

5. Third-Party Property Damage (Location Coverage)

Third-Party Property Damage pays when the production damages property it does not own — a location's hardwood floors, a neighbor's wall, a hotel suite, a leased stage. It is one of the most frequently used coverages on the package and the line that protects your location-fee deposit. The claim requires a signed location agreement plus before-and-after photos; bodily injury at a location is handled by general liability, not this line.

6. Extra Expense

Extra Expense is the financial backbone of any shutdown. It pays the increased cost of continuing production when a covered peril interrupts operations: standby crew, restoration costs, backup locations, make-up days, and replacement equipment rental. It is one of the most forensically reviewed claims on a production — document every additional dollar.

7. Civil Authority & Ingress/Egress

These endorsements respond when access to your location is restricted by an external event even if the location itself is undamaged — the lines that paid during the 2025 LA wildfires and hurricane evacuations in Louisiana and coastal Georgia. Both typically carry a 30- or 90-day maximum duration and a waiting-period deductible of 24–72 hours, and carriers tightened these terms after the 2024–2025 fire and hurricane seasons.

General Liability: The Eighth Essential Line

General Liability covers third-party bodily injury and property damage — the passerby who trips over a cable run, the homeowner who sues over a night shoot, the extra struck by falling set dressing. The small-production floor is $1M per occurrence / $2M aggregate; studios and streamers push umbrella towers to $5M, $10M, $25M, and beyond.

Three endorsements turn a stock GL policy into a production policy: Additional Insured endorsements naming the location, studio, streamer, vendors, and bank; Waiver of Subrogation in their favor; and Primary and Non-Contributory wording. Without all three, your COI will be rejected.

If You Read One Thing About Liability, Read This

Indies routinely buy $1M/$2M, then accept a studio agreement requiring $5M/$10M. When the COI is rejected the day before the shoot, you cannot upgrade limits in 24 hours without short-rate premium and overnight underwriting. Read every distribution, location, and production-services agreement BEFORE you bind. Match the insurance to the contracts, not the other way around.

What Other Coverages Do Productions Need?

Beyond the Producer's Package and general liability, a complete production insurance program adds auto, workers' compensation, E&O, and specialty lines matched to what the production actually does.

Production Auto: Liability, Hired & Non-Owned, Physical Damage

Productions touch three vehicle types: owned, hired (rental trucks, sprinters, picture cars), and non-owned (crew personal vehicles on production business). Hired & Non-Owned Auto (HNOA) is non-negotiable on every production — it responds when a PA rear-ends a sedan on a lunch run, and personal auto policies do not cover business use. Buying physical damage through the production auto policy is usually 30–60% cheaper than rental-counter loss & damage waivers if you run more than one truck. Picture vehicles need agreed-value appraisals and a scheduled Picture Vehicle endorsement; stunt driving needs a separate stunt endorsement.

Workers' Compensation for Cast & Crew

Workers' comp is mandatory, state-specific, and the largest concentration of audit and claim risk on the program. Every W-2 employee — whether paid directly or through a payroll service like Cast & Crew, Entertainment Partners, Wrapbook, or GreenSlate — must be covered in the state where work is performed, from the moment of hire.

• Class codes: Most cast and crew sit on NCCI class code 9610 (motion picture production); stunts, aerial, underwater, and pyro push to higher-rated codes; office staff sit on 8810. Miscoding is common — and shows up on audit.

• Multi-state: Shoot in three states, carry comp in three states. Monopolistic states (ND, OH, WA, WY) require their state fund.

• Water shoots: Work on navigable waters requires federal USL&H coverage; standard state comp does not respond. Crew on vessels needs Maritime Employer's Liability for Jones Act exposure.

• Loan-outs: When talent works through a loan-out corporation, the production's policy needs an Alternate Employer Endorsement so it responds if the loan-out's comp is missing or denies.

The Most Expensive WC Mistake in Indie Film

Classifying crew as 'independent contractors' to save payroll. State workers' comp boards judge by the actual work performed, not the paperwork. When a 'contractor' gets hurt, the state reclassifies, the carrier audits, and the production owes back-premium plus penalties plus the claim. Run cast and crew W-2 through a payroll service — it is cheaper than a single misclassification claim.

Errors & Omissions (E&O): Protecting the Content

E&O is the content-IP liability line: copyright and trademark infringement, defamation, invasion of privacy, right of publicity, plagiarism, and unauthorized use of titles or characters. It responds when the songwriter, the look-alike, or the rights-holder sues. Coverage is claims-made, underwritten from a full Chain of Title package (signed agreements, music licenses, clearances, opinion letters), and required as a delivery item by every major distributor — $1M/$3M standard, $3M/$5M+ for theatrical and major streamers.

Specialty Lines: Weapons, Stunts, Drones, Cyber, Completion Bonds

• Hazardous activity endorsements: Every production policy excludes hazardous activities by default — stunts, pyro, weapons, aerial — until specifically scheduled and endorsed. The post-Rust market is materially tighter on weapons.

• Drone/aerial: Drone work requires a scheduled Drone Liability endorsement, a Part 107-certified operator, Remote ID compliance, and FAA waivers that match the insurance endorsements for crowd, night, or beyond-line-of-sight work.

• Cyber: Standard production insurance excludes cyber. A dedicated cyber policy covers ransomware, dailies lockouts, script leaks, digital-asset restoration, and breach notification. Underwriters expect MFA, encrypted transfer (Aspera/Signiant, not personal Dropbox), and a written incident-response plan.

• Completion bond: Technically a surety, not insurance: it assures financiers the film will be completed and delivered. Fees historically ran 3%–5% of budget; after market restructuring, some indies now see 4.5%–6%, and projects in fire-prone regions during fire season may be functionally non-bondable. Treat bond viability as a financing-stage consideration, not a delivery-stage afterthought.

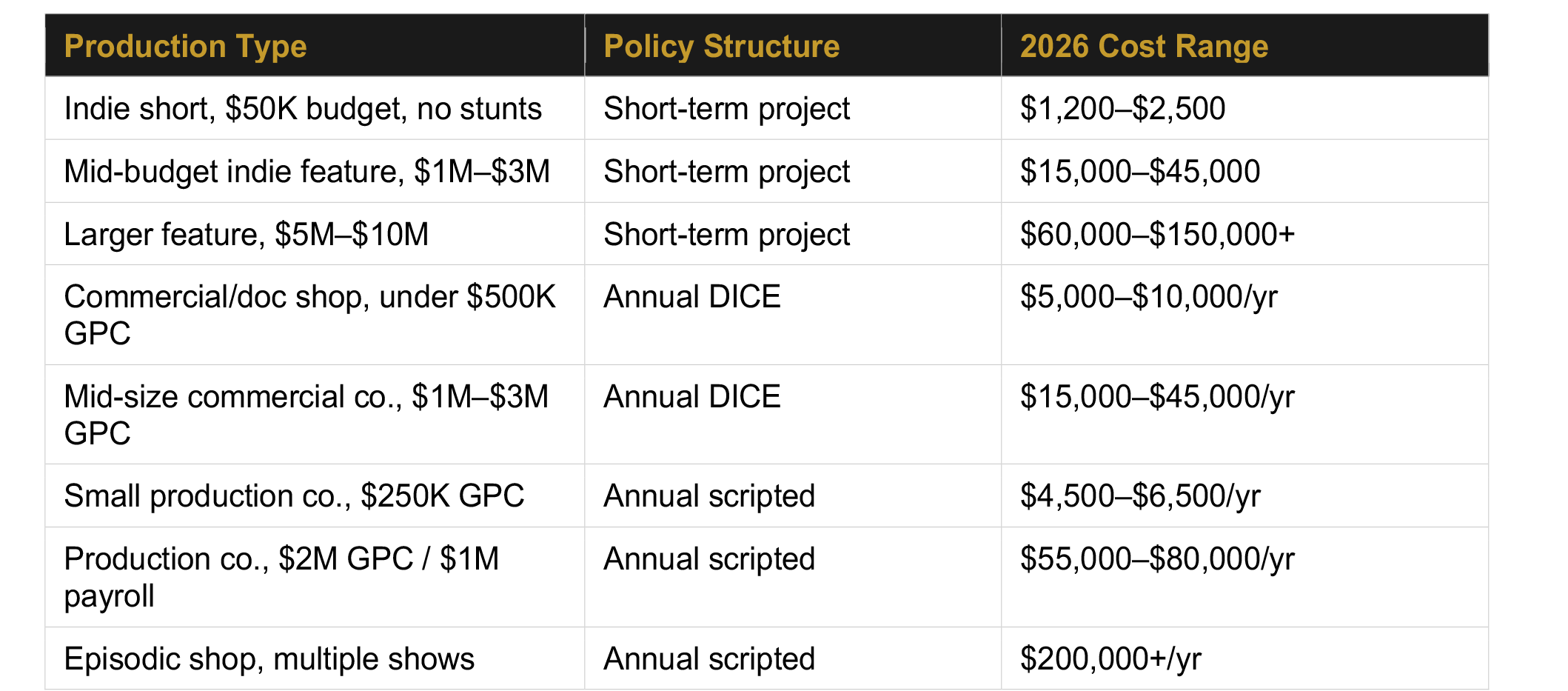

How Much Does Film Production Insurance Cost in 2026?

Film production insurance costs between $1,200 for a small indie short and $200,000+ per year for episodic production companies, driven by gross production costs, payroll, locations, cast, and hazardous activities.

Ranges are directional 2026 market. Every quote is underwritten from the script breakdown, budget, locations, declared cast, and hazardous activities — treat these as planning numbers, not quotes.

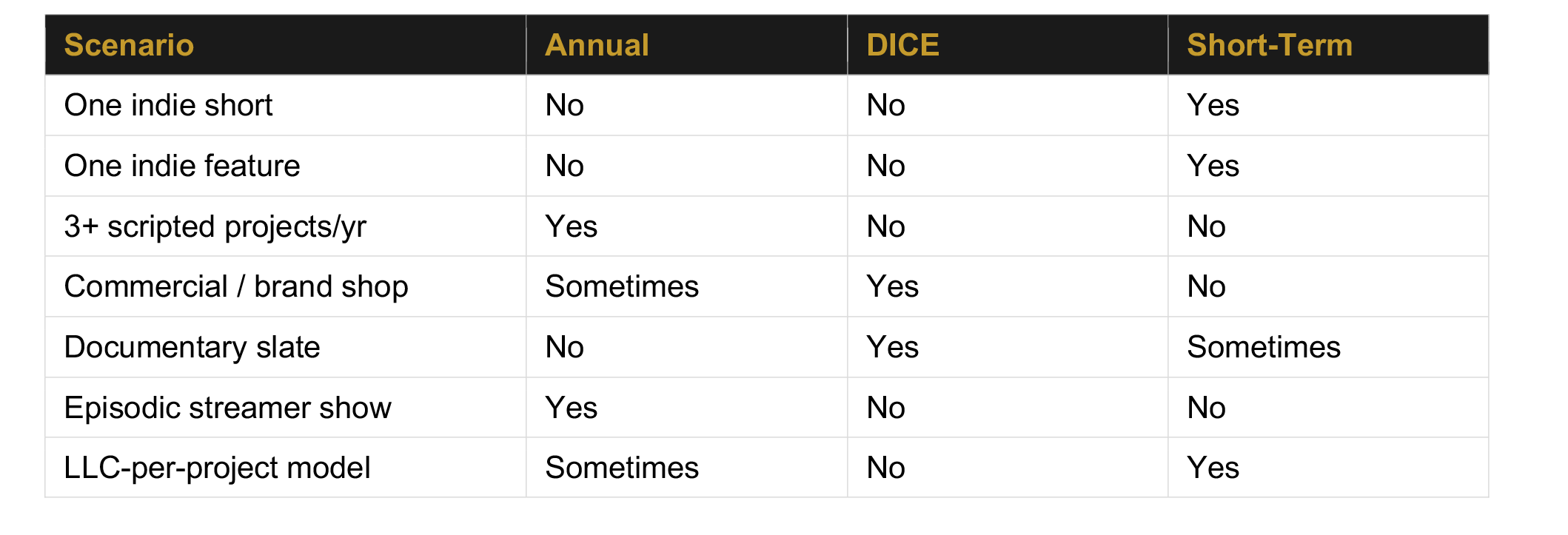

Annual vs DICE vs Short-Term: Which Policy Structure Is Right?

Production companies choose between three structures — annual, DICE, and short-term project policies — and choosing wrong costs money on every production for the life of the company.

Annual Production Policy

Covers everything the company shoots in a policy year, premium calculated against projected annual Gross Production Costs and payroll with a year-end audit against actuals (deposit premium is typically 75–80% of estimate). Best for companies shooting three or more scripted projects per year and episodic shops. Pros: one underwriting cycle, continuity across projects, stacked Additional Insured endorsements, studio preference. Cons: punishing audit-backs if you under-project, limit erosion across projects, and a claim on Project A affects renewal pricing for Project B.

DICE Policy (Documentary, Industrial, Commercial, Educational)

An annual structure built for companies that don't shoot scripted theatrical features — commercial production houses, content agencies, corporate video shops, brand-content arms, and documentary studios. Lower base rates reflect the lower claim frequency of commercial and doc work. Scripted theatrical, episodic above a budget threshold, and high-budget music videos are excluded by default.

Short-Term / Project Policy

Covers a single production from prep through delivery — sometimes a single shoot day — underwritten from the script breakdown with premium final at binding and no audit. Best for first features, one-off indies, and LLC-per-project financing structures. Studios and streamers accept short-term policies for indie and commercial work when the limits, additional insureds, and waiver language match the production services agreement.

Decision Matrix

How Do You Manage Production Risk, Stage by Stage?

The most cost-effective insurance dollar a production spends is the one spent on risk management before the shoot starts — carriers and bond companies underwrite operations, not paper.

Pre-Production: Where Claims Are Prevented

• Script breakdown for risk: Run a parallel risk breakdown alongside the 1st AD breakdown — tag every scene for stunts, weapons, pyro, animals, minors, water, aerial, and private-home shoots. It drives insurance scheduling, location selection, and safety budgeting.

• Location scouts: Every location scout is an insurance scout. Photograph floor-to-ceiling on the first visit, document pre-existing damage, identify the owner and neighbors, and note the closest hospital and trauma center.

• Vendor vetting: Every vendor provides a current COI before the deal memo is signed — rental houses, transport, stunt coordinators, animal handlers, pyro, drone operators, caterers — naming the production as Additional Insured with Waiver of Subrogation and Primary/Non-Contributory wording.

• COI tracker: Log every COI in and out: counterparty, limits, expiration, endorsement language, and a copy of the certificate. COIs that expire mid-shoot are the single largest preventable insurance gap.

• Contract review: Location agreements, vendor agreements, and talent contracts each contain insurance and indemnity clauses that become part of your program. Have counsel or your broker review every one before signing — and push back on blank-check language like 'or such higher amounts as may be required.'

Production: Daily Discipline

• First-of-the-day safety meeting before the first shot, covering stunts, weapons, weather, medic location, and evacuation routes. The 1st AD owns it; document it.

• Post-Rust weapons protocol: licensed armorer present whenever a weapon is on stage, written firearms protocol posted, zero live ammunition on the property, two independent safety checks before every take.

• Drone operations: FAA Part 107 authorization, applicable waivers, Remote ID compliance, and local permits. Traffic control through licensed vendors with their own liability coverage.

• Professional weather monitoring (DTN, WeatherOps, StormGeo) on outdoor shoots — and document every weather hold decision; it matters at the claim.

• Certified set medic for stunts, pyro, and weapons; on larger productions, every shoot day. The medic's incident log is the documentary backbone of any workers' comp claim.

Post-Production: Protect the Asset

• Original media lives in three places: production storage, backup, and off-site or cloud — checksummed at every step. Faulty Stock coverage assumes you can prove the chain.

• Cyber hygiene: MFA on every account, least-privilege vendor access, encrypted transfer, watermarked cuts for distributors and festivals, and a written incident-response plan before the event.

What Do You Do When Something Goes Wrong? Four Claims Playbooks

The first sixty minutes after an on-set incident determine whether the claim resolves cleanly or turns into a six-figure dispute.

Playbook 1 — Auto Claim

First hour: confirm scene safety, call 911 for any suspected injury, always file a police report, photograph everything (vehicles, plates, damage, scene, road conditions), collect all driver and witness information, and notify the broker before giving any recorded statement. First 24 hours: written incident report, broker opens the claim, vehicle held for inspection, parallel WC procedure if the driver is an employee. First 7 days: adjuster inspection, repair estimates, police report retrieval, loss-of-use documentation, and subrogation review.

Playbook 2 — Workers' Compensation Injury

First hour: stabilize the injured person (medic first, 911 beyond minor), photograph the scene before anything moves, identify the supervisor and 1st AD, notify production office and broker. First 24 hours: file the First Report of Injury per state rules (most states within 7 days, several within 24 hours), provide the panel-of-physicians list, open the claim through the payroll service, and begin the return-to-work conversation. First 7 days: collect medical reports and witness statements, offer modified duty when medically supported, review the adjuster's reserve, and verify Alternate Employer Endorsement response for loan-outs. Travel-day injuries are aggressively contested — document the work nexus carefully.

Playbook 3 — Equipment Loss, Damage, or Theft

First hour: confirm the loss, secure the scene and call police for theft, photograph the storage area and any forced entry, pull serial numbers, notify the rental house and broker. First 24 hours: police report on file (every carrier requires it for theft), written replacement quote from the rental house, and do not pay the rental house's L&D invoice until the claim is reviewed. First 7 days: adjuster inspection, salvage discussion, settlement negotiation, and subrogation against any responsible third party.

Playbook 4 — Third-Party / Location Property Damage

First hour: stop further damage, locate the location agreement and pre-shoot walk-through photos, photograph and video the damage, and notify the owner in writing plus the broker. First 24 hours: written incident report, claim opened under Third-Party Property Damage (GL carrier too if there's a bodily-injury element), restoration vendors only with carrier approval, and preserve the damaged material — disposing of it before the adjuster inspects is a common, costly mistake. First 7 days: adjuster on site, pre/post photos compared to establish scope, multiple repair estimates, and settlement coordinated through carrier counsel above the deductible.

Reserves, Subrogation & Settlement — Know These Three

Reserves are the dollars the carrier sets aside for a claim — they become part of your loss runs and affect renewal pricing. Subrogation is the carrier's right to pursue the third party who caused the loss; cooperate fully. Never agree to a settlement number on-scene — admissions of fault bind the carrier. And on WC claims, actively offer modified duty: every week off-duty erodes the outcome and raises your mod.

The 2026 Film Production Risk Landscape: Why Your Premium Just Moved

Six events have rewritten how productions are underwritten, priced, and bonded in 2026. A producer who is not tracking them is paying for risk they no longer have — and uncovered for risk they do.

1. The Rust Fallout and the Firearms Reset

The 2021 Rust shooting and the criminal proceedings that followed through 2024 rewrote the national firearms standard. California began requiring formal armorer training in 2024–2025, with New Mexico and Georgia following. Carriers now require certified armorers, written firearms protocols at every weapons call, rubber versions of every practical firearm, and absolute zero live ammunition on production property — and they are auditing these standards mid-policy.

2. The 2025 Los Angeles Wildfires

The January 2025 fires destroyed neighborhoods in the Palisades, Altadena, and Malibu and paused LA production for weeks. Completion-bond underwriters now price wildfire seasonality in LA County, several carriers non-renewed wildfire-exposed accounts, and Civil Authority / Ingress-Egress terms tightened market-wide. The same dynamic now applies to hurricane exposure in Georgia, Florida, Louisiana, and the Gulf Coast — have weather-cancellation conversations at the financing stage, not the COI stage.

3. Completion Bond Restructuring

Film Finances — historically the largest completion-bond provider — has been working through restructuring. The result: fewer bond providers, tighter underwriting on independent productions, bond fees up from the historical 3%–5% to 4.5%–6% on some indies, and some fire-season projects in fire-prone areas becoming functionally non-bondable.

4. AI and Deepfake Clauses in E&O

Most E&O carriers now ask AI-specific underwriting questions; several have applied absolute AI exclusions to certain forms. SAG-AFTRA's digital-replica protections have raised the contractual standard, and underwriters expect documented consent, scope, and compensation for any AI-generated likeness. If your production uses generative AI in any meaningful way — script, imagery, voice cloning, de-aging — disclose it on the application and read the AI endorsements before binding.

5. The Post-Strike Market Reset

The 2023 WGA and SAG-AFTRA strikes (148 and 118 days) cost the industry an estimated $5 billion+. The downstream effects through 2026: more aggressive underwriting on returning slates, multi-year audit true-ups on annual policies that ran through the strikes, and renewed scrutiny of strike-risk language. Strike and contract-driven shutdowns remain broadly excluded from standard production policies — verify your form rather than assuming coverage.

6. Climate-Driven Weather Exposure and Drone Incidents

Heat waves, atmospheric-river rain, and high-fire-weather day counts have made outdoor shoots materially more weather-exposed than in 2019, and weather-day coverage has become more expensive with tighter triggers. Drone incidents continue to rise with drone use; underwriters now want Part 107 certification, written drone protocols, FAA waiver alignment, and operator history before binding higher limits.

Frequently Asked Questions About Film Production Insurance

What is film production insurance?

Film production insurance is a bundled program — a Producer's Package plus general liability and specialty coverages — that protects a film, TV, or commercial production against cast unavailability, equipment loss, location damage, shutdown costs, injuries, and lawsuits. Studios, rental houses, locations, financiers, and bond companies all require proof of it before a production can shoot.

How much does film production insurance cost in 2026?

A short-term policy for a small indie short runs $1,200–$2,500. A mid-budget indie feature ($1M–$3M) runs $15,000–$45,000. A larger feature ($5M–$10M) runs $60,000–$150,000+. Annual policies start around $4,500–$6,500 for small production companies and scale to $200,000+ for episodic shops. Entry-level DICE starts around $5,000 per year.

What is a Producer's Package?

A Producer's Package is the core bundled production policy. It contains seven first-party coverages: Cast Insurance, Negative Film & Faulty Stock, Props/Sets/Wardrobe, Miscellaneous Equipment, Third-Party Property Damage, Extra Expense, and Civil Authority/Ingress-Egress. General Liability is sold alongside it; auto, workers' comp, E&O, drone, and cyber are added on top.

What is a DICE policy and when do I need one?

DICE — Documentary, Industrial, Commercial, Educational — is an annual production policy for companies that don't shoot scripted theatrical features: commercial production houses, branded-content agencies, corporate video shops, and documentary studios. It's the right structure if you produce three or more projects per year. Entry-level DICE starts around $5,000 annually.

Do I need insurance for a small short film?

Yes. Rental houses won't release gear without a Certificate of Insurance, locations won't sign without liability proof, and SAG-AFTRA contracts require workers' compensation. Even a $5,000 student short needs short-term general liability and workers' comp at minimum. Small-short policies start around $1,200.

How did the Rust shooting change film insurance?

Carriers and studios now require a certified armorer on set whenever weapons are present, zero live ammunition on production property, written firearms safety protocols, and two independent safety checks before each take. California formalized armorer training requirements in 2024–2025, and some carriers have stopped writing weapons risk for productions without IATSE-trained armorers.

Did the 2025 LA wildfires affect production insurance pricing?

Yes. Civil Authority and weather-cancellation terms tightened market-wide, several carriers non-renewed wildfire-exposed accounts, and completion-bond underwriting in LA County now prices wildfire seasonality. The same dynamic applies to hurricane exposure for productions in Georgia, Florida, Louisiana, and the Gulf Coast.

Does my production policy cover drone operations?

Not by default. Drone work requires a separately scheduled Drone Liability endorsement or standalone drone policy, with a Part 107-certified operator and Remote ID compliance. Operations over crowds, beyond visual line of sight, or at night require matching FAA waivers and insurance endorsements.

What does Errors & Omissions (E&O) insurance cover for film?

E&O covers content-IP liability: copyright and trademark infringement, defamation, invasion of privacy, right of publicity, plagiarism, and unauthorized use of titles or characters. Standard delivery requirement is $1M/$3M, with theatrical and major streamer titles at $3M/$5M or higher. Every major distributor requires it as a delivery item.

Are AI-generated likenesses covered by E&O insurance?

Increasingly not by default. Several major carriers added AI-specific exclusions and underwriting questions to E&O forms in 2025–2026. Productions using generative AI for finished imagery, voice cloning, or digital replicas must disclose it on the application, document consent and compensation per SAG-AFTRA digital-replica protections, and confirm coverage in writing before binding.

Do I need cyber insurance for a film production?

Yes. Productions run on shared cloud storage, distributed editorial, and remote VFX — all cyber attack surface — and standard production insurance excludes cyber events. A dedicated cyber policy responds to ransomware, dailies lockouts, script leaks, and breach notification. Underwriters expect MFA, encrypted transfer, and a written incident-response plan.

What is a completion bond and do I need one?

A completion bond (completion guarantee) assures financiers the film will be finished and delivered on agreed terms; if the production fails, the bond company can step in. Fees typically run 3%–5% of budget — now 4.5%–6% on some indies after market restructuring. Nearly every bank and major equity financier requires one on independently financed productions.

How do I handle a workers' comp injury on set?

Stabilize first — set medic responds, 911 for anything beyond minor. Photograph the scene, identify the supervisor and 1st AD for the incident report, and notify the production office and broker. File the First Report of Injury per state rules (most states within 7 days, several within 24 hours), provide the panel-of-physicians list where applicable, and offer modified duty as soon as medically supported.

My location agreement requires $5M in liability but my policy is $1M/$2M. What now?

Increase the underlying limit, add an umbrella, or both — before signing. Last-minute limit increases require short-rate premium and overnight underwriting, both avoidable. Match insurance limits to your largest contractual requirement, not the smallest.

Working With Akker: Get a Film Production Insurance Quote

Akker, LLC is a national specialty insurance agency focused on film, television, and production risk — licensed in 42 states, placing coverage across indie features, episodic streamers, commercial production houses, and documentary slates with admitted and surplus markets that actually understand how productions operate.

What you get: pre-production risk reviews that integrate with your script breakdown, COI workflow that doesn't fall apart the Friday before principal photography, and claims advocacy that starts at the first call from set — not after the adjuster has set the reserve.

• Short-term productions (under $1M): akkerins.com/short-term-film-insurance

• Full productions (over $1M): akkerins.com/film-quote-app

• Free film risk tools (23 tools): akkerins.com/filmriskmanagement

Call 912-247-3075 or email info@akkerins.com — quote, coverage review, or claim help, one call.