The Equipment Rental House Risk Management Guide: How to Protect Your Inventory, Your Business, and Every Renter You Say Yes To

A complete risk management framework for film and entertainment equipment rental houses — from your rental contract to your insurance policy to the moment your gear walks out the door.

By Stan Shkilnyi | Akker LLC — Film & Entertainment Insurance Specialists | 20+ Years Entertainment Industry | akkerins.com/filmriskmanagement

QUICK ANSWER | Equipment Rental House Risk Management

Film and entertainment equipment rental houses face five core risk categories: inventory damage and theft, transit losses, third-party liability at the rental facility, employee dishonesty, and renter non-payment after a claim. A complete risk management program combines the right insurance coverages (inland marine, GL, commercial property, workers' comp), a bulletproof rental contract, a renter vetting process, a COI verification procedure, and a documented inventory system. Together these layers protect your inventory whether it is on your shelf, in a renter's hands, or in a transit vehicle.

If you run a film or entertainment equipment rental house, you already know the basic math: expensive gear, constant turnover, clients you know well and clients you are meeting for the first time, and a business model where every rental is a small act of trust.

A single camera package from your inventory — body, lenses, follow focus, matte box, monitor — can represent $50,000 to $150,000 in replacement value. A full lighting package for a major commercial shoot can top $200,000. When that gear leaves your facility, it is going to sets you have never seen, in vehicles you do not control, operated by crew members you have never met.

Risk management for equipment rental houses is not complicated — but it requires being deliberate. Most rental houses that suffer major losses did not fail because they lacked insurance. They failed because their insurance was the only layer of protection they had. The rental contract was weak. The renter's COI was never verified. The inventory records were out of date. The security system footage was not stored long enough. One or two gaps in the system let a $80,000 loss become unrecoverable.

This guide walks you through every layer of protection a rental house needs — from your rental agreement to your warehouse security to your insurance program — so that when something goes wrong, you have something to stand on.

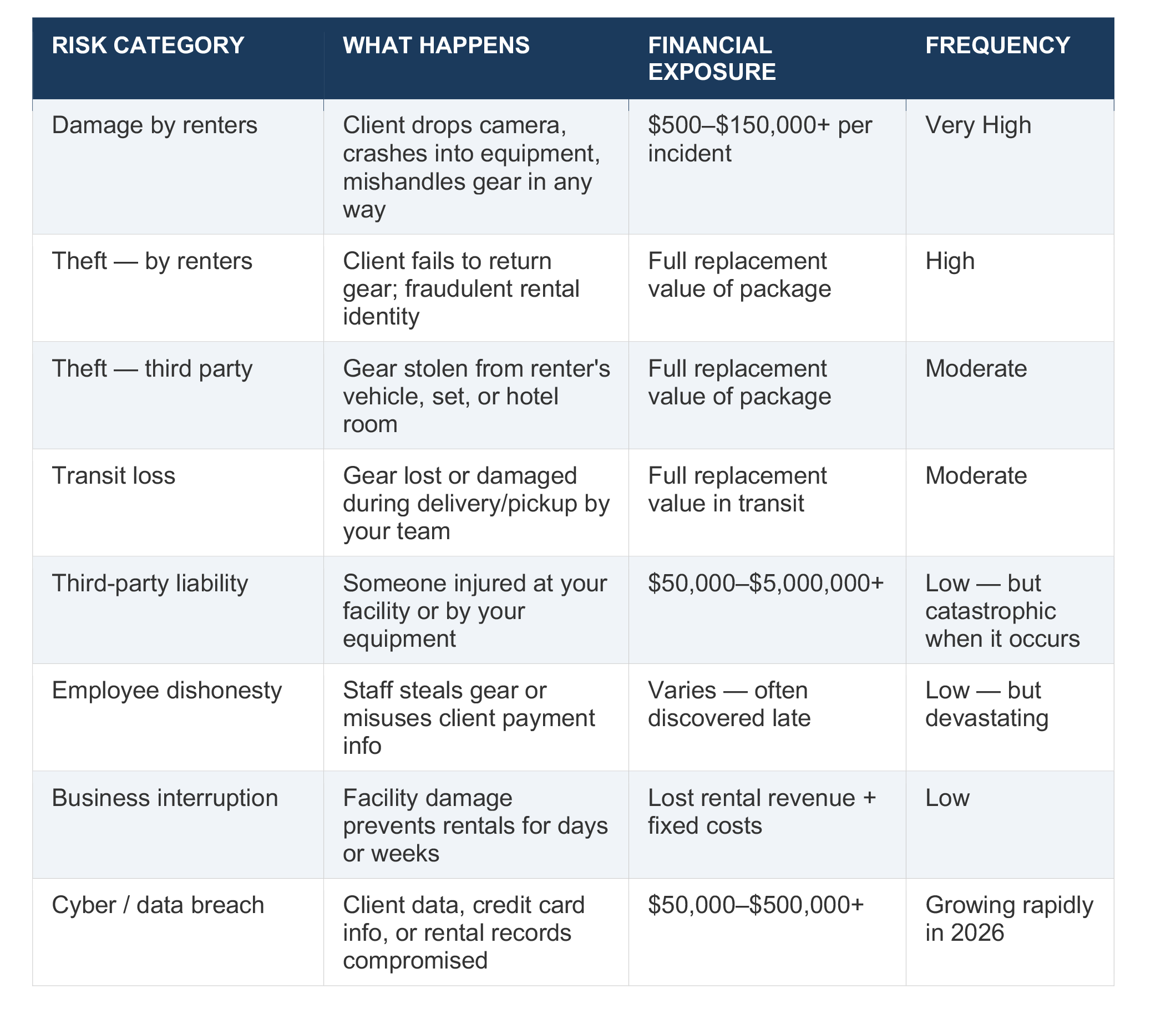

What Are the Core Risks a Film Equipment Rental House Faces?

Before building a risk management program, you need to know exactly what you are protecting against. The risks for a rental house are different from those of a production company or an individual filmmaker — because you are constantly transferring custody of your most valuable assets to third parties.

Risk Management Tool 1 — Your Rental Agreement Is Your First Line of Defense

The rental agreement is not a formality. It is a legally binding contract that determines who is financially responsible when something goes wrong. A weak rental agreement means your insurance policy becomes the primary — and often only — line of recovery for losses that a renter should be covering.

What Every Rental Agreement Must Include

• Replacement value clause: The renter is responsible for the full replacement cost of any equipment damaged, lost, or stolen during the rental period — not the depreciated value and not the rental fee. State this explicitly. Many rental disputes fail because the contract only referenced 'damage costs' and not 'replacement value.'

• Rental period definition: Define exactly when the renter's custody and liability begins (pickup or delivery) and when it ends (return to your facility and inspected). The gap between 'dropped off at the front desk' and 'checked back into inventory' is where disputes live.

• Approved use restrictions: State where and how the equipment may be used. Underwater housing on a camera that was not rented for underwater use. An aerial gimbal on a drone when the rental did not include drone use. Restrictions define the scope of authorized risk.

• Insurance requirements: Require the renter to carry their own inland marine coverage naming your business as Loss Payee and Additional Insured with minimum limits appropriate to the rental value. Define what an acceptable certificate of insurance looks like.

• Security deposit terms: Define exactly what the deposit covers, under what circumstances it is forfeited, and your right to pursue additional recovery beyond the deposit if damages exceed it.

• Jurisdiction and governing law: Specify which state's law governs the contract. Critical for out-of-state renters.

• Force majeure and exceptions: Define what constitutes an excused failure to return — and what does not. Weather delays are not an excuse to return equipment two weeks late.

Stan's direct observation:

The most common contract failure I see in rental house claims is vague damage language. 'Renter is responsible for damage' is not enforceable at the level you need. 'Renter is responsible for the full manufacturer replacement cost of any item damaged, lost, or stolen during the rental period, regardless of cause' is. The word 'regardless of cause' is the difference between a recoverable claim and a payment dispute that takes six months to resolve.

Risk Management Tool 2 — How to Vet Every Renter Before the Gear Leaves

Not every renter is equal risk. A production company you have worked with for five years is a different conversation than someone who called this morning wanting to take a $60,000 camera package out tonight. Your vetting process should be systematic and applied consistently — because inconsistency creates legal exposure when disputes arise.

The Standard Renter Vetting Checklist

1. Verify identity: Government-issued photo ID on file. For companies, require the name and ID of the individual taking custody.

2. Verify the company exists: Google the production company. Check their website, social media, and recent credits. A real production company has a footprint. A fraudulent one usually does not.

3. Require a COI before any gear leaves: The renter's certificate of insurance must name your business as both Loss Payee and Additional Insured, show limits appropriate to the rental value, and list the correct policy period covering the rental dates. Do not accept COIs dated after the rental start date.

4. Call the insurance carrier to verify: A COI can be fabricated. Call the phone number on the certificate — not a number the renter provides — and verify that the policy is active and in force. This takes three minutes and has caught fraudulent rentals.

5. Collect a security deposit by credit card: Never cash. A credit card deposit gives you a chargeback option if the renter disputes the claim. Keep the card on file for the duration of the rental.

6. Document equipment condition before release: Photograph or video every piece of gear at checkout. Time-stamp the documentation. This eliminates disputes about whether damage existed before the rental.

7. Get a signed acknowledgment of replacement values: The renter should sign a document listing every item and its replacement value before taking custody. No surprises after the fact.

Risk Management Tool 3 — Inventory Management as a Risk Control

Your inventory records are the foundation of every insurance claim you will ever file. If you cannot prove what you owned, what condition it was in, and what it was worth — your carrier cannot pay you what you are owed. Rental houses with excellent inventory documentation recover faster and more completely than those without it.

What a Claim-Ready Inventory System Looks Like

• Serial number database: Every item in your inventory catalogued by manufacturer, model, serial number, and current replacement value. Updated when new gear is purchased and when items are retired or sold.

• Condition grading at check-in: Every returned item inspected and graded (Excellent / Good / Fair / Damaged) at return. Damage noted in writing and photographed before any repair is initiated. This is your evidence trail for renter liability claims.

• Replacement value updates annually: Camera technology depreciates fast but some lenses appreciate. Review replacement values at least annually — ideally before each policy renewal — to ensure your coverage limits reflect your actual inventory value.

• Off-premises tracking: Know where every item is at all times. Which items are on rent, who has them, what the return date is, and what their last-known condition was. A rental management software system (Rentman, Current RMS, Point of Rental) handles this automatically.

• Proof of ownership documentation: Purchase receipts, invoices, or appraisals for every high-value item. Stored in the cloud, not just on a local hard drive that can be lost in the same incident as the equipment.

Risk Management Tool 4 — Building the Right Insurance Program for a Rental House

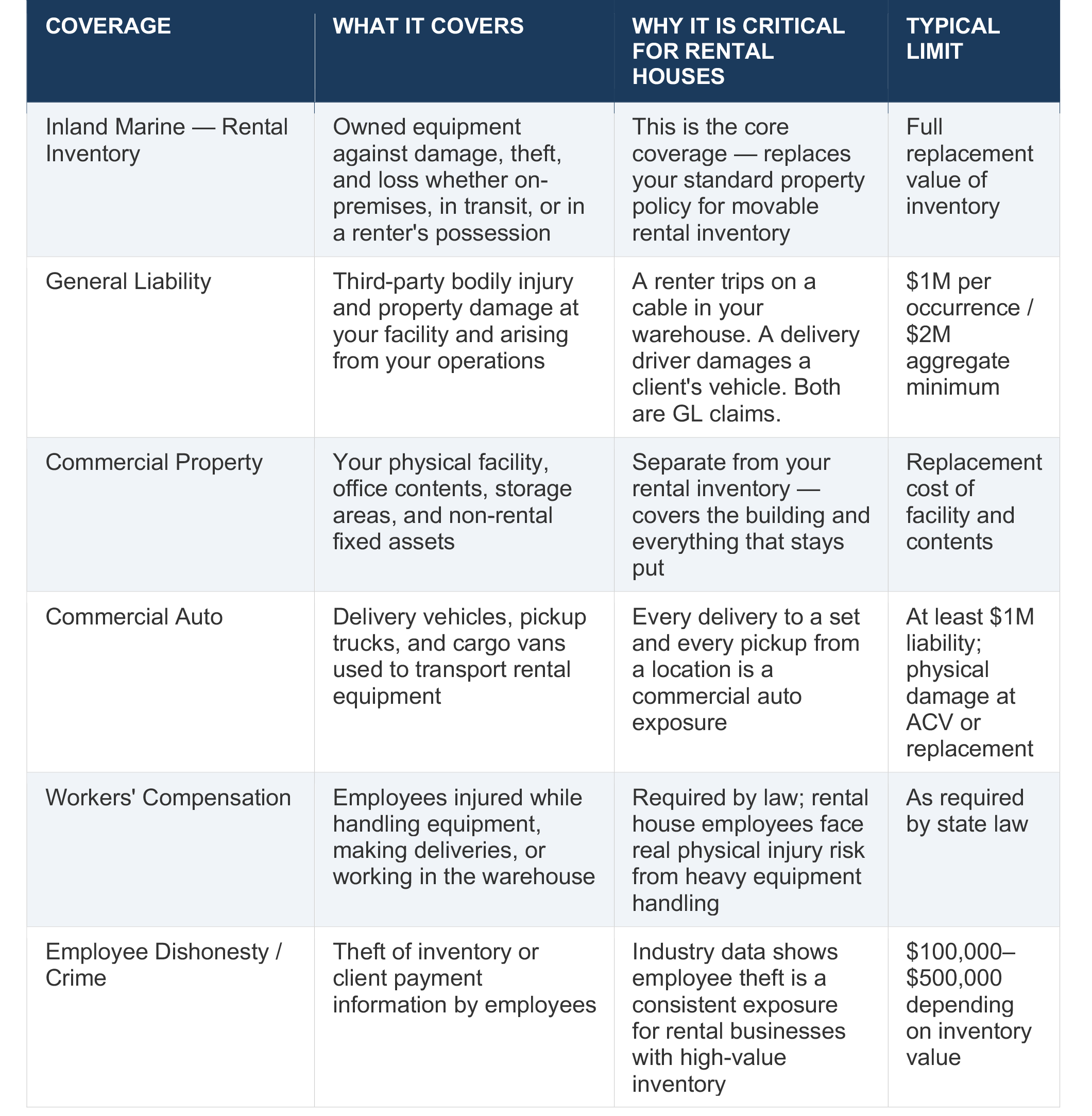

This is where most rental houses either overpay by buying the wrong products from a generalist broker, or under-insure by not understanding what a standard property policy does and does not cover. The critical fact that every rental house owner needs to understand:

⚠️ Standard commercial property insurance does not cover your rental inventory.

Standard commercial property policies are written for equipment that stays at your location. The moment your gear leaves your facility in a renter's hands — or in your delivery vehicle — it exits the coverage of a standard property policy. A rental house that carries only standard commercial property insurance has no coverage for the largest exposure in its business: the inventory that is constantly off-premises.

The 6 Coverages Every Rental House Needs

Optional Coverages Worth Serious Consideration

• Business Interruption Insurance: Covers lost rental revenue and ongoing fixed expenses if a covered loss — fire, flood, break-in — forces you to suspend operations. Most rental houses are completely exposed here.

• Cyber Liability: Covers data breaches involving client credit card information, rental records, and personal identification documents. In 2026, rental businesses that store digital payment and client data are active targets.

• Umbrella / Excess Liability: Provides additional liability limits above your GL, auto, and employers' liability policies. Critical if you rent to large productions with high contractual liability requirements.

• Equipment Breakdown: Covers repair or replacement of equipment that breaks down due to mechanical or electrical failure — distinct from accidental damage. Useful for high-value electronics that experience internal failure without an external cause.

Risk Management Tool 5 — COI Verification — The Step Most Rental Houses Skip

Requiring a certificate of insurance from renters is standard practice. Verifying that the certificate is real, current, and actually covers what it needs to cover is not. This one gap is responsible for more unrecovered rental losses than almost any other single failure.

The 5-Step COI Verification Process

1. Check the policy dates: The policy period on the COI must cover the rental period. A COI that expires during the rental is not acceptable.

2. Verify your business is named correctly: Your business name as Loss Payee and Additional Insured must match exactly. 'Akker LLC' and 'Akker, LLC' are legally different. Insist on the correct legal name.

3. Check the coverage limits: Minimum limits depend on the rental value. For packages over $25,000, require minimum $250,000 in equipment coverage. For packages over $100,000, require $500,000 minimum. Match the limit to the exposure.

4. Call the carrier to verify: Call the number listed on the certificate — not a number provided by the renter. Ask the carrier to confirm the policy is active and in force. Takes three minutes. Has caught fabricated COIs.

5. Keep every COI on file: Store COIs electronically, linked to the rental record. If a claim arises six months after the rental, you need the documentation to be retrievable.

Critical distinction — Loss Payee vs. Additional Insured:

Loss Payee: Your business receives insurance proceeds directly when the renter's policy pays a claim for your equipment. This protects your financial recovery.

Additional Insured: Your business is protected from third-party liability claims arising from the renter's use of your equipment. This protects you from lawsuits.

You need both on every COI. Loss Payee alone does not protect you from liability claims. Additional Insured alone does not guarantee equipment loss recovery.

Risk Management Tool 6 — Physical Security at Your Facility

Your insurance premium is directly influenced by your physical security setup. Carriers writing inland marine coverage for rental houses review your security controls during underwriting — and better controls mean better rates and broader coverage terms. Beyond the insurance benefit, physical security reduces the frequency and severity of losses that damage your claims history and your experience rating.

Minimum Security Standards for a Film Equipment Rental House

• Alarm system monitored 24/7: Central station monitoring with police response. Not just a local alarm. A camera body left unattended in an alarmed warehouse needs a monitored response to be meaningful.

• CCTV coverage of all access points: Including the loading dock, storage rooms, check-out counter, and parking area. Footage retained for minimum 90 days — longer is better, because insurance claims often take weeks to investigate.

• Access control for storage areas: Key card or pin code access to high-value inventory areas. Limit access to employees who need it. Every access should be logged.

• Separate secured storage for highest-value items: Camera packages and premium lenses should be stored in a locked cage or vault within the warehouse — not accessible from the general storage area.

• Delivery vehicle security: Any vehicle used to transport rental equipment needs anti-theft measures. GPS tracking. Cargo area locks. A policy of never leaving equipment unattended in an unlocked vehicle even for five minutes.

• After-hours protocols: Define who has access after hours, what the lockup procedure is, and how after-hours rentals and returns are handled without creating security gaps.

Risk Management Tool 7 — When Something Goes Wrong — Claims Procedure

How you respond in the first 24 hours after a loss determines whether your claim is recoverable — and how much of it you recover. Rental houses that have a written claims procedure before an incident occurs consistently achieve better claim outcomes than those that are figuring it out as they go.

The First 24-Hour Claims Response Protocol

1. Document everything immediately: Photograph the damage. Screenshot communications with the renter. Pull your checkout documentation, COI, and rental agreement before anything else is touched.

2. Notify your carrier within 24 hours: Do not wait until you have the full picture. Report the loss immediately. Late-reported claims face more scrutiny and are more likely to face coverage disputes.

3. Notify the renter in writing: Email or text immediately stating that a loss has occurred and that the renter is responsible under the terms of the rental agreement. This starts the paper trail for recovery.

4. File a police report if theft is involved: Your carrier will require a police report number for any theft claim. File it the same day. Do not wait for the renter to do it.

5. Preserve evidence: Do not repair damaged equipment before your carrier's adjuster has inspected it. Do not erase CCTV footage. Do not discard damaged items.

6. Submit your inventory documentation: Provide the adjuster with serial numbers, purchase receipts, and your most recent valuation for every item in the claim.

7. Pursue renter recovery simultaneously: Your carrier may exercise subrogation rights to recover from the renter or their insurer. Provide all renter documentation — contract, COI, security deposit records — to support that process.

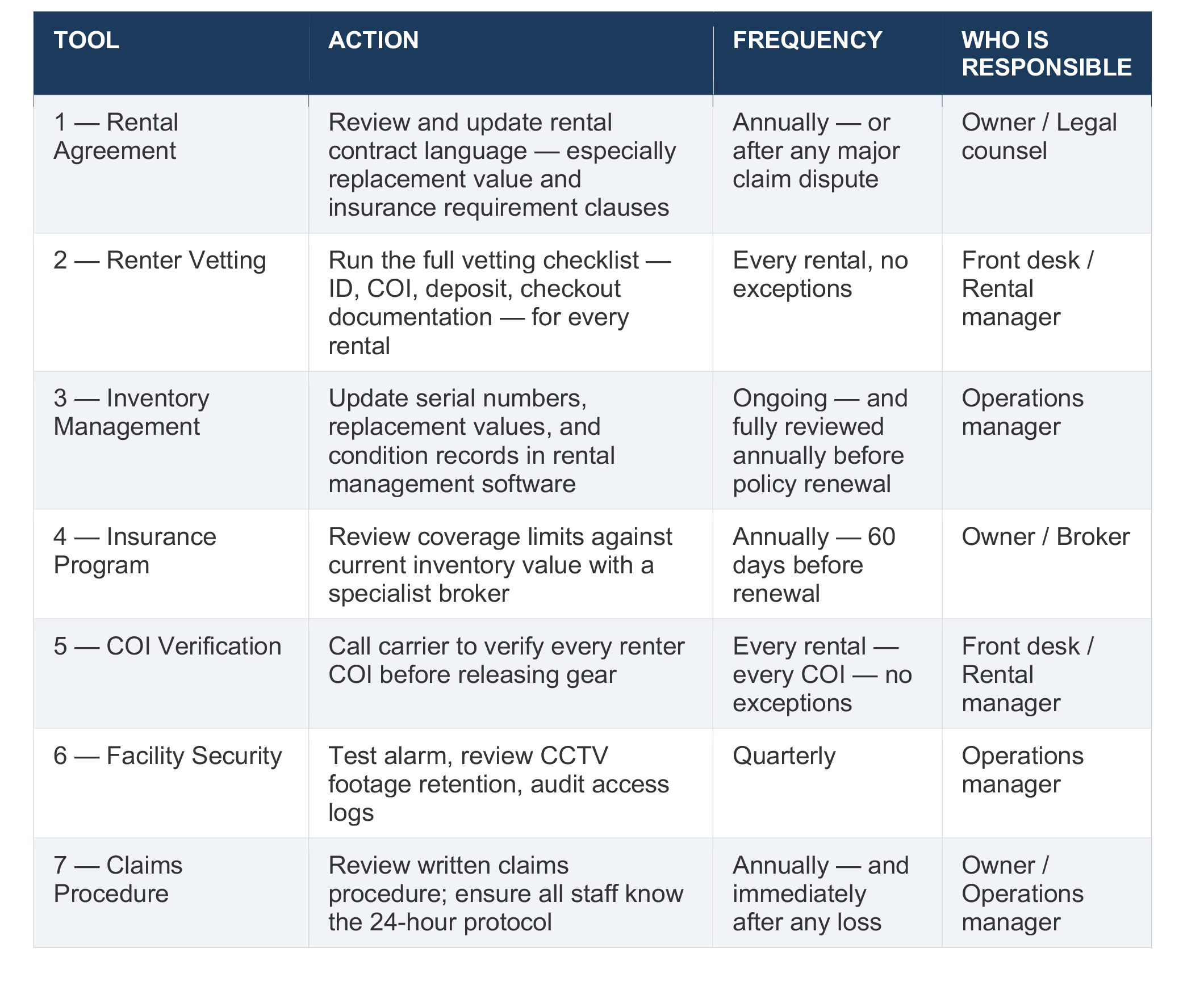

The Complete Risk Management Checklist — At a Glance

Is Your Rental House Insurance Program Built for How You Actually Operate?

Akker LLC works with film and entertainment equipment rental houses to build insurance programs that match how rental operations actually work — not a standard commercial property policy that leaves your inventory unprotected the moment it leaves your facility. We review your rental contract, your COI requirements, your inventory documentation, and your security setup — then place coverage with specialty entertainment carriers who understand this business.

Film Risk Portal: akkerins.com/filmriskmanagement

Film Quote App: https://www.akkerins.com/filminsurance

Contact Stan:stan@akkerins.com | 912-247-3075

Founder, Akker LLC | SCAD Film Producing Graduate | Former Film Producer | IMDB: imdb.com/name/nm3390315 | 20+ Years Entertainment Industry | 15 Years Film & Entertainment Insurance Specialist