Hollywood Just Split in Two Over AI. Neither Side Has the Right Insurance.

James Cameron put a 'NO GENERATIVE AI' title card on Avatar. The co-writer of Pulp Fiction just got three films greenlit overnight by adding the word AI to his pitch. Here is what both sides are missing — and why it matters for every film production in 2026.

Two things happened in Hollywood in February 2026 that nobody has connected. Not the trade press. Not the entertainment lawyers. Certainly not the insurance industry.

First: James Cameron opened Avatar: Fire and Ash with a title card that read 'no generative AI was used in the making of this movie.' A $250 million production. The most technically sophisticated filmmaker alive. A deliberate, public declaration that human artistry was behind every frame.

Second: Roger Avary — Oscar-winning co-writer of Pulp Fiction — went on The Joe Rogan Experience and announced that he had been unable to get a single film made through traditional channels for years. Then he added the word AI to his pitch, launched a company called General Cinema Dynamics, and three features went into active production almost overnight.

Same industry. Same week. Completely opposite bets on where cinema is going.

I have been insuring film productions for two decades. I have a background in film. I have been watching this debate unfold from a seat that most commentators do not occupy — the one where someone has to figure out what happens when something goes wrong on set, in post, or in distribution.

Here is what I can tell you: both sides of this debate have massive blind spots. And the one nobody is talking about is the insurance gap that sits at the center of everything.

The Cameron Side — What It Gets Right and What It Misses

James Cameron's position is principled and, from a filmmaking craft standpoint, defensible. His statement to ComicBook.com was precise: 'I'm not negative about generative AI. I just wanted to point out we don't use it on the Avatar films. We honor and celebrate actors. We don't replace actors.'

That distinction matters. The Avatar films use performance capture — a technology that is 100 percent dependent on real human actors giving real performances that are then translated into digital characters. When people see the Na'vi move, they are watching Zoe Saldana and Sam Worthington. The technology serves the performance. The performance is still human.

This is meaningfully different from generative AI, which synthesizes performances, faces, voices, and bodies from training data. Cameron understands the difference and drew a clear line. And from an insurance standpoint, his position is the comfortable one — because the entire infrastructure of film production insurance was built around exactly this model.

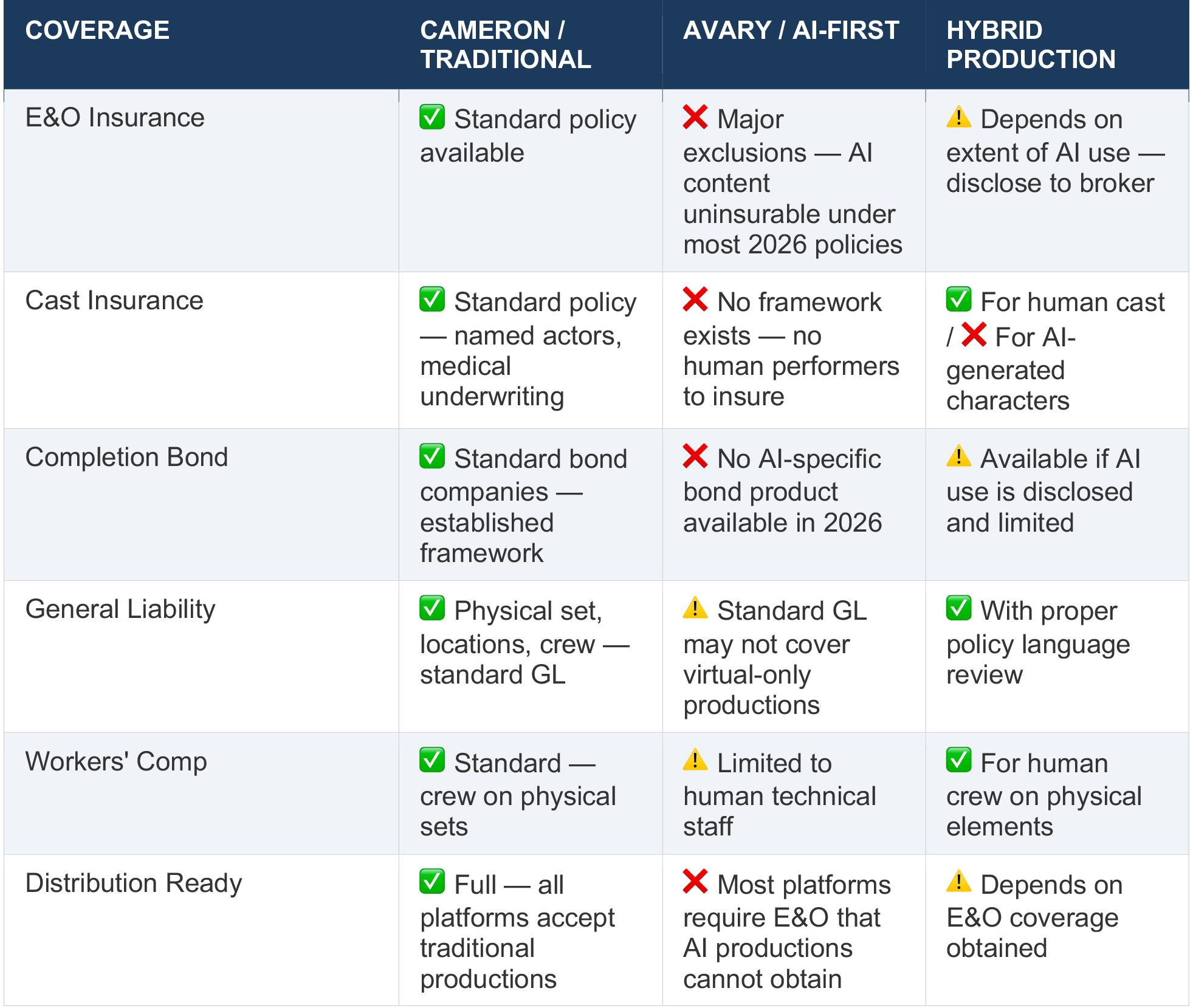

The Cameron Model — Fully Insurable (2026):

✅ Cast insurance: Named human actors. Injury, illness, death coverage — fully underwritten.

✅ Completion bond: Financier protected. Bond company reviews script, budget, schedule — standard framework applies.

✅ E&O insurance: Standard errors & omissions coverage for IP, defamation, clearance issues.

✅ General liability: Physical production locations, crew, equipment — all covered under standard production GL.

✅ Workers' comp: Crew on physical sets. Standard state-by-state WC policies apply.

Cameron's production is fully insurable because it follows the model carriers built their actuarial tables around. Every risk is familiar. Every coverage has a precedent. The premium is high because the budget is high — but the coverage is complete.

What Cameron misses — and where his position has a blind spot — is that the line he is drawing may not hold. Not because he is wrong about craft, but because the economics of the industry are shifting in ways that will eventually force even principled filmmakers to engage with tools they currently reject. The studios funding $250 million films are the same studios quietly running AI pilots in their post-production and VFX pipelines. The gap between Cameron's title card and the actual practice of Hollywood is already narrower than the title card implies.

The Avary Side — What It Gets Right and What It Misses

Roger Avary's announcement was one of the most honest things a filmmaker has said publicly in years. On The Joe Rogan Experience, Episode 2452, he stripped away all of the usual creative justification and said the quiet part loud:

"I go out there and try to get stuff made, and it's almost impossible. And then I built a technology company over the last year, basically making AI movies, and all of a sudden, boom! Like that, money gets thrown at it. Just by attaching the word AI and the fact that it's a technology-based company, all of a sudden, investors came in, and we're in production on three films now. It was so easy for me to get that going and so difficult for me to get a traditional movie going through the traditional route. Just put AI in front of it and all of a sudden you're in production on three features."

— Roger Avary, The Joe Rogan Experience, Episode 2452, February 2026

This is a significant moment. An Oscar winner — someone with legitimate Hollywood credentials and decades of industry relationships — was unable to get projects financed through conventional channels. Then he reframed the same work as AI-driven technology and investors came immediately.

Avary is right that AI is democratizing something real about film financing. The calculation investors are making is rational: if AI can genuinely reduce production costs by 50-70 percent while maintaining acceptable quality, the risk-adjusted return on a $2 million AI film is better than the risk-adjusted return on a $10 million conventional film. That math is not going away.

He is also right that the tools are impressive. Generative AI video platforms like Runway, Sora, Seedance, and Kling have improved at a pace that nobody predicted. The Tom Cruise versus Brad Pitt clip created by Irish filmmaker Ruairi Robinson using Seedance 2.0 was realistic enough that studios sent cease-and-desist letters — not because it was obviously fake, but because it was convincingly real.

The Avary Model — Insurance Status (2026):

❌ Cast insurance: No standard cast insurance product covers AI-generated performers. There is no named insured. There is no medical exam to underwrite. The framework does not exist.

❌ Completion bond: Bond companies underwrite based on human directors, verified budgets, and deliverable scripts. AI productions have none of these in conventional form. No major bond company has published AI-specific terms as of 2026.

❌ E&O insurance: Standard E&O policies exclude AI-generated content from IP coverage in most 2026 endorsements. A film generated using training data from unlicensed sources faces uninsurable copyright exposure.

❌ General liability: Standard GL policies are written for physical production locations. A production that exists entirely in generative pipelines has no insurable 'set' in the traditional sense.

⚠️ Workers' comp: Potentially the one coverage that partially applies — human programmers, supervisors, and post-production staff still need WC. But the scope is vastly different from a traditional production.

What Avary's model misses — and this is the existential risk for AI-driven production companies — is that investor enthusiasm and insurance viability are not the same thing. Investors are betting on upside. Insurance carriers are underwriting downside. Right now, the downside of an AI production is largely uninsured.

The Four Insurance Gaps That AI Productions Face Right Now

Gap 1 — Errors & Omissions: The Distribution Killer

E&O insurance is not optional. Netflix, Amazon, Apple, Disney+, and every major distributor and sales agent require a minimum of $1 million per claim and $3 million aggregate in E&O coverage as a condition of signing any distribution deal. Without it, your film cannot be distributed on any major platform. Period.

Standard E&O policies cover claims arising from copyright infringement, defamation, invasion of privacy, and unauthorized use of music, name, or likeness. The underwriting process requires a chain-of-title review — documentation showing that every element of the film was either created originally, licensed properly, or is in the public domain.

An AI-generated film has no clean chain of title. Generative AI models are trained on datasets that frequently include copyrighted works — images, audio, performances, dialogue — that were not licensed for commercial use. The Motion Picture Association demonstrated exactly how quickly this becomes a legal crisis: when Seedance 2.0 generated a realistic clip of Tom Cruise and Brad Pitt, the MPA filed an immediate copyright infringement action against ByteDance, calling it 'unauthorized use of U.S. copyrighted works on a massive scale.'

An E&O underwriter reviewing a film whose visual style, character movements, or dialogue patterns may be derivative of unlicensed training data has no established framework for issuing a clean policy. Most 2026 E&O policies contain explicit AI exclusions or require representations that the production contains no AI-generated content that cannot be cleared.

Gap 2 — Cast Insurance: No Human, No Coverage

Cast insurance is purchased for specific named individuals whose absence would materially damage the production. The underwriter reviews that individual's medical history, issues a policy, and — if that person is unable to perform due to injury, illness, or death — pays for the production costs incurred as a result.

What happens when the 'cast' is a generative AI model? There is no named individual. There is no medical underwriting. There is no person who can become ill or be arrested. The framework for cast insurance is built entirely around the vulnerability of specific human beings, and that vulnerability is the mechanism through which the coverage operates.

An AI production company whose lead 'actress' is a generated character has no cast insurance product available to them. If the AI company providing the generation technology goes offline, pivots its business, changes its terms of service, or simply loses access to the specific model parameters used to create that character — the production is exposed with no policy to respond.

Gap 3 — Completion Bonds: No Framework for AI Delivery

Completion bond companies guarantee to financiers that the film will be delivered on time and on budget. To issue a bond, they review the script, the budget line by line, the shooting schedule, and the credentials of the key personnel — director, producer, line producer. They are underwriting the probability that a specific group of experienced humans will execute a defined plan.

An AI production has none of these elements in conventional form. The 'script' may be a prompt architecture. The 'schedule' may be a generative pipeline run. The 'director' may be a technical supervisor with no conventional film production credit. No major bond company has published AI-specific underwriting criteria as of 2026.

This matters enormously for financing. Banks, presale buyers, and co-production partners require completion bonds as a condition of releasing funds. An AI production company that cannot obtain a bond cannot access institutional financing — which means it is entirely dependent on the kind of unstructured investor capital that Avary described. That capital comes in fast and can exit just as fast.

Gap 4 — General Liability: The Set That Does Not Exist

Standard production GL policies are written for physical locations — film sets, location shoots, studio facilities. They cover bodily injury, property damage, and personal liability arising from the production's physical presence in the world.

A fully AI-generated production that exists entirely within generative pipelines has no conventional set. There is no location. There may be no physical crew beyond a small technical team working in an office. Standard production GL products are not designed for this model and contain coverage language that may not apply.

This creates a liability gap in the opposite direction from cast insurance: instead of a missing product, there is an existing product that may not cover what it needs to cover. AI production companies buying off-the-shelf production GL policies without reviewing the specific coverage language for AI operations may discover at claim time that their coverage does not respond.

The Larger Picture — Why This Matters Beyond Individual Productions

The Cameron vs. Avary debate is not really about two filmmakers with different philosophies. It is a preview of where the entire industry is going — and the insurance industry's failure to keep pace creates real systemic risk.

Consider what happens when the first major AI film production faces a significant loss: a copyright lawsuit from an actor whose likeness was used without consent, a generative model that produces content that cannot be distributed, a production company that cannot deliver its committed release dates because its AI pipeline failed. With no established coverage, that loss lands entirely on the production company, its investors, and potentially its distribution partners.

That first major claim will reshape the market fast. Carriers will write exclusions, mandate disclosures, and raise premiums across the board — including for traditional productions that used any AI tools in their workflow. The film that used AI to generate background crowd shots in three scenes will find its E&O application flagged. The production that used AI for location scouting visualization will face new underwriting questions.

What Every Film Producer Needs to Do Right Now

Whether you are a traditional filmmaker, a hybrid production using AI tools, or an AI-first production company, here is the practical guidance that should be informing your insurance decisions in 2026:

• If you are a traditional production (Cameron model): Review your E&O policy for AI exclusion language. Many 2025-2026 policy renewals added endorsements that exclude coverage for productions using AI-generated content. Even if your production is fully human-made, verify that your policy does not contain exclusions that could be triggered by post-production tools your team may use without disclosure.

• If you are a hybrid production (using AI tools in some capacity): Disclose AI use to your broker before applying for coverage. Non-disclosure at the application stage is the fastest path to a denied claim. Be specific: what tools, what stages of production, what percentage of content. Different carriers have different tolerance levels. A specialist broker can find you the right market.

• If you are an AI-first production (Avary model): You need a specialist broker, not a generalist one. The coverage you need does not exist in standard form. What does exist is a combination of tech company E&O, cyber liability, professional indemnity, and modified production GL that — when structured correctly — provides meaningful protection. It requires someone who understands both the insurance market and AI production workflows.

• All productions in 2026: Check your E&O application for AI disclosure requirements. The Tilly Norwood situation demonstrated that AI-generated likenesses create copyright exposure that is not theoretical. The MPA's action against ByteDance over the Tom Cruise and Brad Pitt clip demonstrated that studios will enforce IP rights aggressively. Your E&O policy needs to respond when that exposure hits your production specifically.

The Full Comparison — Cameron Model vs. Avary Model

Insuring a Film Production in 2026? Talk to a Specialist.

Akker LLC works exclusively with film and TV productions — traditional, hybrid, and AI-assisted. Our founder Stan Shkilnyi is a SCAD film graduate and former film producer with 20+ years in the entertainment industry. We know which carriers are writing AI-adjacent coverage, what disclosure they require, and how to structure a policy that actually responds when something goes wrong.

Film Risk Portal: akkerins.com/filmriskmanagement

Film Quote App (over $1M): akkerins.com/film-quote-app

Short-Term Under $1M: akkerins.com/short-term-film-insurance

Contact Stan:stan@akkerins.com | 912-247-3075