Temp Worker Can Sue Special Employer for Job-Site Injury: What Every Staffing Firm Must Know

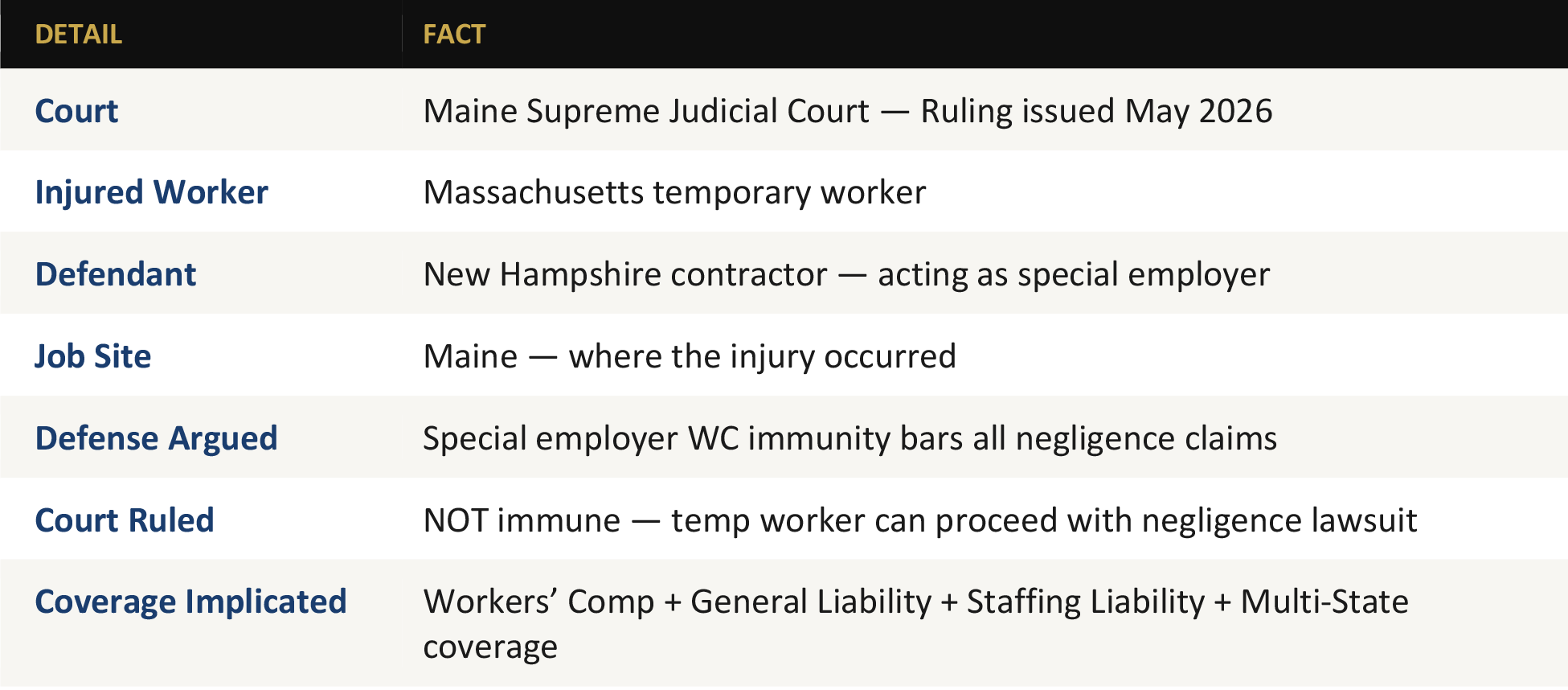

The Maine Supreme Judicial Court just ruled that a New Hampshire contractor acting as a “special employer” was NOT immune from a negligence lawsuit filed by a Massachusetts temporary worker injured at a Maine job site. If you run a staffing firm, this ruling changes how you need to think about your coverage, your contracts, and your liability — in every state you place workers.

The Case: What Happened

This case crossed three state lines before reaching its conclusion — and that’s exactly what makes it so important for staffing firms to understand.

The contractor argued it should be immune from the negligence lawsuit because it had taken on the role of “special employer” — a legal concept in workers’ compensation law that can, in some jurisdictions, extend WC immunity to a company that supervises and directs a temp worker’s day-to-day work.

The Maine Supreme Judicial Court rejected that argument. The court found that special employer status under Maine’s WC framework does not automatically shield the contractor from a separate negligence lawsuit filed by the injured temp worker.

THE COURT’S MESSAGE IN PLAIN ENGLISH

Accepting workers’ compensation liability as a special employer does NOT automatically grant immunity from negligence claims. The temp worker’s right to sue in tort survived the WC relationship. This ruling expands the litigation exposure of every company — staffing firm or client — that places or uses temporary workers across state lines.

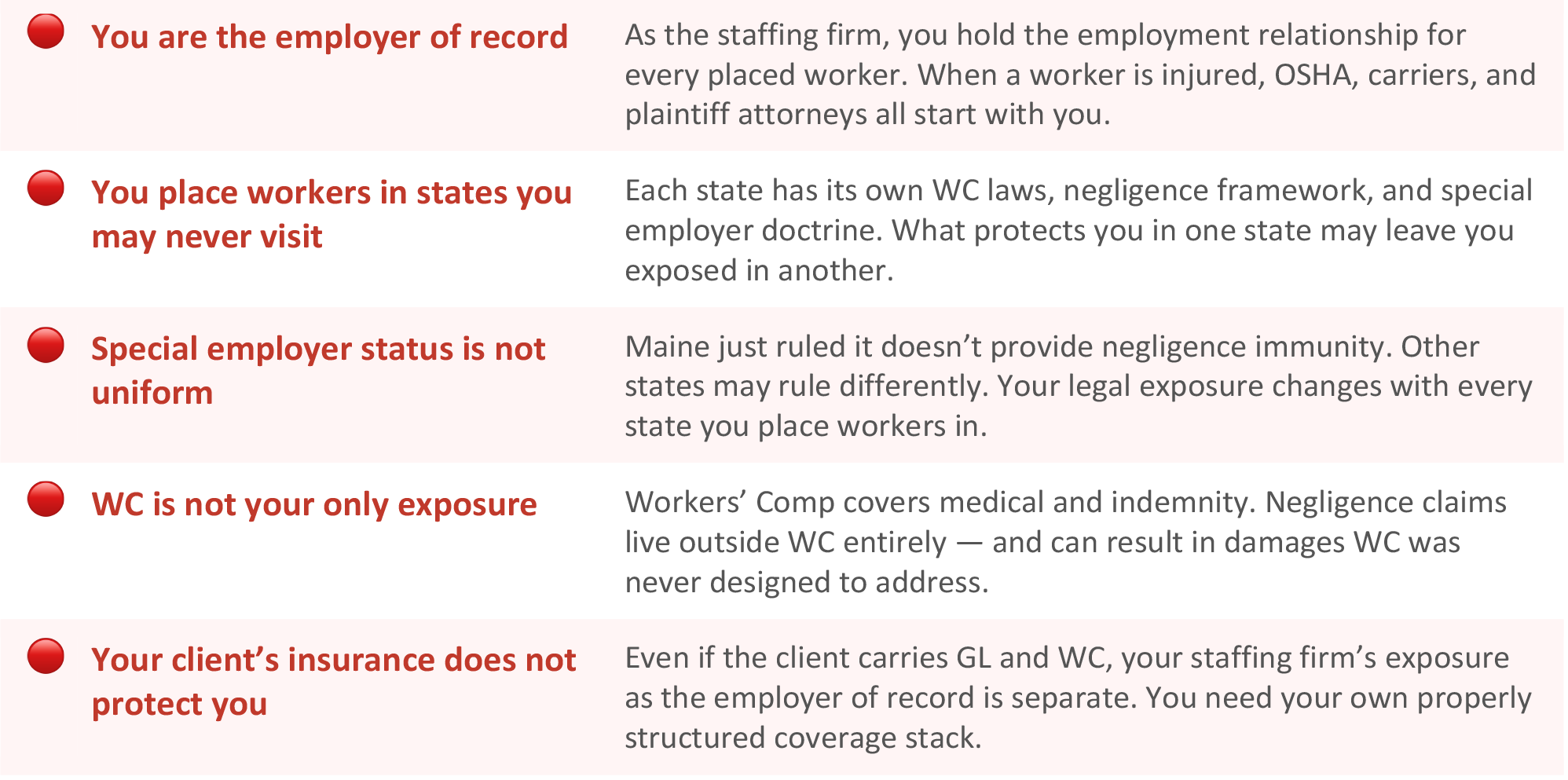

Why This Ruling Hits Staffing Firms Harder Than Anyone Else

Most businesses only have to worry about workers in their own facilities, under their own supervision, in one state. Staffing firms operate across an entirely different risk structure — one that this ruling puts directly in the spotlight.

The Multi-State Problem: Why This Gets More Complicated Every Placement

The Maine ruling illustrates a legal reality that most staffing firms underestimate: state law governs the rights of the injured worker, and state law is determined by where the injury occurred — not where your firm is headquartered, not where the worker lives, and not where the staffing contract was signed.

That means every state where you place workers is a potential jurisdiction with its own rules on:

• Whether special employer status provides negligence immunity

• What the WC exclusive remedy doctrine covers and excludes

• What damages a temp worker can recover in a negligence claim

• Whether your client’s WC coverage extends to your placed workers

• Whether you need separate WC coverage in that state or can rely on a master policy endorsement

• Whether the state is a monopolistic WC state (OH, WA, ND, WY) requiring state-fund coverage

THE MAINE RULING IN CONTEXT

Maine is one of many states where the scope of special employer immunity under WC law is actively litigated. New York, California, Texas, and Florida all have distinct frameworks for how temp worker injuries are handled across the WC and tort systems. A coverage structure that works in one state may leave your firm legally naked in another.

8 Steps Every Staffing Firm Must Take After This Ruling

This ruling is a signal, not an isolated case. Here is what your firm needs to do now to protect itself in every state where you place workers.

STEP 1 | Audit Your WC Coverage for Every State Where You Place Workers

✓ List every state where you have placed or currently place workers — including states where you’ve placed only one or two workers

✓ Confirm with your broker that your WC policy explicitly covers all those states on the declarations page

✓ Identify whether any of those states are monopolistic WC states (OH, WA, ND, WY) requiring separate state fund coverage

✓ Confirm your coverage applies to both W-2 placed workers and 1099 contractors where applicable

STEP 2 | Add Staffing Liability Coverage if You Don’t Have It

✓ WC covers medical bills and lost wages. Staffing Liability covers negligence claims, errors in placement, and third-party bodily injury claims that live outside WC

✓ This ruling is exactly the kind of claim Staffing Liability is designed to cover — a tort claim by a placed worker that WC immunity does not bar

✓ Confirm your Staffing Liability policy covers negligence claims arising from multi-state placements

✓ Ensure the policy does not contain a blanket exclusion for bodily injury claims, which are common in standard GL policies

STEP 3 | Strengthen Your Contractual Risk Transfer Language

✓ Every client contract should contain an indemnification clause requiring the client to defend and indemnify your firm for claims arising from the client’s own supervision or direction of placed workers

✓ Add a right-to-remove clause: your firm can pull placed workers from any client site where safety conditions are inadequate

✓ Require clients to name your staffing firm as an additional insured on their GL policy

✓ Include a governing law and jurisdiction clause identifying which state’s law applies to disputes under the contract

STEP 4 | Conduct a Multi-State Legal Review with Employment Counsel

✓ Engage employment or insurance defense counsel in each state where you place significant volumes of workers

✓ Ask specifically: does special employer status in this state provide WC immunity from negligence suits by placed workers?

✓ Review each state’s exclusive remedy doctrine and where its exceptions apply

✓ Document the findings and update your coverage and contract structures accordingly

STEP 5 | Review Your Client Onboarding Process for Safety Risk

✓ Before placing workers at any new client site, conduct a documented safety assessment of the workplace

✓ Ask clients to disclose their OSHA inspection history, recent incident reports, and current EMR

✓ Identify high-risk client environments (construction, manufacturing, warehousing, healthcare) that carry elevated injury risk across multiple states

✓ Implement a written go/no-go approval process for high-risk placements that requires sign-off from your operations leadership

STEP 6 | Train Your Recruiters on Multi-State Placement Risk

✓ Every recruiter placing workers across state lines needs to understand that WC immunity assumptions may not hold in the receiving state

✓ Train your team to flag high-risk placement scenarios: workers placed at heavy industrial sites, construction zones, hospitals, or warehouses in states your firm hasn’t analyzed

✓ Build a multi-state placement checklist into your placement workflow

✓ Document all training with attendance records and materials

Risk Management Checklist

Use this checklist to assess your firm’s current exposure and close the gaps this ruling has identified.

COVERAGE CHECKLIST — CONFIRM ALL OF THESE WITH YOUR BROKER

☐ WC policy declarations page lists every state where I place workers

☐ Monopolistic WC states (OH, WA, ND, WY) have separate state fund coverage

☐ Staffing Liability policy covers negligence claims outside WC — confirmed in writing

☐ GL policy does not contain a blanket bodily injury exclusion for placed workers

☐ Staffing Liability covers both W-2 placed workers and 1099 contractors

☐ Umbrella or excess policy extends over all primary coverage lines

☐ Employment Practices Liability (EPL) in place for discrimination and retaliation claims

☐ Annual coverage audit scheduled with a staffing insurance specialist

CONTRACT CHECKLIST — REVIEW ALL CLIENT AGREEMENTS

☐ Indemnification clause requires client to defend and hold harmless your firm for claims from client’s supervision of placed workers

☐ Client required to name your staffing firm as additional insured on their GL policy

☐ Right-to-remove clause allows your firm to pull workers from unsafe client environments

☐ Governing law and jurisdiction clause specifies which state’s law applies

☐ Client obligation to report workplace incidents involving placed workers within 24 hours

☐ Client required to conduct site safety orientation for all placed workers on first day

☐ Client required to maintain workers’ comp coverage for any workers they directly supervise

PLACEMENT OPERATIONS CHECKLIST

☐ Pre-placement client site safety assessment documented for every new client

☐ Multi-state placement checklist included in recruiter workflow

☐ Safety orientation records maintained for every placed worker

☐ Incident reporting system in place and communicated to all placed workers

☐ High-risk placement approval process documented and followed

☐ Multi-state legal analysis completed for top 5 states by placement volume

☐ All documentation retained minimum 5 years per placement

The Bottom Line

The Maine Supreme Judicial Court just told the staffing industry something it needed to hear: the legal protections you assume exist across state lines may not hold when a temp worker files a negligence claim in the state where they were injured.

The contractor in this case thought special employer status would protect it. The court said no.

The question every staffing firm owner needs to ask is simple: if a placed worker filed a negligence lawsuit against your firm tomorrow — in whatever state that worker was injured — would your coverage respond? Would your contracts protect you? Would your documentation be there to defend you?

The firms that can answer yes to all three questions will weather this legal landscape. The ones that can’t will find out the hard way that Workers’ Comp was never designed to be their only line of defense.

Is your staffing firm’s multi-state coverage built for today’s legal reality?

15+ years of staffing insurance expertise. Specialist coverage for the liability landscape that actually exists.