The NCCI Mod Worksheet Explained:

What It Is, How to Read It, and 8 Proven Ways to Lower Your Workers' Comp Premium in 2026

QUICK ANSWER · WHAT IS THE NCCI MOD WORKSHEET?

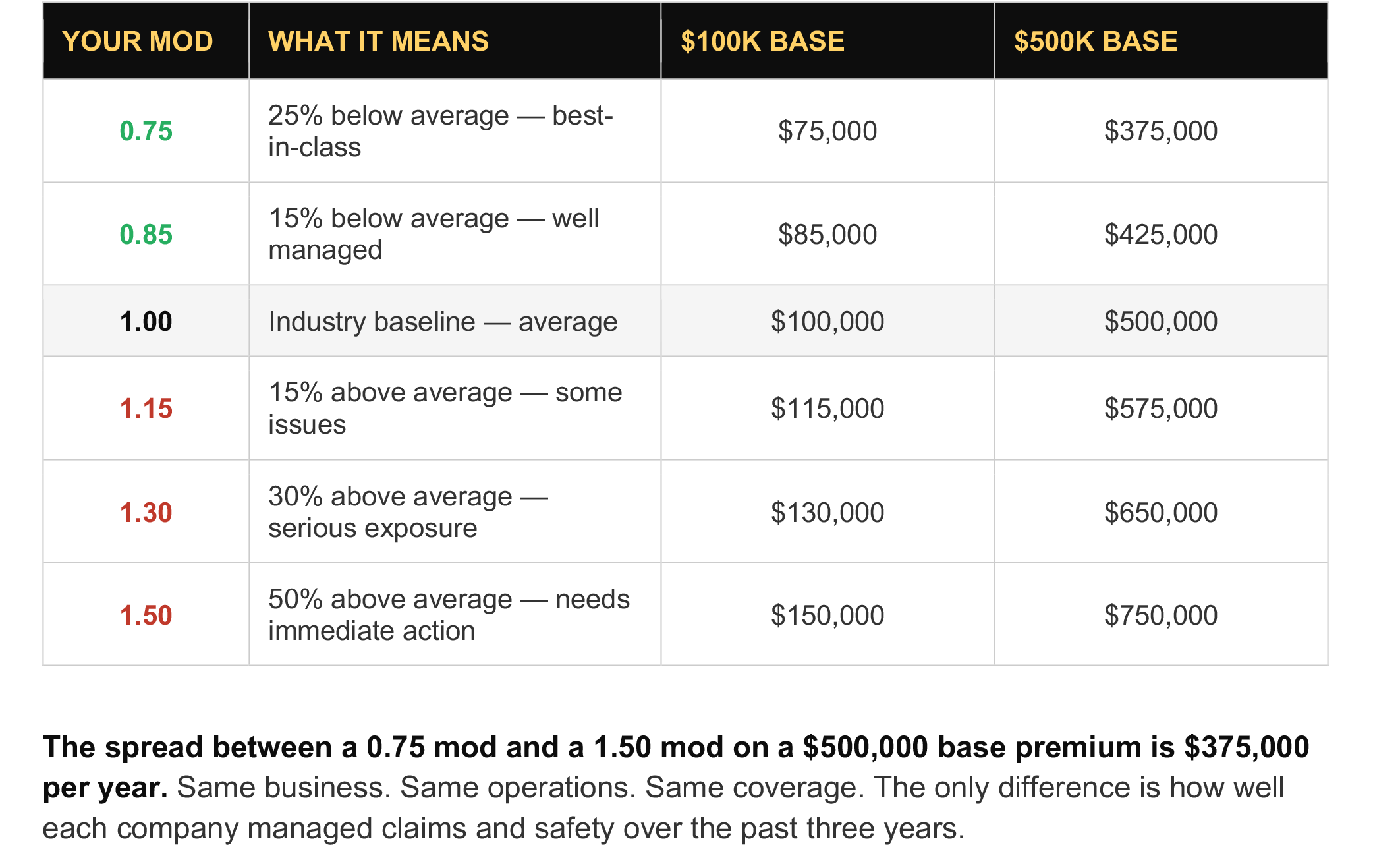

The NCCI Mod Worksheet is the official document that shows exactly how your business's Experience Modification Rate (EMR or "mod") was calculated by the National Council on Compensation Insurance. Your mod is a multiplier — typically between 0.75 and 1.50 — applied directly to your workers' compensation premium. A mod of 1.00 is average. Below 1.00 means you pay less; above 1.00 means you pay more. On a $500,000 base premium, the difference between a 0.85 mod and a 1.25 mod is $200,000 per year for identical coverage. The worksheet lists every claim, payroll figure, and class code used in the calculation. Roughly 1 in 4 worksheets contains an error that, when corrected, results in a lower mod and a premium refund.

Key Takeaways

• Your NCCI mod is a multiplier that directly adjusts your workers' comp premium based on your last three years of claims (excluding the most recent year).

• Frequency hurts your mod more than severity. Ten claims of $5,000 damage your mod more than one $50,000 claim because of how NCCI's primary/excess split point formula works.

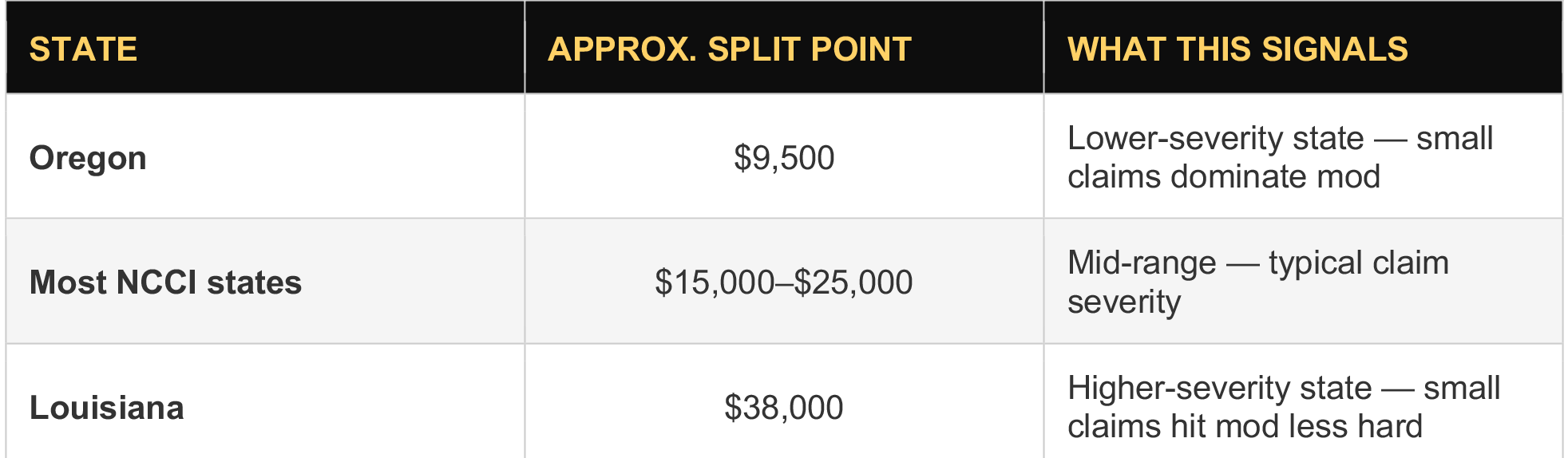

• As of November 1, 2023, NCCI moved from a uniform countrywide split point ($18,500) to state-specific split points that range from $9,500 (Oregon) to $38,000 (Louisiana) according to NCCI's Experience Rating Plan Methodology Update.

• About 1 in 4 mod worksheets contains an error — most commonly stale claim reserves, missing subrogation recoveries, or misassigned claims — that produces an inflated mod and an inflated premium.

• The 8 actions in this guide are ranked by impact: worksheet audit, 24-hour claim reporting, return-to-work program, open claim management, written safety program, class code review, audit preparation, and dispute filing.

What This Guide Covers

1. What is the NCCI Mod Worksheet and who calculates it?

2. How does your mod actually affect your workers' comp premium?

3. What are the 2026 state-specific split points?

4. What should you look for on your NCCI mod worksheet?

5. Why does claim frequency hurt your mod more than severity?

6. The 8 proven steps to lower your experience modification rate

7. Frequently Asked Questions about the NCCI mod

8. When to call a workers' comp specialist

1. What Is the NCCI Mod Worksheet?

The NCCI Mod Worksheet is the official calculation document produced by the National Council on Compensation Insurance (NCCI) — or your state's independent rating bureau — that shows exactly how your business's Experience Modification Rate was determined. Every business above a minimum premium threshold receives a worksheet annually.

Your Experience Modification Rate (EMR), commonly called the "mod," "e-mod," or "x-mod," is a multiplier that adjusts your workers' compensation premium based on your business's claim history over the past three policy years, not including the most recent year. The mod compares your actual losses against the expected losses for a business of your size and industry.

Who Calculates Your Mod?

Most states use NCCI. A handful use independent state bureaus that follow nearly identical methodology:

• NCCI states (about 38 states): The National Council on Compensation Insurance calculates and publishes the mod. ncci.com

• California: Workers' Compensation Insurance Rating Bureau (WCIRB). wcirb.com

• New York: New York Compensation Insurance Rating Board (NYCIRB). nycirb.org

• Other independent bureau states include Delaware, Indiana, Massachusetts, Michigan, Minnesota, New Jersey, North Carolina, Pennsylvania, Texas, and Wisconsin.

Who Is Eligible for a Mod?

Not every business gets a mod. A business must meet a minimum premium threshold — generally $5,000 to $10,000 in average annual workers' comp premium over three years, depending on the state. Below the threshold, the business defaults to a 1.00 mod. Once eligible, every workers' comp claim directly impacts the business's premium for the next three years.

THE SIMPLE VERSION

Your mod is a multiplier applied directly to your workers' comp premium. A mod of 0.85 means you pay 15% LESS than the industry average. A mod of 1.25 means you pay 25% MORE. On a $200,000 base premium, the difference between those two mods is $80,000 per year — for the exact same coverage.

2. How Does Your Mod Affect Your Workers' Comp Premium?

Understanding your mod is one of the most financially important things a business owner can do. Your workers' comp premium is calculated using a formula that includes payroll, class code rates, and your mod as a final multiplier. The table below shows the real-dollar impact across different mod values and base premium levels:

3. The 2026 NCCI Update: State-Specific Split Points Explained

A critical change every business owner needs to know about: On November 1, 2023, NCCI implemented its most significant Experience Rating Plan update in a decade — and it is still rolling through state filings in 2026. The change moves away from a single nationwide "split point" to a state-specific split point that varies dramatically depending on local claim severity.

What Is the Split Point?

The split point is the dollar threshold that divides each workers' comp claim into two parts:

• Primary loss: the portion of the claim BELOW the split point. This portion is given FULL weight in the mod formula because it indicates claim frequency.

• Excess loss: the portion of the claim ABOVE the split point. This portion is given REDUCED weight because severity is harder to predict and shouldn't disproportionately punish a business for one bad event.

Example: If your state's split point is $25,000 and you have a $80,000 claim, $25,000 is primary loss (full weight) and $55,000 is excess loss (reduced weight). This is why the split point matters so much — it controls how heavily individual claims hit your mod.

WHY THE 2026 STATE-SPECIFIC SPLIT POINTS MATTER

Under the old methodology, every NCCI state used the same $18,500 split point regardless of local claim severity. The 2026 methodology recognizes that a $20,000 claim in Oregon represents a very different severity profile than a $20,000 claim in Louisiana. Tailoring the split point to each state produces a more accurate mod calculation — but it also means business owners must check the split point applicable in THEIR state and understand which claims will hit their mod hardest.

2026 Split Point Range by State

According to NCCI's Experience Rating Plan filings, state-specific split points now vary significantly. Examples at the extremes:

4. What Should You Look For on Your NCCI Mod Worksheet?

You are legally entitled to a copy of your mod worksheet every year. Most business owners never request it. That is a mistake. Industry data and NCCI's own audit reviews suggest roughly 1 in 4 worksheets contains an error that, when corrected, lowers the mod and triggers a premium refund.

The 6-Point Mod Worksheet Audit Checklist

1. Every claim listed actually belongs to you. Mistakes happen — claims from other employers sometimes get assigned to the wrong NCCI risk number. Verify every claim against your internal incident records.

2. Closed claims show the correct final paid amount, not the original reserve. A claim closed with $0 paid should show $0 — not the $30,000 reserve that was originally posted.

3. Payroll figures match your final audited payroll, not estimated payroll. If your policy was based on estimated payroll and your final audited number was different, the worksheet may use the wrong figure.

4. Medical-only claims are reduced to 30% via NCCI's Experience Rating Adjustment (ERA). A medical-only claim (no lost time) is automatically discounted to 30% of its value. Confirm the ERA was applied.

5. Subrogation recoveries are reflected. If your carrier recovered money from a third party that caused an injury, that recovery should reduce the claim's impact on your mod.

6. Class codes are correct. There are roughly 700 NCCI class codes, and rates between them vary enormously. A misclassified employee inflates expected losses and produces an inflated mod.

5. Why Does Claim Frequency Hurt Your Mod More Than Severity?

This is the single most misunderstood concept in workers' compensation. Almost every business owner assumes one large claim is the biggest threat to their mod. The math says the opposite.

NCCI's Experience Rating Plan is intentionally designed to penalize claim frequency more harshly than claim severity. The reason is statistical: a business with many small claims displays a pattern of unsafe operations and is statistically more likely to produce a future catastrophic claim. A business with one isolated severe claim is less predictable in either direction.

REAL EXAMPLE — FREQUENCY VS. SEVERITY

Ten claims of $5,000 each ($50,000 total losses) will damage your mod MORE than one claim of $50,000. The ten small claims each hit the primary layer at full weight because each individual claim is below the split point. The single $50,000 claim has most of its cost in the excess layer — where weight is heavily reduced. What this means for your business: preventing slips, strains, and minor injuries matters more for your mod than avoiding rare catastrophic events. Manage frequency first.

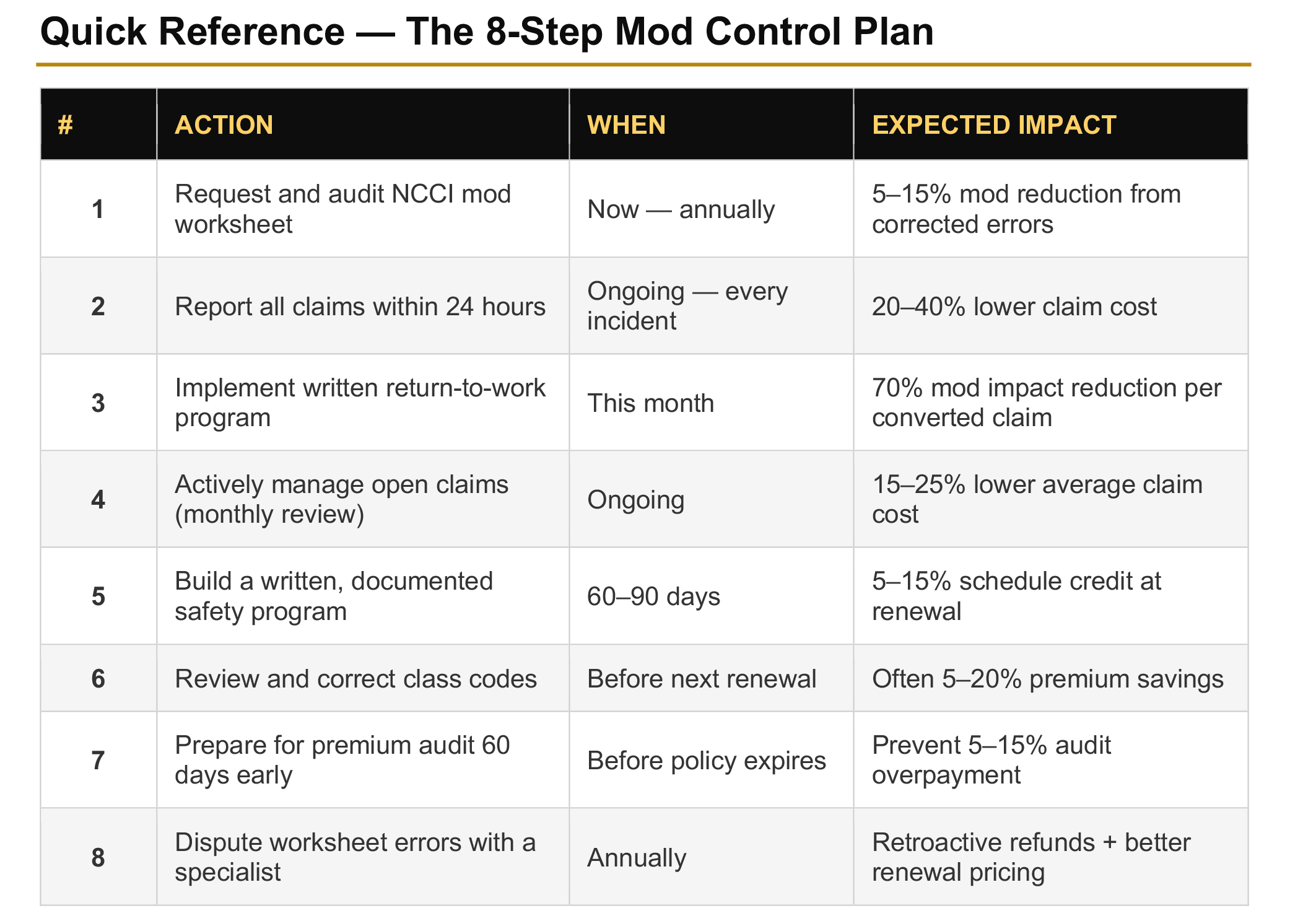

6. The 8-Step Plan to Lower Your Experience Modification Rate

These are the eight actions that move the mod needle the most, listed in order of impact and speed. Each step includes a specific action you can take this week.

Step 1 — Request and Audit Your NCCI Mod Worksheet

Email your broker — or request directly from NCCI at ncci.com — for a copy of your current mod worksheet. Then audit it using the 6-point checklist in Section 4. This single step regularly produces 5–15% mod reductions when errors are corrected. The most common winning finds: closed claims still showing original reserve amounts and claims misassigned to the wrong employer.

Step 2 — Report Every Claim Within 24 Hours

Claim reporting speed is the single highest-leverage operational change most businesses can make. Industry studies — including data published by NCCI and major carriers — consistently show that claims reported within 24 hours cost 20–40% less than claims reported one week or more after the incident. Late-reported claims develop more slowly, attract higher reserves, and sit open longer.

Build a simple one-page incident reporting workflow. Post it. Train every supervisor on it. Audit it monthly.

ACTION — STEP 2

Set a company-wide policy today: every workplace incident — regardless of whether medical care is sought — is reported to HR or management within the same business day, and to the insurance carrier within 24 hours.

Step 3 — Implement a Written Return-to-Work Program

A return-to-work (RTW) program is the highest-ROI risk management initiative most businesses can implement. NCCI's Experience Rating Adjustment automatically reduces the mod impact of a medical-only claim (no lost time) to just 30% of its actual cost. If you bring an injured employee back in a light-duty role before they are fully recovered — even answering phones, filing, or counting inventory — you convert an expensive indemnity claim into a cheap medical-only claim and immediately cut that claim's mod impact by 70%.

ACTION — STEP 3

Write a one-page transitional duty policy. List five light-duty tasks any injured worker could perform regardless of restrictions. Offer transitional duty in writing within 48 hours of every injury. Document the offer even if the employee declines.

Step 4 — Actively Manage Open Claims

Open claims count toward your mod at their full reserve value — not at their eventual paid value. An open claim with a $50,000 reserve is costing you premium today even if it ultimately settles for $20,000. The goal is to close claims faster and keep reserves accurate.

• Call your adjuster every 30 days on every open claim.

• Push for an independent medical exam (IME) when treatment is plateauing.

• Request monthly reserve reviews in writing.

• Push to close settled claims before the annual unit statistical reporting date (typically 18 months after policy inception).

• Flag any claim where a third party's negligence may have caused the injury — subrogation recoveries reduce mod impact.

ACTION — STEP 4

Ask your broker to schedule a quarterly claims review meeting with your carrier's adjuster. Review every open claim with reserves above $10,000. This single habit reduces average claim cost by 15–25% over time.

Step 5 — Build a Real Written Safety Program

Carriers reward written, documented, audited safety programs with schedule credits at renewal — typically 5–15% off your premium. More importantly, a real safety program reduces the frequency of small claims, which (as Section 5 explained) is where most mod damage comes from.

A real safety program is not a binder on a shelf. It includes written hazard assessments for every job role, documented training records with signatures, toolbox talk logs, PPE issuance records, and a clear incident reporting procedure. If you cannot produce these documents during a carrier loss control visit, you will not receive the schedule credit.

ACTION — STEP 5

Start with two documents this week: a written hazard assessment for your highest-risk job role, and a signed safety training log for your last training session. Build from there.

Step 6 — Review Your Workers' Comp Class Codes

Workers' comp class codes determine the base rate applied to your payroll. There are roughly 700 NCCI class codes, and the rates vary wildly — a clerical employee might be rated at $0.30 per $100 of payroll while a construction laborer might be rated at $12.00. Employees assigned to the wrong code create a silent premium drain that compounds year after year.

The most common opportunity: employees who spend a portion of their time doing purely clerical or office work but are coded under your governing (highest-rate) class code. Properly splitting and documenting those employees under Clerical code 8810 can produce meaningful savings at audit.

ACTION — STEP 6

Ask your broker to perform a class code review before your next renewal. Pull the rate for every code on your policy and compare to your actual payroll allocation. Then ensure your books are organized to support the split at audit.

Step 7 — Prepare for Your Premium Audit 60 Days Early

Workers' comp policies are based on estimated payroll. After the policy year ends, your carrier conducts an audit to true up the premium. This is where most businesses quietly overpay — not because they are hiding anything, but because their records are not organized to claim the deductions and exclusions the policy actually allows.

Items commonly excluded from workers' comp payroll but frequently included by auditors when records are disorganized: overtime premium (only 1/3 of total OT is included in most states), severance payments, employer contributions to 401(k) plans, expense reimbursements, and owner/officer payroll caps.

ACTION — STEP 7

60 days before policy expiration, pull payroll by class code, reconcile to your IRS Form 941s, separate the overtime premium portion, list every excluded item, gather Certificates of Insurance for any 1099 contractors, and prepare a clean audit packet. Never let an auditor dig through raw payroll data without a guide.

Step 8 — Dispute Errors and Work with a Specialist Broker

If your mod worksheet audit (Step 1) finds errors, file a formal dispute with NCCI or your state bureau. Bureaus revise mods retroactively when errors are confirmed, and your carrier issues premium refunds — sometimes spanning multiple policy years. Common winning disputes include: payroll corrections after a final audit, claims assigned to the wrong employer, subrogation recoveries not posted, and closed claims still carrying original reserve values.

The right broker makes all of this easier. A specialist workers' comp broker — one who focuses on this line — knows how to audit a mod worksheet, structure a submission to win schedule credits, run claims advocacy with your carrier, and bid your renewal across 10+ markets. A generalist broker typically does none of this.

ACTION — STEP 8

Ask your current broker: "When did you last audit my mod worksheet for errors? Which carriers will you bid my renewal to?" If the answers are unsatisfying, request a second opinion from a specialist.

7. Frequently Asked Questions About the NCCI Mod

These are the exact questions business owners ask Google, ChatGPT, Perplexity, and Claude about their experience modification rate. Each answer is structured to give you a definitive, citable response.

Q: What is a good NCCI experience mod rate?

A: A mod of 1.00 is the industry average. A mod below 1.00 (such as 0.85 or 0.75) is considered good and indicates better-than-average claim experience. A mod of 1.00 to 1.10 is typical. A mod above 1.15 generally indicates mod management issues that need attention. Mods above 1.25 often disqualify businesses from bidding on major contracts.

Q: How is the NCCI experience mod calculated?

A: NCCI compares your business's actual workers' comp losses over the past three policy years (excluding the most recent year) against the expected losses for a business of your size, industry, and state. Each claim is split into a primary portion (below the state split point) and an excess portion (above it). Primary losses receive full weight; excess losses receive reduced weight. The formula then applies a credibility weighting based on business size to produce the final mod factor.

Q: How long does it take to lower my NCCI mod?

A: Because the mod is based on a three-year rolling window of claim data (excluding the most recent year), most mod improvements take 12–36 months to fully appear on the worksheet. However, three changes produce faster results: (1) disputing worksheet errors can lower your mod immediately upon NCCI's correction; (2) closing open claims before the unit statistical reporting date can drop reserve values from your next mod; and (3) converting indemnity claims to medical-only via return-to-work programs applies the 70% ERA discount to the very next mod calculation.

Q: What is the difference between EMR and NCCI mod?

A: There is no difference. EMR (Experience Modification Rate), e-mod, x-mod, and "NCCI mod" all refer to the same number: the multiplier applied to your workers' comp premium based on your three-year claim history. NCCI is the organization that calculates it in most states. California uses the WCIRB and New York uses the NYCIRB, but the concept is identical.

Q: Can I dispute my NCCI mod?

A: Yes. You can file a formal dispute with NCCI (or your state's independent rating bureau) for any error on your worksheet. Common winning disputes include claims assigned to the wrong employer, closed claims still showing original reserve values, payroll corrections after a final audit, and missing subrogation recoveries. When NCCI confirms the error, your mod is revised retroactively and your carrier issues a premium refund.

Q: What is the 2026 NCCI split point?

A: As of November 1, 2023, NCCI moved from a uniform $18,500 countrywide split point to state-specific split points. As of 2026, split points range from approximately $9,500 (Oregon) to $38,000 (Louisiana), with most NCCI states between $15,000 and $25,000. The split point is the dollar threshold that divides each claim into primary loss (below — full weight in mod) and excess loss (above — reduced weight). Check NCCI.com or ask your broker for your specific state's current split point.

Q: Does a $0 closed claim affect my mod?

A: Typically no — but only if NCCI correctly reflects the $0 paid amount on your worksheet. A claim closed with no payment should show $0 in losses. However, one of the most common worksheet errors is a closed-no-pay claim still listing the original reserve amount that was set when the claim was first reported. This is one of the highest-yield items to audit on your worksheet because correcting it often produces a meaningful mod reduction.

Q: How does a return-to-work program lower my NCCI mod?

A: NCCI applies an Experience Rating Adjustment (ERA) that automatically reduces the mod impact of a medical-only claim (no lost time) to just 30% of its value. If you bring an injured employee back in any productive light-duty role before they would otherwise be released to full duty, you convert an indemnity claim (full weight) into a medical-only claim (30% weight) — a 70% reduction in that claim's mod impact. This is the highest-ROI mod management lever available to most businesses.

Q: Why did my workers' comp premium go up if I had no claims?

A: Several factors beyond claims can drive premium up at renewal: (1) NCCI annual loss cost or rate filings approved in your state; (2) payroll growth — more payroll equals more premium even at a stable rate; (3) class code rate changes; (4) loss of schedule credits at renewal if your safety documentation has weakened; (5) carrier-specific rate changes; (6) policy form changes. Even with zero claims, the underlying loss costs your carrier files with the state can move up or down.

Q: Do I need a specialist broker for workers' comp?

A: For most businesses with a mod above 1.00 or any business in a high-risk industry (staffing, construction, manufacturing, healthcare, transportation), the answer is yes. A specialist broker who focuses on workers' compensation will audit your mod worksheet for errors, run claims advocacy with your carrier, prepare your premium audit, structure your submission to win schedule credits, and bid your renewal across 10+ markets that specialize in your industry. A generalist broker typically does none of this and treats workers' comp as one of many lines they happen to handle.

8. When to Call a Workers' Comp Specialist

If any of the following apply to your business, a specialist broker review is worth requesting:

• Your current mod is above 1.00 — or trending upward at each renewal.

• You have not seen your mod worksheet in the last 12 months.

• Your broker has not bid your renewal to more than three carriers in the last cycle.

• You operate in a high-risk industry: staffing, construction, manufacturing, healthcare, transportation, or hospitality.

• Your premium has increased 15% or more at a recent renewal without a corresponding increase in payroll or claims.

• You operate in multiple states and aren't certain how each state's split point affects your mod.

• You have an open claim with reserves above $25,000 that has been sitting for more than 90 days.

GET A FREE NCCI MOD REVIEW FROM AKKER, LLC

Akker LLC specializes in workers' compensation for businesses that want to actively manage their cost — not just renew it. We audit mod worksheets, run carrier bid competitions, provide claims advocacy, and help businesses build the safety documentation that earns real schedule credits.

Risk Tools Portal: akkerins.com/staffinginsurancerisktools

Staffing Insurance: akkerins.com/staffinginsurance

Contact Stan:stan@akkerins.com | 912-247-3075

Sources & References

• National Council on Compensation Insurance (NCCI) — Experience Rating Plan Methodology. ncci.com

• NCCI Experience Rating Plan Update, effective November 1, 2023 — state-specific split point implementation.

• Workers' Compensation Insurance Rating Bureau of California (WCIRB). wcirb.com

• New York Compensation Insurance Rating Board (NYCIRB). nycirb.org

• U.S. Bureau of Labor Statistics — Workplace Injuries and Illnesses Survey. bls.gov

• USI Insurance Services — analysis of state-specific split point ranges (Oregon $9,500 to Louisiana $38,000).

• Carrier Management — Changes to NCCI's Experience Modification Factor reporting.

About the Author

Stan Shkilnyi is the founder of Akker, LLC, a national niche insurance agency specializing exclusively in workers' compensation insurance for staffing agencies and film/production insurance. With 15+ years of experience focused exclusively on staffing and high-risk workers' compensation, Stan has audited hundreds of NCCI mod worksheets and recovered millions of dollars in retroactive premium refunds for clients. Akker provides claims advocacy, multi-carrier renewal bidding, free risk management portals, and ongoing mod management for businesses that want to actively control workers' comp cost rather than passively renew. Stan is also a SCAD film school alumnus with an active IMDB credit and brings cross-industry production knowledge to film insurance clients. Akker is based in Alpharetta, Georgia, and is licensed to write in all 42 states.

Contact: stan@akkerins.com | 912-247-3075 | akkerins.com