California Workers’ Comp Is a Crisis in 2026 — And Every Staffing Agency in the State Needs to Know It

If you run a staffing agency in California, 2026 is not the year to be reactive about your workers’ compensation insurance. The market has reached a breaking point — and the agencies caught flat-footed at renewal are facing rate increases, coverage restrictions, and in some cases, carriers simply walking away.

Here is what is happening, why it matters specifically to staffing firms, and what you need to do right now.

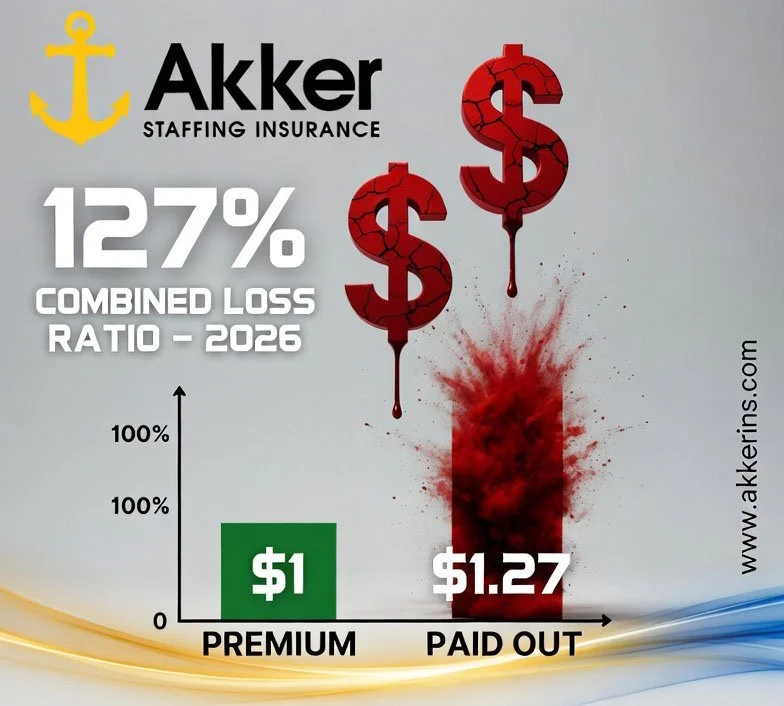

The 127% Problem: What That Number Actually Means

California’s workers’ compensation combined loss ratio has hit 127% in 2026. That means for every single dollar an insurance carrier collects in premium, they are paying out $1.27 in claims and expenses. The workers’ comp market in California is not breaking even — it is hemorrhaging money.

What does that mean for you as a staffing agency? It means carriers are recalibrating. They are raising rates, tightening underwriting criteria, and scrutinizing staffing accounts more carefully than they have in years. If your renewal is coming up and you haven’t had a proactive conversation with your broker about your exposure, you are likely to be surprised — and not pleasantly.

KEY STAT:

California Combined Loss Ratio in 2026 = 127%. Carriers are paying $1.27 for every $1.00 collected. Rate increases are not optional — they are mathematically inevitable.

Why Staffing Agencies Are the Most Exposed

Not all employers feel the workers’ comp crisis equally. Staffing agencies are uniquely vulnerable for three specific reasons:

1. You Place Workers Into High-Risk Environments

• Warehouse, logistics, light industrial, and hospitality placements carry significantly higher injury rates than office-based work.

• Temporary workers are statistically more likely to be injured in their first 30 days — before they know the environment, the equipment, or the safety protocols.

• High workforce turnover means you are constantly onboarding new workers into unfamiliar settings, compounding the risk.

2. Cumulative Trauma Claims Are Surging

California has seen a dramatic surge in cumulative trauma (CT) claims — injuries that develop over time from repetitive motions rather than a single incident. These claims are notoriously difficult to defend, take significantly longer to close, and almost always involve extended treatment timelines that drive up claim severity. For staffing agencies cycling workers through repetitive-motion roles — assembly, packing, picking — CT exposure is now one of the biggest hidden liabilities on the books.

3. Medical Inflation Is Compounding Every Claim

The same workplace injury that cost $18,000 to resolve in 2022 can now exceed $28,000 or more. Prescription drug costs, surgical fees, and post-acute rehabilitation are all rising faster than general inflation. Every open claim on your loss run is now more expensive to close than it was three years ago — and that directly impacts your experience modification factor (ex-mod) and your renewal premium.

The Litigation Factor: Attorney Involvement From Day One

California has one of the most active plaintiff bars in the country when it comes to workers’ compensation. Injured workers are increasingly represented by attorneys from the moment a claim is filed — not after a dispute arises. Attorney involvement extends the life of a claim, increases the final settlement amount, adds legal defense costs on both sides, and makes light-duty return-to-work programs harder to execute.

For staffing agencies, this is compounded by the fact that you often have limited visibility into what happens after a worker is placed. If your client does not have a strong safety program, incident reporting protocol, or return-to-work structure in place, your claims get worse — and your premium reflects it.

What Mandatory Rate Increases Actually Look Like

Staffing agencies operating in California should expect the following at their next renewal if they have not already addressed their exposure:

• Base rate increases of 10–25% across high-risk class codes including warehouse, industrial, and hospitality

• Experience mod surcharges for agencies with claims activity over the past three years

• Carrier non-renewals for accounts with combined loss ratios above 60–65%

• Increased scrutiny on your client list, placement types, and safety documentation

Agencies that are proactive — that have clean loss runs, documented safety programs, and a broker who specializes in staffing — will still see increases, but they will be manageable. Agencies that walk into renewal without preparation are looking at sticker shock.

What California Staffing Agencies Should Do Right Now

There are concrete steps you can take before your renewal arrives to position your agency as favorably as possible in this hardened market:

• Pull your loss run today. Know your three-year claims history before your carrier does the math for you. Understand your ex-mod and what is driving it.

• Implement ergonomic oversight for placed workers. Specifically for repetitive-motion placements, this directly reduces cumulative trauma exposure and demonstrates to underwriters that you take risk management seriously.

• Build a return-to-work program. This single initiative has more impact on claim severity than almost anything else. Keeping injured workers connected to light-duty roles shortens claims timelines and lowers total costs.

• Document your safety program. Written safety protocols, new hire orientation documentation, and incident reporting procedures are underwriting gold. Carriers price based on risk — documentation proves you manage it.

• Talk to a broker who specializes in staffing — now, not at renewal. The staffing insurance market is not the same as general commercial insurance. The class codes are different, the coverage nuances are different, and the carriers who understand staffing are a short list. Working with a generalist broker on a staffing account in this market is a costly mistake.

How Akker Is Helping California Staffing Agencies Navigate This Market

At Akker, staffing insurance is not a side business — it is one of our three core specialties alongside film and production insurance. We understand how temp agencies and light industrial staffing operations are underwritten, where the coverage gaps typically hide, and how to position your account to get the best available terms in a market that is actively tightening.

We are currently reaching out to every California staffing client ahead of their renewal to conduct a coverage review, run loss analysis, and make sure their program is built for what the 2026 market actually looks like — not what it looked like three years ago.

If you are a California staffing agency and haven’t had this conversation yet, let’s change that before your renewal forces it.

Ready to review your California workers’ comp coverage?